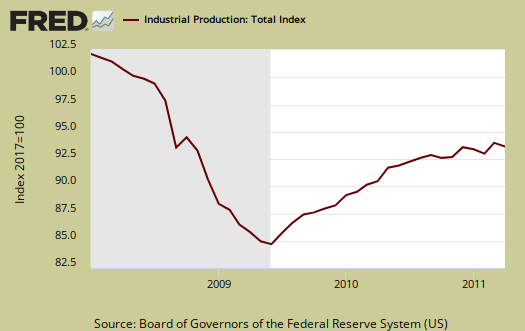

The Federal Reserve's Factory Production report shows a no change for April 2011 Industrial Production, or output for factories and mines. Manufacturing industrial production alone dropped 0.4% for April. Here is their detailed report. March was revised one percentage point lower to 0.7% and February had a 0.3% decrease in industrial production. Industrial Production is still down 6.9% from pre-recession levels.

Industrial production was unchanged in April after having increased 0.7 percent in March. Output in February is now estimated to have declined 0.3 percent; previously it was reported to have edged up 0.1 percent. In April, manufacturing production fell 0.4 percent after rising for nine consecutive months. Total motor vehicle assemblies dropped from an annual rate of 9.0 million units in March to 7.9 million units in April, mainly because of parts shortages that resulted from the earthquake in Japan. Excluding motor vehicles and parts, factory production rose 0.2 percent in April. The output of mines advanced 0.8 percent, while the output of utilities increased 1.7 percent. At 93.1 percent of its 2007 average, total industrial production was 5.0 percent above its year-earlier level. The rate of capacity utilization for total industry edged down 0.1 percentage point to 76.9 percent, a rate 3.5 percentage points below its average from 1972 to 2010.

Major industry groups breakdown of industrial production.

- Manufacturing: -0.4%

- Mining: +0.8%

- Utilities: +1.7%

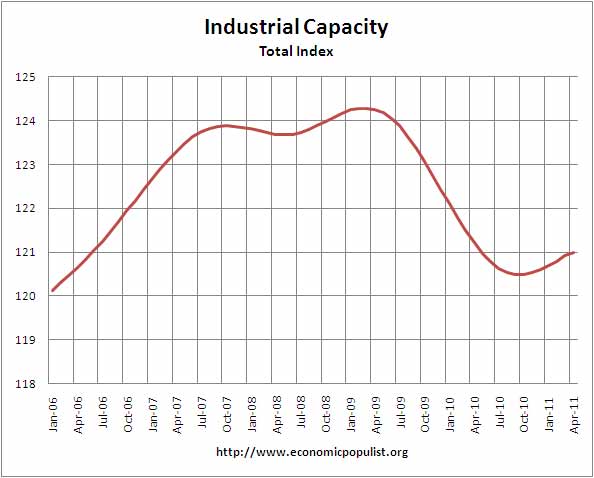

Below is the graph of raw capacity, indexed against 2007 output. This is just how much capacity does the U.S. have to make stuff. Look at how total capacity has declined for the first time in the historical data. This index represents the raw facilities, potential to make stuff. Raw capacity is the underlying number by which utilization is calculated.

Below is the Fed's description of Market groups from the report and their monthly percent changes. Consumer durable goods had a dramatic drop as did automotive, 7%. Overall the report shows a slowing of output, in line with other economic indicators and reports. We also are finally seeing the effects of the Japan disaster on global supply chain.

The production of consumer goods decreased 0.7 percent in April because of weakness in the output of consumer durable goods. The index for consumer durable goods fell 4.4 percent, while the index for consumer nondurables rose 0.3 percent. Within the durables category, the output of automotive products dropped 7.0 percent, and the output of appliances, furniture, and carpeting fell 4.2 percent. The index for miscellaneous consumer durables recorded a decrease of 0.2 percent, while the index for home electronics increased 0.7 percent. The output of non-energy nondurable goods rose 0.6 percent, with gains in all of its main components. The output of consumer energy products declined 0.5 percent.

The index for business equipment fell 0.4 percent in April following a loss of 0.5 percent in March. Within business equipment in April, the output of transit equipment decreased 3.6 percent as a result of the large drop in motor vehicle assemblies; the production of most other types of transit equipment, particularly civilian aircraft, advanced substantially. The index for industrial and other equipment gained 0.7 percent, while the index for information processing equipment was unchanged. Despite a second consecutive monthly decrease in business equipment, the index in April was 9.9 percent above its level 12 months earlier.

