The Conflicts Brewing In America's Ten Classes

Authored by Charles Hugh Smith via OfTwoMinds blog,

What we do know is that things have internal structures with dynamics that operate whether we "like" them or not.

Correspondent Manoj S. recommended an essay from the always-insightful John Michael Greer on the dissolution of unproductive classes behind the smokescreen of AI: A Game of Musical Chairs

"You can sell Americans on anything, no matter how wretchedly unsatisfactory it is, by labeling it as progress. That's what's being done now, with AI being used as a justification for firing useless workers, deleting unnecessary departments, cutting office staff down to scales that actually make sense, and shutting down the classroom-to-cubicle pipeline that once poured new graduates into salary class jobs. We can expect that process to accelerate dramatically in the years ahead."

Greer begins by laying out a compelling taxonomy of class in America, four self-explanatory classes defined by this question: how do different groups in today's America get their income?

1. investment class: income from investments (i.e. capital)

2. salary class: income from a monthly salary with benefits

3. wage class: income from an hourly wage with no benefits

4. welfare class: income from welfare programs

Greer argues that the salary class is now the gravitational center of power in the U.S., absorbing much of the national income in unproductive faux-problem-solving for fabricated problems explicitly devised to justify generous salaries and benefits.

The nation can no longer afford this staggeringly costly unproductive work force and so "replacing cognitive work with AI" is the cover story for the mass evisceration of this class, in a parallel to the previous gutting of the factory work force by automation and offshoring.

I've been addressing the class taxonomy of the US since 2012, and I'd like to add some commentary on the dynamics Greer so succinctly describes. In America's Metastasizing Class Wars (August 27, 2020), I laid out ten classes, based not just on sources of income but on several additional criteria:

Systemic Power: political control of the state's monopoly of force / coercion; financial control of the system's taxation, incentives and optimizations; corporate control of essential technologies - platforms; corporate-state "soft power" control of cultural, social and intellectual belief structures and sources of influence: media, social media, think-tanks, foundations, the Higher Education Clerisy, etc.

The power to protect bureaucratic-institutional fortresses from budget cuts, transparency and accountability.

Agency: the power to leave employment or a locale and change one's life; freedom from debt-servitude / employment bondage.

My ten classes: yes, this is more complicated that Greer's four classes but since power has sources other than income, accuracy demands an accounting not just of income but of power and agency, which is an individual form of power with systemic consequences such as social mobility.

1. The Deep State. Unelected, unaccountable, they wield state power. Call them if you're about to be renditioned. But you need either power or relationships to have their number. Relationships are a form of power.

2. The Oligarchs. Top bidders in the auction for political and financial influence. The top .001%. Able to rig the structures of power to serve their private interests.

3. New Nobility. The super-wealthy class just below the Oligarchs. The top .01%. They have the means to serve their private interests via lobbyists and campaign contributions. $10 million in campaign contributions nets $100 million in tax breaks / subsidies.

4. Upper Caste. The technocrat/professional class that manages the Status Quo for the upper classes. This includes wealthy entrepreneurs and owners of enterprises: rich but not rich enough to rig the structures of power to serve their private interests.

5. State Nomenklatura. Well-paid government administrators with ironclad job security and power.

Together, the Upper Caste and the Nomenklatura comprise the upper-middle class. Owners of enough capital (real estate and stocks) to cheer serial credit-asset bubbles. Since I'm doing well, the system is working great.

6. The Middle Class. Wage-earners and salaried employees, owners of traditional sources of financial security: family home, 401K retirement funds, etc. Due to high debt, many qualify as debt-serfs / wage-slaves with minimal agency despite their ownership of middle-class status signifiers.

7. The Working Poor. Households with earned income but it is not sufficient to secure the basics of middle class life. Many qualify for social welfare programs such as food stamps and Medicaid. Due to high debt, many qualify as debt-serfs / wage-slaves with minimal agency.

8. State Dependents. Though often labeled "poor," those with cash / black-market income often live better than the working poor, due to generous social welfare benefits.

