“China is still pegging its currency which is destroying our manufacturing sector”

WOW! You have just gone head to head with Bonddad, New Deal Democrat and SilverOz. They have be trumpeting the ‘myth of American Manufacturing in decline'. I don’t know how to link but see one example: “No, Virginia, US Manufacturing Isn’t Dead” -Bonddad 2/23/2010. I hope you would comment.

I periodically read him but I keep trying to keep the middle column RSS feeds on people who are consistently accurate vs. some sort of economic religious view, as you noted, that claim of somehow the entire world must return to serfdom to "maximize the economy" mantra.

But that entire "call out" stuff, well, in my view if you're going to do that a lot....you had better your own backyard spotless and well....

uh, about that "V" jobs growth....

;)

But overall Mish is reasonably accurate and insightful, but we're the layperson's blog, the working stiff, the middle class, so obviously helping promote various people who really would like to wipe it out...well, that's why they aren't in the middle column...

But I am finding some of the weirdest "blind spots" in almost every economic category as of late. Someone will be dead on in one area, say derivative reforms or global finance...and then you'll find pure economic fiction in say something like trade or labor econ. Very weird.

If the workforce has to compete against cheaper labor in other countries, then its earning power will be diminished. Carey even anticipated the situation we find ourselves in today, noting in his time that as earning power diminished, the U.S. must buy imports on credit, creating a bubble of indebtedness that must sooner or later burst.

Minsky, Carey, etc. There are plenty of people who predicted the situation we've gotten into, but only the Chicago School of Economics is being taught. Since the Chicago School is so flawed, no one can imagine the solutions.

For instance, arguing against "Free Trade" is practically useless because it has become a religious issue rather than a scientific one. Even so-called progressives, like Bonddad and Krugman won't go against the Free Trade canon.

Back around 1992 or so, when the web was relatively new, there was a professor in the Netherlands who had started a project on U.S, history using the new mark-up language of HTML. I was the person who added an article on Henry Carey, and added a series of long quotes from most of the chapters of Carey's 1851 book The Harmony of Interests: Agricultural, Manufacturing & Commercial.

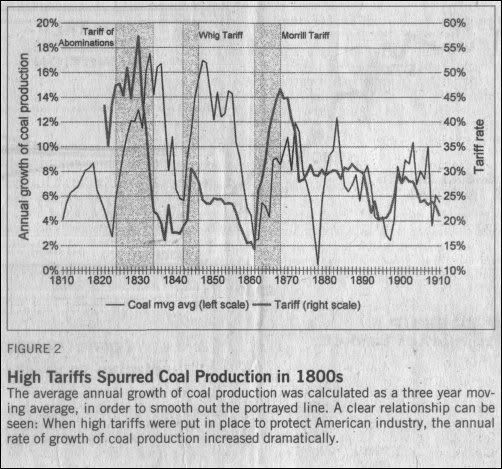

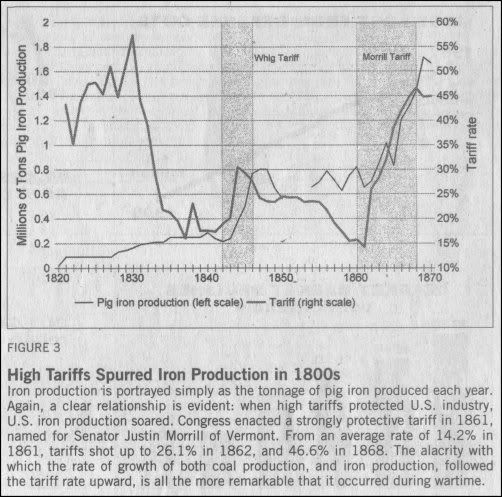

In the early 1990s, I used the Bicentennial Statistical Abstract - Colonial and Historical Statistics, to plot out steel production, railroad mileage built, and coal production, against the various tariff regimes in the 1800s to 1920s. The results were very stark: low tariffs are strongly correlated with downturns in real production, and high tariffs are strongly correlated with increased in real production. Exactly like Henry Carey, wrote in the mid-1800s. These are the charts I generated back (God, do I miss QuattroPro - trying to edit Excel graphics suck by comparison, even now, nearly two decades later)

, scanned from the clippings of my articles.

