Investors and the press love to read the tea leaves of the FOMC meeting minutes. Most in the press believe July 31st Federal Reserve Open Market Committee meeting minutes confirm quantitative easing, the $85 billion a month in mortgage backed securities and asset purchases, will be reduced starting in September. We don't know that answer but we can guess. From the minutes:

Looks like history could be repeating itself. Now we've known for some time that the Chinese were getting weary about buying and holding US-Dollar demominated government securities. They've been pairing back from the longer dated maturity paper to shorter ones.

Slowly but surely, they want to move away from American debt. All that money we've been shoveling their way, a byproduct to our trade imbalance, has gone into things showing their diversification plan, from farm lands in Africa to purchasing major steaks in mining firms to buying precious metals and oil. Now it seems, according to one Li Liangzhong, want to extend into further real estate purchases in the US.

The global financial crisis may morph into a second, equally virulent phase where borrowing costs rise again, hobbling an embryonic economic recovery, debilitating cash-strapped banks, and punishing investors all over again.

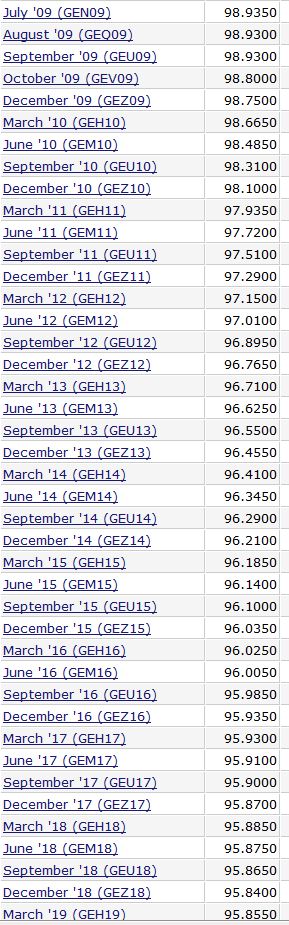

Deflation, inflation, it really doesn't matter. The price for money, that is interest rates, is going up. You can see it in the back month contracts in the futures market. You can see it in the failed auctions for foreign debentures like the Gilt in the UK. Investors/lenders are demanding a higher rate for loaning out money. The banks may be lending, but it's still a capital desert out there. We were at historical lows, not seen in decades. Folks, it was not always going to stay that way.

Remember when buying Tech stocks would make you wealthy? Then that bubble burst.

Remember when buying a house would make you wealthy? Then that bubble burst Remember when...

Remember when the present crisis broke in 2007, the reassurances that it would not spread beyond the confines of subprime; when it did spread, the forecasts that Wall Street banks

' losses would amount only to a total of about US$200 billion. Remember when "experts" insisted no widespread credit crunch would result. Remember when they insisted that the crisis was unlikely to spread from Wall Street to the real economy on Main Street?

One of the lunch regulars, Dave the BondMan, notes for to our suprise that the Rate for a Credit Default Swap, the cost of insuring against default, on a 5 Year US Treasury Note is now a full 100 basis points.

The cost of credit default insurance is a real world, market assessment of the risk of default of the U.S. Govt, as opposed to the fantastical ratings issued by Moodys and S&P.

The Yield on a 5 Year T Bond is 1.92%.

It now costs more than one half of your return to guarantee a midrange US sovereign debt note.

Long-dated Treasuries rallied with the 30-year bond jumping more than 3 points

The cost to insure against $10 million of debt issued by the U.S. government jumped to 47.5 basis points or $47,500 per year for five years, according to credit data company CMA DataVision. This compared with 43.5 basis points or $43,500 late Monday.

Credit default swaps insuring $10 million of U.S. Treasuries edged up to a record 50.0 basis points or $50,000 a year for 10 years

Earlier, before these latest expenditures, CNBC wrote a story that the U.S. might lose it's AAA credit rating.

{kind=link}

Recent comments