9. Mobile Creatives. Self-employed independents, entrepreneurial sole proprietors with adaptive skills. They may collaborate with other Creatives rather than have employees, and may have part-time conventional jobs. They have mobility between sectors and ways of earning income sufficient to acquire capital / assets. They "own their livelihoods." Their credo is trust my network, not the corporation or the state.

10. Gig economy precariat. May supplement insecure employment (limited hours, no benefits, etc.) with gig work, may combine cash work with rideshare gigs, may juggle several delivery / eBay sales / rideshare gigs. The difference between precariats and Mobile Creatives is precariats are generally in survival mode (high debt, unreliable income, etc.) and are unable to acquire capital / assets. They "rent" their livelihoods rather than "own" them.

Here is a curated list of my essays on the taxonomy of class in the US:

The Three-and-a-Half Class Society (October 22, 2012)

America's Nine Classes: The New Class Hierarchy (April 29, 2014)

What the Global Status Quo Optimizes: Protecting Elites and the Clerisy Class That Serves Them (September 26, 2014)

Explicitly describing what the system optimizes would trigger social instability.

The New Class: Mobile Creatives (May 1, 2014)

The key characteristic of the Mobile Creative class is that they live by this credo: trust your network, not the corporation or the state.

When Belief in the System Fades (March 12, 2008)

Let's distill the key dynamics this structure reveals.

1. This is a neofeudal society passing itself off as a free-market democracy. Power is concentrated in the top state-private sector classes. No one below has any real power. Electing another leader or party changes nothing: life gets more difficult, insecure and expensive for commoners regardless of who's in office. The Imperial project grinds on, regardless of the delusional hope that electing someone else will change anything. Everything else is an illusion of power, not real power.

Try switching the 37% tax rate on labor to capital gains and all income from capital, and see how far you get.

2. Debt and social engineering are the foundations of America's neofeudalism. The essence of neofeudalism is debt penury and wage-slave bondage to the owners of the debt, which is capital that generates income. Commoners have no agency because they have to work for corporations or the state to service their debt. They can't change jobs because they'll lose healthcare insurance, and so on.

Social engineering: as Greer highlighted, Americans can be sold anything, no matter how destructive, unhealthy and exploitive, as long as it's packaged as Progress, especially technological Progress and novelty-as-progress. This is the power of The Mythology of Progress.

3. Beneath the endless marketing of "free market capitalism," few have any real agency. Stripped of PR gloss, the majority of workers have a false choice of servitude: they can serve their current oligarch / state agency / corporation, or they can toil in another noble's domain. Six one way, half-dozen the other.

4. America's neofeudalism now depends on inflating an endless series of credit-asset bubbles that generate phantom wealth, financial claims that are easily inflated without actually creating any real value via increasing income streams by means other than inflation and monopoly extortion.

This has worked so well for so long that recency bias has kicked in and we now believe this is a well-oiled permanent mechanism we can rely on. Alas, credit-asset bubbles are inherently unstable and the current system-wide bet on AI being something that will actually generate value / massive new income streams is an all-in last-ditch bet. When this bubble pops, the conditions enabling a future bubble will no longer exist.

But nobody says that, do they?

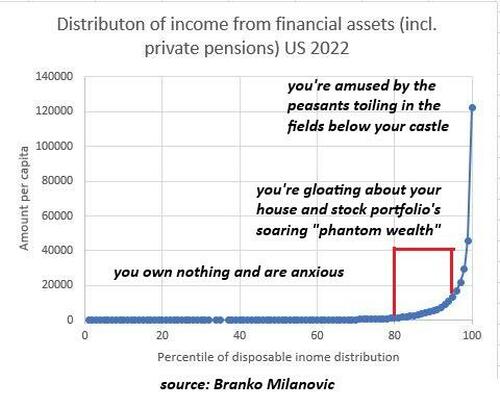

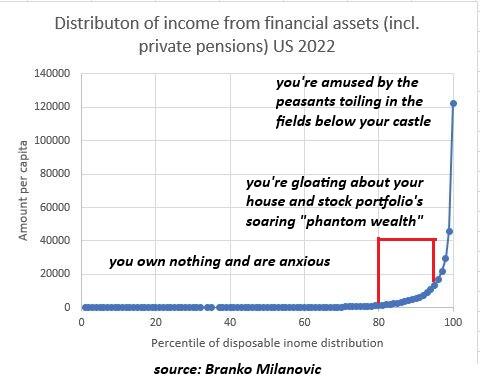

5. Here is a chart of the income distribution from owning capital. Note that it follows a power-law distribution: the few collect the lion's share of the income generated by capital. The vast majority don't own any income-generating capital, and the top 20% are delighted by the steady rise in their phantom wealth as the bubble-du-jour inflates the nominal price of the assets they own, setting up the inevitable crash when tulip bulbs revert from "investments" to flowers.