The production index for defense and space equipment was unchanged in April after decreasing 0.3 percent in the previous month. Output in April was 1.4 percent above its year-earlier level.

Among nonindustrial supplies, the output of construction supplies declined 0.1 percent in April. This index has risen 3.0 percent since April 2010 but remains well below its pre-recession peak. The production of business supplies increased 0.7 percent in April following a similarly sized gain in March. Within business supplies in April, the index for commercial energy advanced 0.6 percent, and the index for non-energy business supplies moved up 0.7 percent---its sixth consecutive monthly increase.

The output of materials to be processed further in the industrial sector rose 0.3 percent in April after increasing 0.9 percent in March. The output of durable materials declined 0.4 percent in April; a drop of 5.4 percent in consumer parts---primarily motor vehicle parts---more than offset an increase of 0.9 percent in equipment parts. The output of nondurable materials edged up 0.2 percent after increasing 0.5 percent in March. In April, among nondurable materials, a sizable increase in textile production and a small gain in chemical production more than offset a decrease in the output of paper. The index for energy materials moved up 1.1 percent, with similarly sized increases in primary energy and converted fuel.

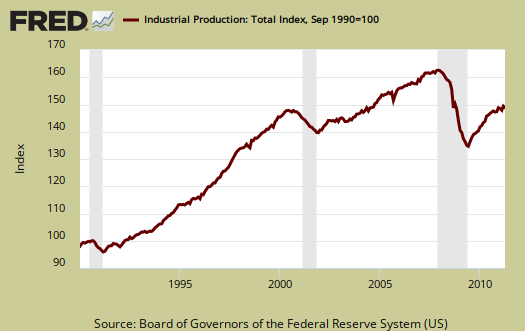

Below is another graph of industrial production since September 1990, indexed to that month. Look at the slope, the growth through the 1990's and then compare to 2000 decade. It was in 2000 when the China trade agreement kicked in and labor arbitrage of engineers, advanced R&D, I.T., STEM started in earnest.

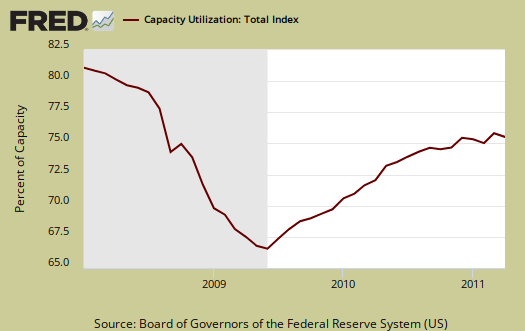

Capacity utilization, or of raw capacity, how much is being used, for total industry is now 76.9%. But the Fed notes this is 3.5 percentage points below the average from 1972 to 2010, 80.4%. Manufacturing capacity utilization is down 0.6% for the year.

Below are capacity utilization's monthly percent change breakdown.

- manufacturing: -0.4%

- mining: +0.3%

- utilities: +1.2%

- selected high-technology industries: +0.5%

- crude: +0.4%

- primary: +0.1%

- finished: -0.5%

The below graphs show the overall decline of U.S. capacity utilization. Capacity utilization is how much can we make vs. how much are we currently using. These graphs show the U.S. is simply not producing what it is capable of, a reflection of the output gap. Note, this index is normalized to a specific year, currently from most reports, the 2007 yearly average (see year in the graph). Therefore, one cannot take absolute values of capacity utilization, i.e. 80%, and claim this is an indicator of a healthy economy, for it all depends on what year capacity utilization is normalized to. One can take the slope, or rate of change from the peak of a recession and determine recovery, but again, these percentages are relative, they are not absolute ratios to a static point in time. Also recall utilization is a percentage of real total capacity. Notice that total capacity in the United States has declined.

According to the report, manufacturing uses 77.8% of capacity, utilities 10.4% and mining 11.8%.

Below is the Manufacturing capacity utilization graph, normalized to 2007 raw capacity levels, going back to the 1990's. Too often the focus is on the monthly percent change, so it's important to compare capacity utilization to pre-recession levels and also when the economy was more humming.

Here are some more details on industrial production categories (market groups) from the Federal Reserve's report:

If you are baffled by what crude, finished mean, read these stages of production definitions.

The Federal Reserve releases detailed tables for more data, metrics not mentioned in this overview.

Recent comments