Carey explained that the ability to import is based on the ability to pay. The ability pay, in turn, is based on the earning power of the nation’s workforce. If the workforce has to compete against cheaper labor in other countries, then its earning power will be diminished. Carey even anticipated the situation we find ourselves in today, noting in his time that as earning power diminished, the U.S. must buy imports on credit, creating a bubble of indebtedness that must sooner or later burst. Unfortunately, the person who discussed the American System a lot back then when I was writing was Lyndon LaRouche. But, in the late 1980s, James Fallows went to Korea and Japan to write about why their economies were doing so much better than the U.S.'s. The Koreans and Japanese gave him an earful of American history, including Carey, List, and E. Peshine Smith (Smith being the economist, I believe, who introduced American System thinking to the Japanese, which formed the basis for the period unfortunately called the Meiji Restoration, when Japan began to "copy" Western industrialization. In actuality, the Japanese were implementing the nation-building programs Alexander Hamilton had elaborated as Secretary of the Treasury. Fallows laid all this out in a great series of articles in The Atlantic. I suspect, but don't know for sure, that it was Fallows' articles that were picked up up Michael Lind, who is now one of the most vocal proponents for a return to American System policies. See especially Lind's 1997 book, Hamilton's Republic: Readings in the American Democratic Nationalist Tradition

(You see, Mr. Oak, I was never able to fully grasp the mathematical side of modern economics, but I was able to pick up a lot from economic and industrial history!)

What is important to note is that the traditional opponent of the American System, the laissez faire of the British East India Co., (which was formulated almost solely to justify the moral depravity of Britain's opium trade with India and China), was repackaged by Milton Friedman and sold to Americans as "freedom to choose."

A particularly important book to read, for anyone who wants to understand more about the actual economic policies that created the United States, is The Great Challenge: The Myth of Laissez-Faire in the Early Republic, by Frank Bourgin. Interestingly, Bourgin's book is his 1940s PhD dissertation, which was rejected by the University of Chicago. Bourgin published the book in the 1980s after being encouraged hy historian Arthur Schlesinger Jr.

I hve an underwater mortgage I borrowed "from Suntrust," but it turns out that it was then actually owned by Fannie Mae. I could solve part of Fannie Mae's problem by buying this "underwater" mortgage at its present value. In fact, there are many of us who could provide relief for Fannie's cash-short problem -- they get rid of the toxic "default risk" and reduce their cost at the same time. Hey Fannie, who is the person to talk to about this financial innovation?

Frank T.

of wealth. The one you usually hear about from liberals and progressives is the "tax cuts for the rich." Conservatives retort that hardly anybody with less than 25,000 or so in income pay taxes. That's only true in so far as federal income taxes. When you look at the variety of other taxes, from FICA at the federal level down to state and local property and retail taxes, the tax structure in the U.S. is actually highly regressive.

The other mechanism hardly anyone talks about is the burden of usury, speculation, and economic rent seeking behavior imposed by the financial system. The $25 billion Goldman Sachs dispensed in bonuses has to come from somewhere. This year, of course, it came directly from the taxpayer in the form of bailouts. But in previous years, this money would come out of the hide of the rest of the population whose incomes and benefits were held down in order to "meet Wall Street expectations." This mechanism is discussed from the perspective of the investor class by Warren Buffet in his little story about the Gotrocks family and what they pay for financial advice. But the more correct perspective is breathtakingly captured in the Frontline May 2006 story Can You Afford to Retire?, in the segment about the bankruptcy of United Airlines. While the employees of United lost almost all their pension, "The banks, with their superpriority, got back every penny plus interest, plus tens of millions of dollars in fees." You have to watch the video to get the full impact of former J.P. Morgan executive Repko has he smiles smugly and admits that, yes, JP Morgan got every penny it asked for.

Similarly, wealth is transferred by the fees and profit margins generated by the enormous amount of financial trading. Two years ago, I created the Wikipedia page on financialization with a table showing financial turnover compared to gross domestic product. This is work I first did in the early 1990s. In the 1960s, it took all financial markets about nine months to trade the dollar volume equivelent to one year of GDP. Today, it takes about three days.

