The massive and unprecedented amount of debt being issued by the Treasury Department, and the relatively finite amount of savings in the world, has left the country vulnerable to a currency crisis. The place where evidence of this crisis might first turn up is in the treasury bond market.

That evidence might have happened in the last two weeks.

Just last week a treasury auction of 5-year bonds nearly failed.

but for the primary dealers the bid-to-cover was less than one, meaning that some of the issue would have been left on the table.That's a fail; but for the primary dealers the issue would not have subscribed.

Primary dealers are required to bid. That's the deal in exchange for their being named as "primary dealers."

It's very unusual for a treasury debt auction to receive so few bids, but doesn't necessarily mean anything in and of itself.

However, what happened during the following auction was enough to raise an eyebrow.

Just one week after the Treasury Department issued $28 Billion in 7-year bonds, $10 Billion being bought by Primary Dealers, the Federal Reserve turned around and bought up 47% of the primary allocated bonds in Open Market Purchases. This is backdoor monetization of debt.

They didn't even wait a full week! A more honest and open approach would have been for the Fed to simply buy them outright at the auction but this way, using "primary dealers" and "POMOs" and all these other extra steps the basic fact that the Fed is openly monetizing US government debt is effectively hidden from a not-too-terribly inquisitive US press and public.The speed of the shell game is accelerating.

This immediate repurchase of newly auction bonds by the Fed tells us that demand for these bonds is not nearly as high as advertised, and that things are not quite as strong as represented.

While certainly suspicious, this doesn't necessarily prove anything major. It could be just a temporary slack in demand...which just happens to accompany an enormous increase in supply.

Either that or it was a pre-arranged agreement, explicitly or not, that the Primary Dealers buy up the auction and the Fed would purchase half of them back the following week.

It doesn't take a konspiracy minded person to start drawing some conclusions. But a person might want some more evidence. Which brings me to this.

Foreign central bank liquidity swaps are again at the lowest level since the Lehman bankruptcy ($77 billion) - the level in 2008 pre-Lehman was $62 billion. The Fed is aggressively recalling any and all liquidity swaps.

So what exactly does that mean? I'll let someone more fluent in macroeconomics answer that question.

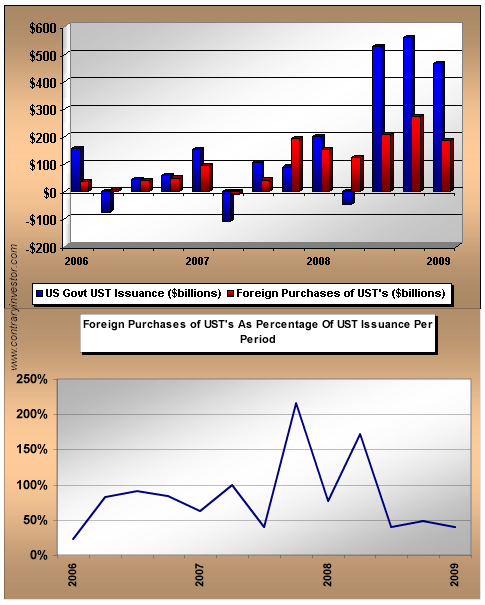

by means of USDollar Swap Facilities, the USDept Treasury is handing money to friendly foreign central banks in order to purchase USTreasurys in hidden or custodial accounts, all indirect bidders. Without them, the auctions would fail miserably.

Jim Willie goes on to point out that the "Toronto Dominion and Royal Bank (both of Canada) as well as Nomura (of Japan)" are all primary bond dealers now. Thus it appears that foreign demand for our debt appears larger than it really is.

What we are looking at is deceptive, nearly criminal attempts that propping up the American debt market, and on the backside the Fed is creating money out of thin air to buy back that debt.

All over the world, nations with a long history of defaults are borrowing money at lower rates than American municipalities. This has never happened before in modern history. Could the American debt markets have finally hit the wall?

Comments

Next week

with another %78 billion in auctions should be interesting. And yes, I too was mystified at how demand for the 7 was far greater than that of the 5 the day before. For the record, I am short treasuries.

Fed intervention

If this is really true, won't it become obvious on the Fed balance sheet when their holdings are posted? But will it be deemed newsworthy?