I wrote the story below in response to an outrageous trick Congress just tried to play on the public. As many of you know, the Senate passed 0/congress/bills/111/hr3808/text">HR 3808 The Interstate Recognition of Notarizations Act of 2010 unanimously on September 27. The bill was a carefully crafted, stealth "silver bullet" for the big banks to deal with their increasing legal problems with foreclosures. President Obama exercised a "pocket veto," which means he let it die after Congress adjourned. (Image)

While my story focused on the process and contempt shown to citizens by Congress in that process, I became aware of a much broader issue. We may well be on the verge of a real estate value meltdown as a result of very bad behavior, illegal in many cases, by the big banks combined with the legitimate push back of mortgage holders.

If banks can't foreclose and people can do a strategic default and walk away (0r live free in their residence), what will happen to real estate values?

The larger question emerged in reviewing bank bad behavior.

If there are fundamental flaws in many, maybe most mortgage, flaws of a serious legal nature, what if a strategic default movement spreads beyond just those facing foreclosure? That's where Armageddon comes in

The bill, HR 3808, is short and sweet. It allows banks to use interstate notarization's to validate title and loan documents. Seems simple until you realize that state law prevails in real estate purchases. In just a few minutes, Senator Richard Casey (D-PA) got this bill that would change all that passed unanimously, a bill that would negate established law in the 50 states. Casey also made sure there was no debate and no roll call vote.

When I posted the article on The Agonist, there was a very lively commentary. Replies often amplify and extend original posts in ways that are very productive. The replies I'll quote here concern implications of the stall in foreclosures and questions about mortgage contracts and the legal nature of what's been done. The full comments are worth reading but I'll excerpt.

Before that, it's critical to understand one fact about the approval of these bills. This wasn't some vote that was poorly understood by members or that was off the radar of of the House and Senate leadership. They know exactly what to do - pass the bill quietly and without any investigation or debate. They knew this for one of two reasons: 1) the big bank lobbyists told them exactly what to write and when to pass it or 2) they thought it up all on their own. Of course, it's one. The leadership got the call from the banks and the members were told mum's the word. It was all about obedience to the ultimate authority in Congress - big money and the people who control it.

Real Estate Armageddon: What the foreclosure stall and legal problems with mortgages mean.

This reply pretty much sums it up.

What matters is that this emerging mortgage mess is a revolutionary moment in American history. What gets done next to resolve this full stop economic meat grinder is going to be a defining moment for us all.

The housing market is about to stop dead. No sales, no foreclosures, no more reason to pay a mortgage. The whole thing revealed to be a monumental con job, out in the open.

When the housing market stops, the economy stops.

So the government HAS TO ACT to keep things moving, no matter what that means, no matter what it takes. That's what is coming next.

The government HAS TO ACT to see that mortgages continue to be paid off by homeowners --

- no tsunami of strategic defaults,

- no Mortgage Rebellion where everyone stops paying,

- no stopping the foreclosure epidemic,

- no cramdowns or admission that these mortgages are junk,

- no letting banks too big to fail up and fail,

and if the American housing market is not kept on its rails, the entire economy will come off the track and freeze up solid. No one will have any reason to pay their monthly if there is no effective foreclosure process, if there is no hope of holding equity in the structure or property. Antifa - The Agonist

Let's take Antifa's argument as a given. The assumption is that Congress and the banks along with the executive branch will be able to do something about it. That's where my serious pessimism comes in. The banks crated the problem through reckless disregard and a blinding greed. Congress compounded the problem by keeping the banks alive. The banks and Congress made sure there was nothing done in 2008 on foreclosure relief, when a chance existed to mitigate much of this.

These people lack the ability to devise a path out of this mess, one that would prevent the economy from unraveling. They've demonstrated that. In addition, the banks and Congress are and will remain in power through the duration of this crisis. That's a deadly combination - stunning ineptitude and perpetual power.

Poster Antifa provides a list of bad behavior on the part of the banks and enabling by Congress and regulators (one of whom is now Secretary of the Treasury). The segment below makes clear the relative blame for the crisis:

Those many, many persons who should never have gotten a mortgage loan from anyone, under any circumstances -- and this is several million people, apparently -- received them only because the originating banks aggressively committed three criminal acts of fraud:

1. Creating varieties of mortgages that no sane banker had ever considered before and pushing them on the real estate market. Liar's Loans of a dozen different kinds aggressively sold to real estate brokers. The brokers didn't come up with these mortgages, in fact, they were appalled until they saw how much money they could rake in by looking the other way.