How much does it cost our economy to move around this much financial paper each and every day? Let us assume that the fees, commissions, and so on paid to the financial system for all this frenetic activity amount to one percent. (An October 2003 study conducted by John P. Hussman, President of Hussman Investment Trust, found that the costs to the funds he manages actually amounted to approximately 1.87%; scroll down to the bottom.)

So, one percent of three trillion a day is $30 billion in commissions / fees / bonuses, etc., paid to the financial system for all that paper being shoved around. That's the amount that is going to all those people like the guys in the Chicago futures pits standing behind CNBC's Rick Santelli you saw last month.

$30 billion a day is the equivalent of 600,000 (six hundred thousand) jobs paying $50,000 a year.

That is, the cost to the economy of allowing the financial system to operate as it has been, trading $3 trillion a day, is equivalent to 600,000 good, middle class jobs. Each and every day. This is how the financial system sucks the life blood out of the economy.

The more conservative thinkers are appalled at the idea that the monetary order that emerged post-collapse of Bretton Woods might be attacked, because living off of dipping a small cup in the Niagra Falls of finance is the only world they have ever known. . .

As for returning to Bretton Woods, understand that the system was not all that great. And we certainly do not want to return to a system of gold reserves, which severely constrains money creation, which must, in a sane policy regime, expand at pretty much the same rate as an economy's productive potential (not production, but productive potential) expands. In fact, there is a not insubstantial argument to be made that the Great Depression and both World Wars resulted from the City of London's attempts to restore itself as the center of restored international gold reserve systems.

Such a system involves choice of a number of parameters that would need to be negotiated by participants. First, there is choice of the target exchange rate. Second, there is the choice of size of the band in which the exchange rate could fluctuate. Third, there is a choice whether the band would be hard or soft. A hard band is automatically and decisively defended; a soft band is one that allows for marginal temporary deviations outside the band, while retaining a commitment to bring the exchange rate back within the band when market conditions are most conducive. Fourth, there is the choice of the rate of crawl. This involves determining the rules governing the adjustment of the target and band. Issues here concern the periodicity of adjustment, and the rule governing adjustment of the nominal exchange rate. . . .

Finally, rules of intervention to protect the target exchange rate need to be agreed upon. Historically, the onus of defending the exchange rate has fallen on the country whose exchange rate is weakening. This requires the country to sell foreign exchange reserves to protect the exchange rate. Such a system is fundamentally flawed because countries have limited reserves, and the market knows it. This gives speculators an incentive to try and “break the bank” by shorting the weak currency, and they have a good shot at success given the scale of low cost leverage that financial markets can muster. Recognizing this, the onus of exchange rate intervention needs to be reversed so that the strong currency country (the central bank whose exchange rate is appreciating) is responsible for preventing appreciation, rather than the weak currency country being responsible for preventing depreciation. Since the strong currency bank has unlimited amounts of its own currency for sale, it can never be beaten by the market. Consequently, once this rule of intervention is credibly adopted, speculators will back off, making the target exchange rate viable. Such a procedure recognizes and addresses the fundamental asymmetry between defending weak and strong currencies.

Thanks for this report, I read Mish everyday but missed this. Interestingly, I have this strange ‘approach avoidance’ conflict about him. His anti labor (unionism) is to my mind appalling. Not that I don’t have problems with unions. I’ve been in a couple and know the problems with them up close. But, Mish seems to think the way to economic recovery is to reduce all labor to the least common denominator. Apart from the ethics, what does that do to purchasing power and in turn the impact on the economy?

But, I digress. Nevertheless, he is a wealth of information on a wide range of economic topics and always a good read. Also, Calculated Risk got him started in blogging and links his blog. That’s a heck of a recommendation.

But, I digress. New Deal Democrat on the Bonddad blog has taken a couple of swipes at Mish and they seemed to me to be ‘cherry picking’ as is, it seems to me, NDD’s style. Once I responded to NDD on Mish, but I never read where Mish responded directly, although there were times that he seemed to respond obliquely. The very direct response to Bonddad in the headline no less is interesting.

Thank for bringing it to my attention

or something going on to spend hours and hours in comments denying economic statistics....

I consider SilverOz an econ troll frankly, as he seems to have never met a MNC lobbyist corporate policy he didn't like...

