Well Fargo announced today $3 Billion in profits. It was fantastic news and it sent the stock market soaring.

However, one thing that didn't get talked about was why they made so much money.

Wells Fargo CFO Howard Atkins discusses the banks $3 billion reported first quarter 2009 earnings. Atkins hypes the impact of mortgages to the bottom line, due to low interest rates and foreclosure selling no doubt, but shockingly admits at the 7:45 mark that with the writedowns that would have been required by Mark to Market the bank actually lost money on the quarter.

To put it another way, Wells Fargo made money because the government allowed them to play "let's pretend your assets are worth something".

The reason why the government back-tracked on requiring banks to price their assets to market value was the premise that those assets are actually worth more than the market says they are. In other words, the banks are smarter than the investors.

That's a pretty shaky premise to believe. It requires us to accept the idea that those trillions of dollars worth of mortgage-backed securities are actually worth something close to face value. For this premise to be true you have to believe that the housing market is about to bounce back. It has to bounce back to historic highs in the midst of the deepest economic downturn since the Great Depression. Does anyone really think that is going to happen?

"I refer to the American housing market as “the big slum.” A slum is where the market value has fallen below the replacement value. It doesn’t make sense to fix anything. You don’t fix it, you just let it go to hell. There’s no way to get your money back."

- Eric Janszen

One person who has been consistently correct about the housing implosion, Mr. Mortgage, believes otherwise.

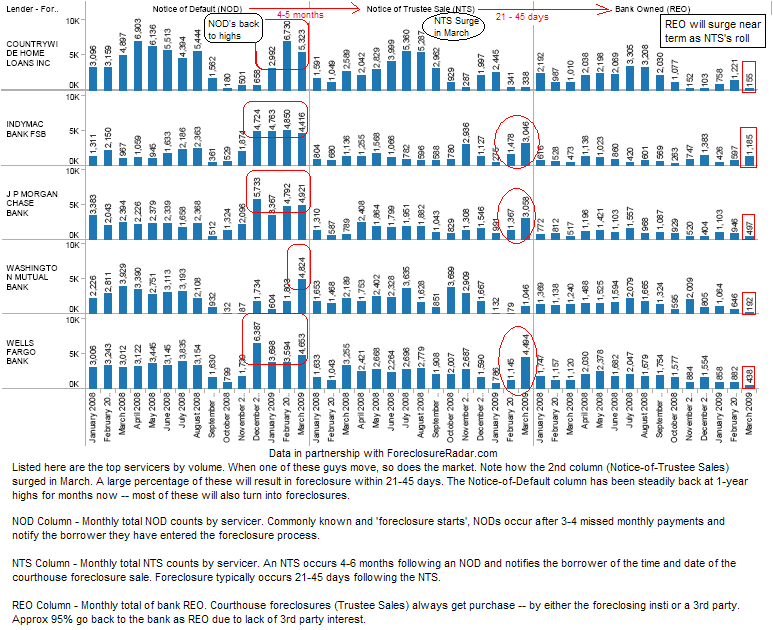

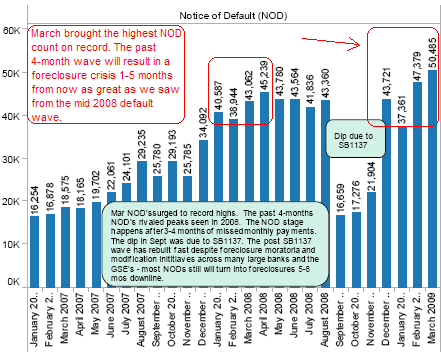

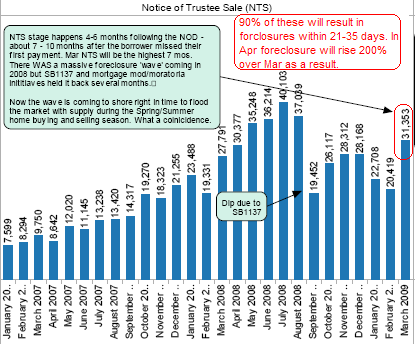

Are you ready to see the future? Ten’s of thousands of foreclosures are only 1-5 months away from hitting that will take total foreclosure counts back to all-time highs....