2. Willful failure to perfect the security interest -- banks are required to audit every loan and make sure those people do have that income, the house does have clear title, there was a building inspection, and it was appraised accurately, and a bunch of other legal touchpoints. Only after confirming all this can a bank sell or offer the loan as an investment instrument. This perfecting the security interest was not done at all -- at all -- by the issuing banks.

3. These fraudulent mortgages were tranched and sold to investors as quality instruments, when virtually all of them were missing material information, were falsely issued, were outright lies and fraud, and should have been rescinded the moment an auditor took a look at them. But no auditor ever did. That was specifically discouraged and prevented. Antifa - The Agonist

How do we get out of the crisis when those who created it, the banks and government, engaged in what is both horrible business and activity that deserves investigation and prosecution?

I have no idea.

(These writers have covered the specifics and implications of the current crisis: Tyler Durden, Karl Denninger, & Numerian)

====================

(This is the full article concerning the absolute underhanded behavior by the entirety of the U.S. Senate present when the unanimous voice vote approved this and those House members who passed the bill this back in April. It's that bipartisan coalition with its Republican and Democratic wings that always operates in the interest of The Money Party.)

Why Does Congress Hate America?

Originally posted at The Agonist

Michael Collins

Oh, it's just that Collins guy mouthing off again.

Actually, I was far too easy on Congress yesterday in Lawless Nation - Congress.

Here's why: 0/congress/bills/111/hr3808/text">HR 3808 The Interstate Recognition of Notarizations Act of 2010

The bill is the response to the events outlined in a story that Numerian scooped on foreclosure problems. The banks are in big trouble. They failed to follow the law and rules in handling mortgages. Instead of foreclosing on home owners, those upside down and under water can consider strategic defaults on the mishandled notes. Legal efforts have reached a point where there's a "tsunami of legal action against mortgage servicers" as Tyler Durden calls it.

A clever Mandarin somewhere figured out that by changing the law on notarizations, after the fact, Congress could stop the tsunami by "making it more difficult for homeowners to challenge foreclosure proceedings against them." (See Ellen Brown)

HR 3808 passed both houses of Congress with ease. How? (See "Major Actions") On April 27, it passed the House by a voice vote. On September 27, it passed the Senate unanimously. It took just minutes for the bill to pass in both chambers. Things move right along when there's no debate.

It was more important for Congress to fix things for the bankers than to keep constituents in their homes in the midst of a relentless financial crisis, as a cold winter approaches. Congress has inherent contempt for the people. We're probably not even important enough to hate.

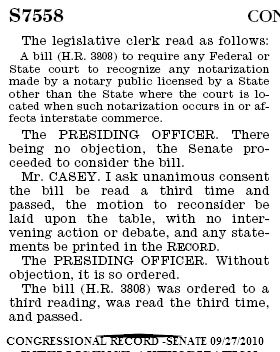

Here's the Smoking Gun

The bill originated in the House and passed without debate on April 27. It had a Republican sponsor and three cosponsors for a split two Republicans and two Democrats. The House version of the bill was sent to the Senate months ago. It sat dormant in the Senate Judiciary Committee until things got dicey and strategic defaults emerged as a real possibility due to rule breaking on a massive scale in the mortgage industry.

As if by magic, the bill emerged from committee and was passed unanimously by the United States Senate.

From the Congressional Record - a Smoking Gun for the Big Fix

Leahy let the bill out of his committee. Casey was the bag man. But everyone from top to bottom in both chambers was in on it. Hold them all accountable. Can you imagine any Republican stopping it? Would Senate Finance Chair, Chris Dodd, (D-CT) have stopped it? Where was Rep. Barney Frank (D-MA) when this beast was born in the House?

"… with no intervening action, and any statement be printed in the Record."

This is how they cover their tracks creating plausible deniability, to use a DC term. The people don't deserve a debate and, come to think of it, Mr. Casey may have thought, they don't even deserve a written record. We're just the chumps, the pawn to be moved around the chess board of their strange world so disconnected from reality.

Winners and Big Losers

Lets start with the losers first.

Big Losers: Every member of the U.S. House of Representatives who knew about this bill and failed to object; the Speaker of the House; and, the majority and minority leadership. And, of course, the sponsor and three co-sponsors of HR 3808: sponsor, Rep. Robert Alderholt (R-AL) and co-sponsors Representatives Bruce Braley (D-IA), Michael Castle (R-DE), and Artur Davis (D-AL).

Big Losers: Every member of the United States Senate who knew about this bill and failed to object plus the majority and minority leadership. Special mention goes to Senator Patrick Leahy (D-VT), Chairman of the Senate Judiciary Committee for letting the bill go and Sen. Robert Casey (D-PA), who introduced the bill for passage without cmment and without any statements on the Record. Casey made sure that the bill passed unanimously.