The post in question is good ole Bonddad, who is also busy worshiping at the church of "free" trade as well, in case you missed those lovely posts (with no data in the past I might note)....

I think the point is, this isn't the first time, not by a long shot, I've seen graphs misused by them, misinterpreted. I think that's a critical call out and probably the difference between your criticism and mine.

Mine is they are just plain wrong so often. Tom often comments on my graphs and asks why my graphs and their graphs are different...and I go into the Federal Reserve database, do a few tweaks to show why....but I mean I am sorry, not getting a differential is not an absolute, as a math head, drives me nuts...

Case in point was initial unemployment claims. Of course there was a dramatic upward slope after Q1 2009, but slope from a trough does not a trend make...it's like claiming you climbed Everest because you are out of a deep upward slope on 100 meters of the trek.

I believe Krugman called it. How is Estonia? The reason I mention Estonia is it was proclaimed to be the "economic miracle" due to all of the endorsement of our classic bad trade, "free market" "reforms" and were pointed to repeatedly when trying to blast any sort of socialism aspects to France, Nordic, U.K. etc policies and why of course they should be torn asunder.

After the next government payout, Fannie Mae’s borrowings will carry an annual dividend cost of $7.6 billion, which the company said it will repay by borrowing more money from the Treasury. “This amount exceeds our reported annual net income for all but one of the last eight years, in most cases by a significant margin,” the company said.

$7.6 Billion in dividends while they borrow tens of billions from taxpayers. That is just straight out theft.

I forget how many posts I've written about the GSE black bail out hole and on top of it, sure looks like they kicked the entire real estate market can down the road...

Yet these continual things get little "oh shit" press articles and then ...nothing happens.

I think my last tally is they are way bigger than TARP now in terms of risk and taxpayer liability.

I think it's because people just do not understand them...

might be time for one of those tutorial type overview posts?

This time by international economist Robert Scott and he's being way too kind.

Unfortunately he links to the economic fiction so I went and checked and it's just getting truly psycho. Claims that the trade deficit don't hurt U.S. manufacturing, that current and future bad trade policies are all good...

and lest we not forget our infamous "V" ....ya know the slope says jobs are just around the corner, a chicken in every pot!

(Bloomberg) -- Fannie Mae will seek $15.3 billion in U.S. aid, bringing the total owed under a government lifeline to $76.2 billion, after its 10th consecutive quarterly loss.

The mortgage-finance company posted a fourth-quarter net loss of $16.3 billion, or $2.87 a share, Washington-based Fannie Mae said in a filing yesterday with the Securities and Exchange Commission.

The GSE's are a gushing wound on the economy and no one seems to care.

"...but the problem is that the ruling class that benefits from the current system will never let that happen..."

And that assertion is almost certainly true as long as the ruling class is allowed to remain the ruling class. In my view, one best grasps the economic problem as an outcropping of a pre-existing political problem. If there were not first whores there would not follow johns, eh?

Our system is irremediable as a consequence of the ongoing symbiotic relationship between special interest lobbies and

the trollop politicians dependent upon them for their livelihood. All the big sis, Elizabeth Warrens in the world do nothing more than inspire the illusion that reform is actually possible. The remedy in such circumstances as it always has been is to be seen in recourse to massive demonstrations and economy paralysing strikes. The Polish example of the 1980s is instructive here. So corrupted are our structures that one need only kick in the door and the whole rotten edifice would come tumbling down. Imagine for a moment the personal courage of a botoxed, teeth whitened Joe Biden or Nancy Pelosi looking out upon a sea of angry faces as distant as the horizon. Such a "peoples' moment" is not without possibility, particularly so as our unemployment continues to intensify. It will be critical, however, to distinguish this "peoples' moment" from the brownshirt Tea Party counterfeit serving presently to funnel public discontent into the black hole of deficit hating, starvation inducing libertarianism. We need root and branch change, not a return of the Confederacy or membership in the Flat Earth Society.

So, let me guess....if "the economy turns for the worse" means just how many CDSes? How much toxic gambling debt is still left? Oops, but haircuts, which could have been imposed in bankruptcy....nary a possibility....and while we're focused in on the 100% payouts PLUS the acquisition of the underlying CDO by the various counterparties....

how much of this is left to go and of course, I'm sure there is no further negotiations for a hair cut right?

