Personal Income and Outlays for January 2010 was released today.

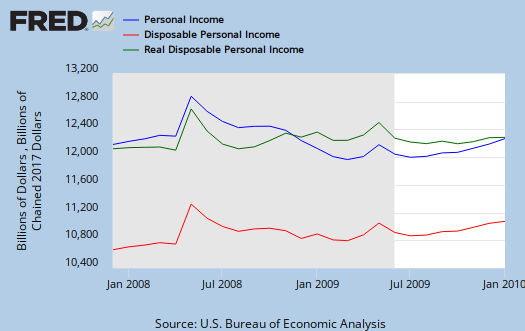

Personal income increased $11.4 billion, or 0.1 percent, and disposable personal income (DPI) decreased $47.6 billion, or 0.4 percent, in January.

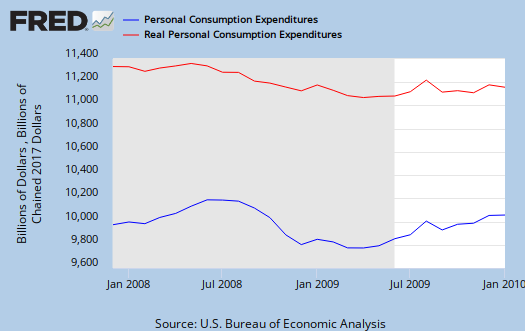

The decrease in DPI reflected an increase in federal nonwithheld income taxes. Personal consumption expenditures (PCE) increased $52.4 billion, or 0.5 percent. In December, personal income increased $41.2 billion, or 0.3 percent, DPI increased $40.3 billion, or 0.4 percent, and PCE increased $26.4 billion,or 0.3 percent, based on revised estimates.

Real disposable income decreased 0.6 percent in January, in contrast to an increase of 0.2 percent in December. Real PCE increased 0.3 percent, compared with an increase of 0.1 percent.

Also, minus transfer payments real personal income is down -0.2% (table 5). Below is Personal Consumption, so we can see income is flat yet consumption increased. Of that, energy was 2.9%. PCE minus spending on energy goods and services was flat.

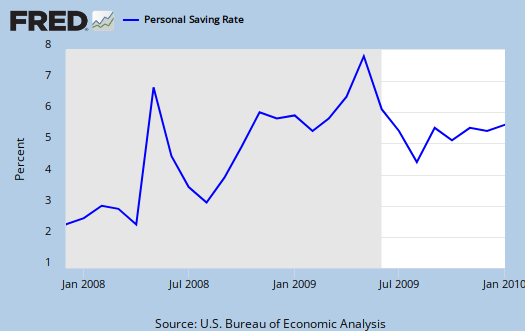

Personal saving as a percentage of disposable personal income was 3.3 percent in January, compared with 4.2 percent in December.

So, what does all of this mean? People are broke, using their savings to pay for increased energy related costs is my take. Also, this is yet more evidence relying on the grand consumer is a tapped out stimulus plan for economic growth. On the farmers income hammering of a -7.9% drop, this also includes inventory and capital.

Others with more observations, analysis, please comment. An example, in table 3, personal current transfer receipt, we have "other". What exactly is "other"? I'd personally like to find a better breakdown in income and wealth, to see where it all is actually coming from to gain more insight.

Subject Meta:

Forum Categories:

| Attachment | Size |

|---|---|

| 97.94 KB |

Yikes

Imagine if we didn't have the meager social safety net we have now.

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

Let me just add

it was those damn commie policies of FDR and New Deal that saved from having NO income growth.

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

well

this report is kind of bland actually, I kind of put what I could determine from it....that consumption, i.e. the plastic laden consumer isn't coming back and the reason savings went down is people are having to pay higher gas, energy bill...

what bothers me is I cannot find some really good raw data from our lovely gov. to show the breakdown and loss of wealth, retirement, income, for the middle class.

If someone knows where those details are hiding, i.e. overall income is $40k retirement savings now equals 0%, income = $500k, wealth = $1.2M, income for $28k, debt=$40k and so on. We know it's there!

The person I recall having

The person I recall having the most of that was Elizabeth Warren in her Two Income Trap book, and from reading it (and watching her talks via the internet), I believe she had the help of some researchers and fairly unfettered access to various government data. I'm not sure how much of it is available online, how much she had to request, etc.

If you have not read her book, you should though. She goes through exactly what you describe here, although at this point her numbers are now a few years out of date. Still an extremely worthwhile read.

good idea anonymous

you might consider creating an account too.

I don't have that book, although read a lot of the papers so maybe I can find references to the government databases, where exactly they are locating the raw data. I know it's out there, a matter of locating it.

Do try the book- she cited

Do try the book- she cited her sources as I recall. I wish I knew where my copy was, and I'd just look right now. I have far too many books!

Elizabeth Warren

My #1 choice for that vacant seat on he FED. It would be great to have someone inside who does not believe the crap the banksters keep feeding us (yield or die!!!)

Lady Liz could shock the Fed into plain dealing -- an end to the FED secrecy that is so outrageous!! Make the banks tell the truth.

Frank T.

Frank T.