Last week ago, Institutional Risk Analytics interviewed Josh Rosner of Graham Fisher & Co and David Kotok of Cumberland Advisors, and the discussion is one of the most direct and revealing of the true political nature of the financial collapse I have yet seen. As I have written before, using reports from the Fed, FDIC, and Comptroller of the Currency, the financial problems are very tightly concentrated in a handful of the largest banks, with over 8,000 plus smaller and regional banks having declined to participate in Wall Street’s derivatives madness.

But in this interview, the participants explain that there are only six large banks and financial firms that are the core of the problem – and the problem is not being addressed in the public’s best interest because of the huge political power these firms have. Citigroup, Bank of America, JPMorganChase, Wells Fargo, and to a lesser degree, Goldman Sachs, and Morgan Stanley are essentially dead. The enormity of their losses this year is going to force a break through the political obstacles these big banks have selfishly created to actually solving the financial and banking crises.

Since most of the toxicity in the banking system is concentrated among the larger banks, with perhaps US Bacorp (NYSE:USB) on down viable in the long run, perhaps we can rebuild the industry using the next round of TARP funds to bulk up these relatively smaller banks and thereby end up with 10-15 larger super regionals in the $300-$500 billion asset range.

Second, the Good Bank/Bad Bank debate is really a political battle between the large banks listed above plus Goldman Sachs (NYSE:GS) and Morgan Stanley (NYSE:MS) et al among the Sell Side survivors in NYC vs. the rest of the industry and the US economy. In preparing their plans for review by the White House, we hear that the Fed and OCC are supporting further bailouts for the larger banks, while the rest of the industry is being resolved and recapitalized a la Washington Mutual and Lehman Brothers.

Perhaps we ought to feed the "good bank" parts of the "too big to fail" crowd, a crowd prone to leverage and bad risk management, to the smaller and plain vanilla bankers that comprise the nominal majority of the industry. This would solve many things including reducing the lobbying power that Wall Street has in Washington. Come to think of it, President Obama should think about banning lobbying by any company participating in the TARP.

IRA also notes that Sheila Bair’s proposals have the same result: saving the big banks while sacrificing the rest of the banking system and the economy. It mentions that the rest of the banking industry about to burst into open revolt.

. . . you can understand why the smaller banks in the industry are SERIOUSLY PISSED OFF at the large banks and their minions in the Obama Administration like Tim Geithner and Robert Rubin. Oh, and don't forget Chairman Ben Bernanke and the entire Fed board of governors. These leading officials are increasingly taking the side of the large banks in the battle over limited financial resources, a fact that is causing the community bankers to rise in anger. Stay tuned.

Rosner flat out states, “I am hearing very clearly from within the regulatory community that it is their primary concern that whatever they are planning is predicated on the notion that we must keep the large banks alive.” Kotok confirms, and notes

The motivation of keeping big banks alive is driven by a desire to avoid another Lehman on the Obama watch. I hear people saying that we cannot have another Lehman, therefore we cannot permit a failure…

Kotok notes that Paul Volcker is pushing this “no more Lehmans” line. He also notes that of the 16 primary dealers of U.S. debt that remain, nine of them are foreign owned. This creates a big problem for the Fed, because it gives a foreign government final say in any decision about the failure of a primary dealer. This is essentially what happened in the case of Lehman Bros. British regulators and the Bank of England placed such requirements on the Barclays purchase of Lehman, that the Fed backed away. Importantly, Kotok nails Bernanke and Geithner for lying about this in testimony before Congress and Geithner’s conformation hearings.

IRA: Nobody in the Congress or the White House wants to acknowledge that the policy prescriptions coming from the Fed and Treasury are badly flawed when it comes to bank solvency. The market liquidity measures have had success, but the "save the big banks" approach by the Fed is just more of the same nonsense that cause the problem in the first place.

Rosner: Exactly. In operational terms, there are no longer institutions that are too big to be resolved. As we discussed with the tree analogy, that is different from 'failing'. Any risk of a run on C[itigroup] or the other banks is now ameliorated. The recently enacted changes to guarantees on deposits, non-interest bearing transactions accounts, etc, addressed that issue. The other systemic issue was counterparty risk, but with the qualified financial contract rule just put in place by the FDIC that risk is also largely gone and you can resolve a bank's counterparty exposures into a good bank/bad bank configuration with little problem and without creating larger systemic risk. If the a counterparty's financial contracts are adequately collateralized, then they can go with the good bank, but the FDIC must retain unilateral power as receiver to reject or accept contracts. The notion that we can't allow C[itigroup] to be wound down and broken up is a spurious argument. I think this argument has less to with Lehman and more to do with the fact that the Fed of New York and the Board have always benefited from the failure of small institutions and the absorption of those assets by the big banks. There is no way that they can stomach seeing their regulatory power dissipated by those institutions now being broken up and sold. Perhaps we have to go back to the question of whether it makes sense for the Fed to be a regulator as well as a central bank.