They've paid back about half of what they owe. However, there is another tiny condition about us getting that back.

As reported by other news operations, AIG said in a separate filing with the Securities and Exchange Commission that it would need more funding from taxpayers if the financial markets took a turn for the worse.

"Should certain of these risks emerge, AIG may need additional support from the U.S. government," the company said in the 10-K filing.

God, meanwhile, back at the Farm, the Fed, our Gov. bought and paid for Senate (esp.) Congress are just completely ignoring derivatives as if it all just doesn't exist.

What are chances for economic Armageddon redux and I do believe Las Vegas or some place should allow bets on it happening in a certain time window at this point.

Gee wiz, only $8.87 billion in a single quarter and how much money have we given to AIG? I lost count, I thought it was about $150 billion at this point. Have to go check my notes.

I remember that Bold Stroke well -- At the time, I saw a CIA report (TS of course) with the names of every American at the Canton trade fair. The memorable quote in the financial press "If we could sell aspirin to every Chinese." Not that the Chinese lack willow bark or pharmaceutical plants, but such was our delusion at the time.

The real "scandal" at the time was the outrage in the Pentagon and the moves to undermine the Nixon administration over it. We had Americans getting killed on the ground while our leaders made nice with Mao and Brezhnev. I still remember psyop leaflets with pictures of Nixon toasting with Mao and Brezhnev dropped on North Vietnam to undermine their confidence.

But our business leaders did not see it in that framework -- here was that huge market opening up. It was finally fashionable to wear Mao badges. They forgot that the Middle Kingdom had exported rea to Emgland, but needed nothing the British could export. They wanted silver -- hard money -- for their tea. Thus, the opium wars of the 19th century "to open up China for trade." China is finally getting even with the West.

Frank T.

“China is still pegging its currency which is destroying our manufacturing sector”

WOW! You have just gone head to head with Bonddad, New Deal Democrat and SilverOz. They have be trumpeting the ‘myth of American Manufacturing in decline'. I don’t know how to link but see one example: “No, Virginia, US Manufacturing Isn’t Dead” -Bonddad 2/23/2010. I hope you would comment.

I periodically read him but I keep trying to keep the middle column RSS feeds on people who are consistently accurate vs. some sort of economic religious view, as you noted, that claim of somehow the entire world must return to serfdom to "maximize the economy" mantra.

But that entire "call out" stuff, well, in my view if you're going to do that a lot....you had better your own backyard spotless and well....

uh, about that "V" jobs growth....

;)

But overall Mish is reasonably accurate and insightful, but we're the layperson's blog, the working stiff, the middle class, so obviously helping promote various people who really would like to wipe it out...well, that's why they aren't in the middle column...

But I am finding some of the weirdest "blind spots" in almost every economic category as of late. Someone will be dead on in one area, say derivative reforms or global finance...and then you'll find pure economic fiction in say something like trade or labor econ. Very weird.

It's embedded in this Friday Night Video

It's a talk by Ha-Joon Chang on what a fallacy "free trade" rhetoric really is, by history.

(second video in the list)

Not only that and it's really an Economist's in depth talk...

Chang is a SCREAM funny! I mean Professional Comedian level funny so, this isn't your typical dense, dry Academic talk.

Maybe I should do Friday Movie Night reruns? It's really good as well as backs up your graphs.

Hey man, history, statistics r us! ;)

Minsky, Carey, etc. There are plenty of people who predicted the situation we've gotten into, but only the Chicago School of Economics is being taught. Since the Chicago School is so flawed, no one can imagine the solutions.

For instance, arguing against "Free Trade" is practically useless because it has become a religious issue rather than a scientific one. Even so-called progressives, like Bonddad and Krugman won't go against the Free Trade canon.

Back around 1992 or so, when the web was relatively new, there was a professor in the Netherlands who had started a project on U.S, history using the new mark-up language of HTML. I was the person who added an article on Henry Carey, and added a series of long quotes from most of the chapters of Carey's 1851 book The Harmony of Interests: Agricultural, Manufacturing & Commercial.