Foreclosure start (NOD) and Trustee Sale (NTS) notices are going out at levels not seen since mid 2008. Once an NTS goes out, the property is taken to the courthouse and auctioned within 21-45 days.

On September 2008, just as the subprime implosion was reaching its peak, the California legislature passed SB 1137. This law put a 90 day moratoria on many foreclosures in the state. That law has now expired. The law did nothing but buy time.

The numbers are hard to ignore. Credit Suisse says $1 Trillion in Alt-A and Option ARM mortgages will be resetting in the next 30 months. The subprime bust is mostly over, but the prime bust is only now starting.

If these resets and the resulting increased monthly payments send defaults soaring, and given other factors such as job losses and falling home prices there is every indication they will, the bank projects that foreclosures over the next four years could reach nine million or 18 percent of all mortgages.

An extremely large percentage of these Alt-A mortgages are commercial mortgages. Small businesses hold about 3.7 million of these mortgages and nearly 1.3 million of them are already delinquent.

Another factor weighing on the real estate market is the enormous "phantom supply" of bank owned homes.

Some of the top U.S. lenders own as many as 700,000 foreclosed homes they have yet to offer for sale, said Rick Sharga, executive vice president for marketing for RealtyTrac.The banks may be waiting to see how U.S. government plans develop before selling the properties, Sharga said.

These homes aren't even on the market and thus aren't counted against homes for sale numbers. The real reason why the banks haven't put these homes on the auction block is a debatable. But if I was to guess I would say that the reason is because once these homes are sold the mortgages behind them have to be marked-to-market.

If the banks were to do that to 700,000 mortgages you would suddenly see a bunch of banks become insolvent.

Thus you see a stand-off. The banks pretend that the real estate they own is worth something, and the government pretends that the banks are solvent. It's the same situation that played out in Japan back in the 1990's.

The Census released a report—migration in the US is off like 87 percent. It’s not like there’s some booming state someplace. Which is what’s unusual about this downturn compared to every other since World War II.Also, this is the only downturn where there are fewer cars on the road. There’s all sorts of other obvious indicators that this is not just a recession.

What’s not reported is every recession was induced on purpose by the Fed, in order to cool down the economy. This recession was not created by the Fed. The implications of that are lost of a lot of people: They are absolutely not in control.

- Eric Janszen

Comments

Did you notice?

NOD's & NTS's for Wells spike up since December.

This summer is going to bring housing right back to the headlines again. I feel sorry for all those people who are swallowing the MSM kool-aid.

It has always been about class warfare.

Nice job

This is the first good, timely article I've seen about the back side of the mortgage reset hurricane.

you proved my guess - great post

I suspected it was all about fictional assets by the modifications on mark-to-market.

18%, that's just incredible.

And we have not even delved into commercial real estate on EP. That is supposedly one of the next neutron bombs, along with unsecured debt.

More on the Wells Fargo numbers

I just spotted this article, which adds to the information.

1999 was my last year as a

1999 was my last year as a Series 7 person. If I had manipulated the facts, if I had misled the public like I see the banks doing today, the NASD would have fined me. There would have been possible criminal actions.

Instead the MSM prints this stuff, making it sound like it is some mystical stone that will turn lead into gold. Mr CPA what does two plus two equal. Answer....what do you want it to equal? This is a lot of accounting wizardry. But they rely on the fact that most people don't know the difference between debits and credits. Heck, maybe they are right because so far they it's worked for them.

God how long until people wake up or am I naive to believe people will wake up? Thirty years of wage stagnation but they still don't get it?

Help Mr. Wizard! Twizzle twazzle twizzle thwo...time for this one to come home. I'm not sure how much ore of this I can take without hitting the bottle.

The historical irony

That the big banks are essentially financial ghouls, while the smaller/community banks are doing well....well most of them are, there are some in trouble. Over the years the little guy banks were getting killed by the bigger ones, now it is the very advantage that the latter posed that now serves as their achillies heal.