Rosner: If the FDIC determined C[itigroup] is sick enough, were it not politically blocked by the Fed and OCC, then the FDIC has the authority to resolve C[itigroup] tomorrow.

The IRA: We are reminded of one of the drafts of the TARP legislation where somebody inserted language that would have allowed the FDIC unilateral authority to declare an institution insolvent without first getting a declaration of same from the primary regulator. Needless to say, the provision was not included in the final bill, but this illustrates the civil war that rages between the Fed and OCC, on the one hand, and the FDIC and the state regulators on the other. This issue of resolving the larger banks has been a political issue going back to Paul Volcker's day.

They foretell the appointment of Bill Dudley to replace Geithner as President of the New York Fed, and discuss who is really running policy in Washington. Geithner is too wounded to actually lead, but the Republicans in Congress are afraid to oppose him because they “fear a socialist in the wings.” (I wrote about some of the problems with Geithner back in November.)

Kotok says this leaves Volcker and Summers running the show, but IRA argues that an internal battle between Volcker on one hand and Summers and Rubin on the other has yet to be decided.

. . . Paul Volcker and Robert Rubin, and Larry Summers, represent very different and ultimately incompatible world views. Volcker is all about public service, transparency and fairness. Rubin and also Summers represent political duplicity and malfeasance on a grand scale, especially when you look at their role in blocking regulation of OTC derivatives and structured finance.

I will conclude with a statement by Rosner:

Summers is just as capable of being misdirected by the same Wall Street inputs as caused this mess. We need to somehow communicate to Summers et al, though the media if necessary, that the managed breakup of the big New York banks does not necessarily mean a systemic failure and another crisis.

The Big Banks vs. America: A Roundtable with David Kotok and Josh Rosner

Can we verify this?

If this is true, that most banks are/were perfectly fine and it was just the large bad apples....then even more nationalization of those bad apples sounds like it is in order.

Any sites/watchdogs having a percentage list of who really are the bad banks and how many are not?

Multiple reports of the bad banks lobbying to get TARP money and now Geithner is supposedly going to limit that but the details are not clear.

From my DailyKos diary I wrote last year after Bare Sterns

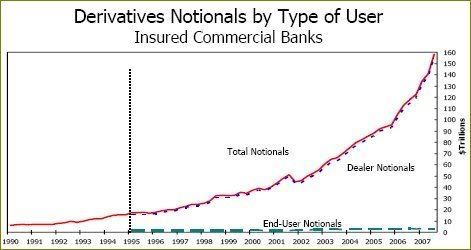

Take a look at this graph from the Third Quarter 2007 Report on Bank Derivatives Activities by the Office of the Comptroller of the Currency

Look at that bottom line that stays flat no matter how much derivatives increases. That’s the amount held by end-users. End-users ?! So it’s the banks that are holding most of the derivatives. Now, this is just commercial banks, and does not include derivatives activities of investment banks.

According to the Federal Reserve Board’s Report on the Condition of the U.S. Banking Industry: Second Quarter, 2006

derivatives holdings of the 50 largest bank holding companies as of the second quarter of 2006 totaled $ 117,631 billion, or $117.6 trillion.

Derivatives holdings of all other reporting bank holding companies in the United States was $88 billion.

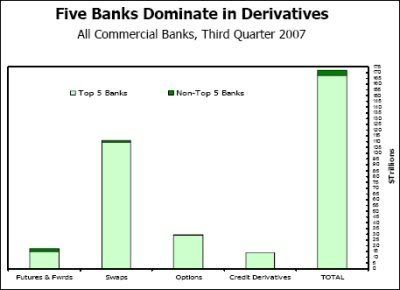

In fact, only five commercial mega-banks - J.P. Morgan Chase, HSBC, Citibank, Bank of America, and Wachovia – account for well over 90 percent of derivatives activities by commercial banks. Here’s a graph from the OCC report:

updated blog post?

If you use the search, there are some really good posts on EP on derivatives but it looks like none of them include the raw data you are displaying.

Perhaps you want to do a "hard core" data/stats/graph update on derivatives blog piece?

This is damn good juju.

I'll try and get to it this weekend

if I don't post it, holler me a reminder. Unless I can just post the April 2008 original. Euthanize Wall Street to save the economy

we recycle on EP!

I'd suggest simply update it to now be current and then take what is relevant in the original and repost.

Many of the writings from the people on here are not that "time dependent" which ya know blogs really are.

So, I personally think it's fine to update older writings and just bring them up to current, revised and repost them.

Matter of fact I have a few that I should consider doing that.

It's kind of a bummer when people write timeless detailed posts with all sorts of references, analysis and it's shelf life is 24 hours (on EP the shelf life of post I have purposely make longer, because of this and still looking to improve that)