In the early 1990s, I used the Bicentennial Statistical Abstract - Colonial and Historical Statistics, to plot out steel production, railroad mileage built, and coal production, against the various tariff regimes in the 1800s to 1920s. The results were very stark: low tariffs are strongly correlated with downturns in real production, and high tariffs are strongly correlated with increased in real production. Exactly like Henry Carey, wrote in the mid-1800s. These are the charts I generated back (God, do I miss QuattroPro - trying to edit Excel graphics suck by comparison, even now, nearly two decades later)

, scanned from the clippings of my articles.

Carey explained that the ability to import is based on the ability to pay. The ability pay, in turn, is based on the earning power of the nation’s workforce. If the workforce has to compete against cheaper labor in other countries, then its earning power will be diminished. Carey even anticipated the situation we find ourselves in today, noting in his time that as earning power diminished, the U.S. must buy imports on credit, creating a bubble of indebtedness that must sooner or later burst. Unfortunately, the person who discussed the American System a lot back then when I was writing was Lyndon LaRouche. But, in the late 1980s, James Fallows went to Korea and Japan to write about why their economies were doing so much better than the U.S.'s. The Koreans and Japanese gave him an earful of American history, including Carey, List, and E. Peshine Smith (Smith being the economist, I believe, who introduced American System thinking to the Japanese, which formed the basis for the period unfortunately called the Meiji Restoration, when Japan began to "copy" Western industrialization. In actuality, the Japanese were implementing the nation-building programs Alexander Hamilton had elaborated as Secretary of the Treasury. Fallows laid all this out in a great series of articles in The Atlantic. I suspect, but don't know for sure, that it was Fallows' articles that were picked up up Michael Lind, who is now one of the most vocal proponents for a return to American System policies. See especially Lind's 1997 book, Hamilton's Republic: Readings in the American Democratic Nationalist Tradition

(You see, Mr. Oak, I was never able to fully grasp the mathematical side of modern economics, but I was able to pick up a lot from economic and industrial history!)

What is important to note is that the traditional opponent of the American System, the laissez faire of the British East India Co., (which was formulated almost solely to justify the moral depravity of Britain's opium trade with India and China), was repackaged by Milton Friedman and sold to Americans as "freedom to choose."

A particularly important book to read, for anyone who wants to understand more about the actual economic policies that created the United States, is The Great Challenge: The Myth of Laissez-Faire in the Early Republic, by Frank Bourgin. Interestingly, Bourgin's book is his 1940s PhD dissertation, which was rejected by the University of Chicago. Bourgin published the book in the 1980s after being encouraged hy historian Arthur Schlesinger Jr.

I hve an underwater mortgage I borrowed "from Suntrust," but it turns out that it was then actually owned by Fannie Mae. I could solve part of Fannie Mae's problem by buying this "underwater" mortgage at its present value. In fact, there are many of us who could provide relief for Fannie's cash-short problem -- they get rid of the toxic "default risk" and reduce their cost at the same time. Hey Fannie, who is the person to talk to about this financial innovation?

Frank T.

of wealth. The one you usually hear about from liberals and progressives is the "tax cuts for the rich." Conservatives retort that hardly anybody with less than 25,000 or so in income pay taxes. That's only true in so far as federal income taxes. When you look at the variety of other taxes, from FICA at the federal level down to state and local property and retail taxes, the tax structure in the U.S. is actually highly regressive.

The other mechanism hardly anyone talks about is the burden of usury, speculation, and economic rent seeking behavior imposed by the financial system. The $25 billion Goldman Sachs dispensed in bonuses has to come from somewhere. This year, of course, it came directly from the taxpayer in the form of bailouts. But in previous years, this money would come out of the hide of the rest of the population whose incomes and benefits were held down in order to "meet Wall Street expectations." This mechanism is discussed from the perspective of the investor class by Warren Buffet in his little story about the Gotrocks family and what they pay for financial advice. But the more correct perspective is breathtakingly captured in the Frontline May 2006 story Can You Afford to Retire?, in the segment about the bankruptcy of United Airlines. While the employees of United lost almost all their pension, "The banks, with their superpriority, got back every penny plus interest, plus tens of millions of dollars in fees." You have to watch the video to get the full impact of former J.P. Morgan executive Repko has he smiles smugly and admits that, yes, JP Morgan got every penny it asked for.