Winner: Numerian for the best comprehensive analysis of the failure of foreclosures and emergence of strategic defaults in The Devil's in the Details plus the cadre of financial bloggers who flesh out these stories.

Winner: President Barack Obama who did a pocket veto of this bill thus killing it for the time being. Well done!

Winner: White House blogger Dan Pfeiffer who explained the president's pocket veto. After diplomatically stating why the bill was nixed, Pfeiffer said, "The authors of this bill no doubt had the best intentions in mind when trying to remove impediments to interstate commerce." White House Blog Oct 7 Irony with a tinge of condescending sarcasm. Well done!

Watch for the sequel, Re-Animator II - How Congress Tries Again to Save the Big Banks.

END

HR 3808 and Summary of Major Actions

This article may be reproduced in whole or in part with attribution of authorship and a link to this article.

Comments

slicky tricky

Honestly, glad you looked at this because I didn't analyze it, but that's what Congress thinks their job is, to slip in very dense legislation, corporate lobbyists demands that no one figures out until at least the bill is signed into law, if not a couple of years later.

This will get very ugly, very soon

The story of this bill is too good to pass up and MSM was already on the foreclosure/strategic default story a week or so ago. The activities of the banks sound outright criminal. How do you sell another bailout or even help for the banks as that emerges.

I decided not to post 'Why Does Congress Hate America' at EP since it didn't have enough of an economics spin (plus I didn't want you to know how populist I really am;). But it fits now, particularly with the economic implications.

If this was the bank fix it bill for a lot of this mess, they're in more trouble than I've imagined.

Michael Collins

Populist rants and raves

are good for the site, as long as the data/stats/facts are cited and accurate.

I'm pretty "geeky" myself, thinking mathematical equations and graphs scream "they are f&*kin! ruining this nation and destroying the globe!" by themselves.

;)

Well, while Geithner sings praises on TARP, to me they simply funneled the funds around and now it's the Fed, Fannie/Freddie holding the taxpayer bag.

Either way on this, to me, all trying to avoid prices going down back to levels people can afford the houses is a losing proposition. I think they could have bought everyone a 2000 sq. ft house in America for the amount of money that has gone into the entire mess.

A house in every driveway

What a deal that would have been. It will take some brilliant financial and political thinking to devise a solution to this problem. This bill was a dirty trick to devise a solution for the banks only. That's what stopped Obama from signing it, in addition to any other motives. The real estate market can't collapse, unless we're looking for total chaos. At the same time, the banks have to be punished for their illegal behavior and the people need help with foreclosure relief (which Congress wouldn't approve even with 60 Democrats!).

FDR's approach in his first term would do.

Michael Collins

State Mortgage Laws

Bottom line is that we have a different mortgage system in every state. One reason none of this was done before is that investors are not stupid. To create the ponzi scheme to enrich themselves, the crooks needed a complex system no one, including themselves, seems to have understood. Their profits quickly went into their private bank accounts. State courts will be the deciders in this mess. Even a notary system that applies to all states simply means the notary signed trash. Who owns the note? Who receives the payments? Can the "chain of title" be traced within the state records? The same flunkies who created the bad mortgages sometimes writing them using straw buyers (I have seen this) are running the mass foreclosure scams.

No one would have funded these mortgages if they knew what they were doing. This follows the S&L crises from the "license to steal" law done by Reagan. The scams in CA from energy deregulation including Enron. Better believe they will sweep this under the rug if they can with the help of a corrupt legislature. My bet is that it is too big and too stupidly done for a quick fix.

like the law itself?

Try collecting on any civil action and try getting any financial justice. There is none, except for the attorneys, the costs are excessive and even when you win, that is just the start of the collections process.

It's all a beyond belief rigged game, all for attorneys in my view.

No surprise mortgage companies would be right in therer, front and center, out to extract more fees and games from Joe Blow citizen Q.

Ponzi schemes

Excellent elaboration! I'll bet with you - this is too big, by a long shot, to sweep under the carpet.

Obama had to veto this piece of garbage bill but that doesn't get him and the rest of us off the hook to mitigate incomprehensible damage in store if there isn't a solution for this.

My analysis and reading of history, particularly since 2000, is that the people in charge and their minions are too damn dumb to solve this in a way that will both work and provide a degree of equity and justice for those who got screwed (not the flippers or scam artists, the everyday citizens who thought they were making an investment they'd be able to pay off).

Michael Collins