Similarly, wealth is transferred by the fees and profit margins generated by the enormous amount of financial trading. Two years ago, I created the Wikipedia page on financialization with a table showing financial turnover compared to gross domestic product. This is work I first did in the early 1990s. In the 1960s, it took all financial markets about nine months to trade the dollar volume equivelent to one year of GDP. Today, it takes about three days.

How much does it cost our economy to move around this much financial paper each and every day? Let us assume that the fees, commissions, and so on paid to the financial system for all this frenetic activity amount to one percent. (An October 2003 study conducted by John P. Hussman, President of Hussman Investment Trust, found that the costs to the funds he manages actually amounted to approximately 1.87%; scroll down to the bottom.)

So, one percent of three trillion a day is $30 billion in commissions / fees / bonuses, etc., paid to the financial system for all that paper being shoved around. That's the amount that is going to all those people like the guys in the Chicago futures pits standing behind CNBC's Rick Santelli you saw last month.

$30 billion a day is the equivalent of 600,000 (six hundred thousand) jobs paying $50,000 a year.

That is, the cost to the economy of allowing the financial system to operate as it has been, trading $3 trillion a day, is equivalent to 600,000 good, middle class jobs. Each and every day. This is how the financial system sucks the life blood out of the economy.

One of Stirling Newberry’s best zingers was that

As for returning to Bretton Woods, understand that the system was not all that great. And we certainly do not want to return to a system of gold reserves, which severely constrains money creation, which must, in a sane policy regime, expand at pretty much the same rate as an economy's productive potential (not production, but productive potential) expands. In fact, there is a not insubstantial argument to be made that the Great Depression and both World Wars resulted from the City of London's attempts to restore itself as the center of restored international gold reserve systems.

Former AFL-CIO economist Thomas Palley suggested a scheme of crawling band target zones to replace the complete, unregulated chaos we have today in foreign exchange markets, in The Fallacy of the Revised Bretton Woods Hypothesis: Why Today’s System is Unsustainable and Suggestions for a Replacement.

Thanks for this report, I read Mish everyday but missed this. Interestingly, I have this strange ‘approach avoidance’ conflict about him. His anti labor (unionism) is to my mind appalling. Not that I don’t have problems with unions. I’ve been in a couple and know the problems with them up close. But, Mish seems to think the way to economic recovery is to reduce all labor to the least common denominator. Apart from the ethics, what does that do to purchasing power and in turn the impact on the economy?

But, I digress. Nevertheless, he is a wealth of information on a wide range of economic topics and always a good read. Also, Calculated Risk got him started in blogging and links his blog. That’s a heck of a recommendation.

But, I digress. New Deal Democrat on the Bonddad blog has taken a couple of swipes at Mish and they seemed to me to be ‘cherry picking’ as is, it seems to me, NDD’s style. Once I responded to NDD on Mish, but I never read where Mish responded directly, although there were times that he seemed to respond obliquely. The very direct response to Bonddad in the headline no less is interesting.

Thank for bringing it to my attention

or something going on to spend hours and hours in comments denying economic statistics....

I consider SilverOz an econ troll frankly, as he seems to have never met a MNC lobbyist corporate policy he didn't like...

The post in question is good ole Bonddad, who is also busy worshiping at the church of "free" trade as well, in case you missed those lovely posts (with no data in the past I might note)....

I think the point is, this isn't the first time, not by a long shot, I've seen graphs misused by them, misinterpreted. I think that's a critical call out and probably the difference between your criticism and mine.

Mine is they are just plain wrong so often. Tom often comments on my graphs and asks why my graphs and their graphs are different...and I go into the Federal Reserve database, do a few tweaks to show why....but I mean I am sorry, not getting a differential is not an absolute, as a math head, drives me nuts...

Case in point was initial unemployment claims. Of course there was a dramatic upward slope after Q1 2009, but slope from a trough does not a trend make...it's like claiming you climbed Everest because you are out of a deep upward slope on 100 meters of the trek.

I believe Krugman called it. How is Estonia? The reason I mention Estonia is it was proclaimed to be the "economic miracle" due to all of the endorsement of our classic bad trade, "free market" "reforms" and were pointed to repeatedly when trying to blast any sort of socialism aspects to France, Nordic, U.K. etc policies and why of course they should be torn asunder.

It's his pet theory and he doesn't want to give it up.

He's got a point, but his wedded to it so hard that he can't see anything else.

$7.6 Billion in dividends while they borrow tens of billions from taxpayers. That is just straight out theft.

I forget how many posts I've written about the GSE black bail out hole and on top of it, sure looks like they kicked the entire real estate market can down the road...

Yet these continual things get little "oh shit" press articles and then ...nothing happens.

I think my last tally is they are way bigger than TARP now in terms of risk and taxpayer liability.

I think it's because people just do not understand them...

might be time for one of those tutorial type overview posts?

This time by international economist Robert Scott and he's being way too kind.

Unfortunately he links to the economic fiction so I went and checked and it's just getting truly psycho. Claims that the trade deficit don't hurt U.S. manufacturing, that current and future bad trade policies are all good...

and lest we not forget our infamous "V" ....ya know the slope says jobs are just around the corner, a chicken in every pot!

They should rename the site Hooverville.

The bailouts of the GSE's continue.

The GSE's are a gushing wound on the economy and no one seems to care.

"...but the problem is that the ruling class that benefits from the current system will never let that happen..."

And that assertion is almost certainly true as long as the ruling class is allowed to remain the ruling class. In my view, one best grasps the economic problem as an outcropping of a pre-existing political problem. If there were not first whores there would not follow johns, eh?

Our system is irremediable as a consequence of the ongoing symbiotic relationship between special interest lobbies and

the trollop politicians dependent upon them for their livelihood. All the big sis, Elizabeth Warrens in the world do nothing more than inspire the illusion that reform is actually possible. The remedy in such circumstances as it always has been is to be seen in recourse to massive demonstrations and economy paralysing strikes. The Polish example of the 1980s is instructive here. So corrupted are our structures that one need only kick in the door and the whole rotten edifice would come tumbling down. Imagine for a moment the personal courage of a botoxed, teeth whitened Joe Biden or Nancy Pelosi looking out upon a sea of angry faces as distant as the horizon. Such a "peoples' moment" is not without possibility, particularly so as our unemployment continues to intensify. It will be critical, however, to distinguish this "peoples' moment" from the brownshirt Tea Party counterfeit serving presently to funnel public discontent into the black hole of deficit hating, starvation inducing libertarianism. We need root and branch change, not a return of the Confederacy or membership in the Flat Earth Society.

So, let me guess....if "the economy turns for the worse" means just how many CDSes? How much toxic gambling debt is still left? Oops, but haircuts, which could have been imposed in bankruptcy....nary a possibility....and while we're focused in on the 100% payouts PLUS the acquisition of the underlying CDO by the various counterparties....

how much of this is left to go and of course, I'm sure there is no further negotiations for a hair cut right?

They've paid back about half of what they owe. However, there is another tiny condition about us getting that back.

God, meanwhile, back at the Farm, the Fed, our Gov. bought and paid for Senate (esp.) Congress are just completely ignoring derivatives as if it all just doesn't exist.

What are chances for economic Armageddon redux and I do believe Las Vegas or some place should allow bets on it happening in a certain time window at this point.

Gee wiz, only $8.87 billion in a single quarter and how much money have we given to AIG? I lost count, I thought it was about $150 billion at this point. Have to go check my notes.

I remember that Bold Stroke well -- At the time, I saw a CIA report (TS of course) with the names of every American at the Canton trade fair. The memorable quote in the financial press "If we could sell aspirin to every Chinese." Not that the Chinese lack willow bark or pharmaceutical plants, but such was our delusion at the time.

The real "scandal" at the time was the outrage in the Pentagon and the moves to undermine the Nixon administration over it. We had Americans getting killed on the ground while our leaders made nice with Mao and Brezhnev. I still remember psyop leaflets with pictures of Nixon toasting with Mao and Brezhnev dropped on North Vietnam to undermine their confidence.

But our business leaders did not see it in that framework -- here was that huge market opening up. It was finally fashionable to wear Mao badges. They forgot that the Middle Kingdom had exported rea to Emgland, but needed nothing the British could export. They wanted silver -- hard money -- for their tea. Thus, the opium wars of the 19th century "to open up China for trade." China is finally getting even with the West.

Frank T.

Pages