Meanwhile, those collecting 95% of the income from capital look down on the toiling peasantry from their Kafkaesque castles with amusement. Student loans, mortgages, 27.99% interest rate credit cards--it's really quite marvelous, isn't it?

6. Symbolic work versus productive work. Much of the work Greer describes as unproductive is considered highly productive because our exploitation of hydrocarbons and technology has generated such a vast surplus that we could spend it on symbolic work--meetings about meetings, compliance reports, marketing plans, projections, consulting, and so on, work that despite claims to the contrary has little to do with harvesting grain, connecting pipelines, replacing transformers, making beds, performing surgery or any other real-world work.

What If the Work We're Busy Automating Is Needless? (June 19, 2026)

Try telling the priesthood of the temple gods that their work is symbolic. Ours is the most valuable labor, as we're the ones keeping the whole thing glued together. If we stop, the gods will be angered and all will fail. Indeed.

As a result, we have no experience of a way of life stripped of symbolic work based on seeking positions of status, accumulating credentials, and so on.

7. The number of Mobile Creatives is modest. Some years ago I dug into IRS data on types of income and found that only a tiny sliver of the workforce is truly independent / self-employed, i.e. they earn a middle-class income from royalties, ownership of enterprises or professional services. Out of roughly 160 million employed people, around 16 million are self-employed, but only 6.9 million are professional-class with some form of incorporation, and around 3 million others make enough income to live well. So around 6% of the work force is truly independent.

We're inundated with glowing accounts of individuals earning big bucks on "passive income" schemes, just as there are endless posts about how to make six figures using "can't lose" techniques that just so happen to cost $200.

The reality is it's extremely challenging to live outside the peasantry-Nobility arrangement. In my experience, it takes a willingness to constantly absorb risk and failure, and wear an absurd number of hats: accountant, manager, programmer, laborer, creative wizard, psychologist, consultant, student--and even after all that, success is not guaranteed. The difference between living in a shack and "success" is often some form of luck.

8. Something's gotta give. Soaring debt, public and private, rampant corruption, extortion, exploitation, dynamic pricing, unaffordable shelter, utilities and food, tulip-bubble scale euphoria, moated bureaucracies, complexity thickets that stifle competition, neofeudal lords digging bunkers and hiring private armies as they sense the peasantry's distemper--something's gotta give, we just don't know what will break first.

The usual explanations no longer explain anything. Their incoherence is obvious but lacking anything more coherent, we go back to insisting that all will be well if only everyone would wear their Silly Hats. What Once Explained Everything Now Explains Nothing.

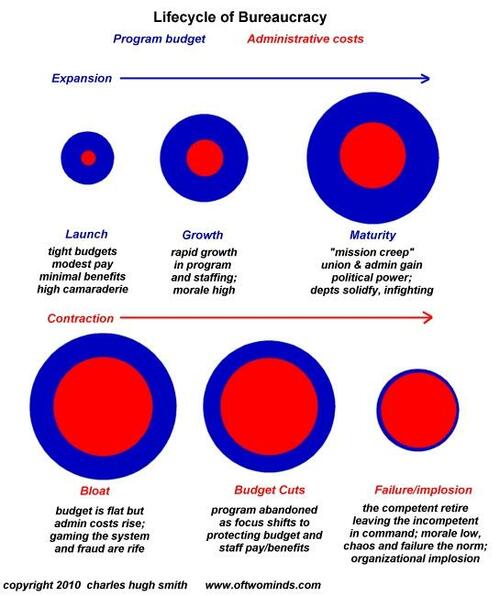

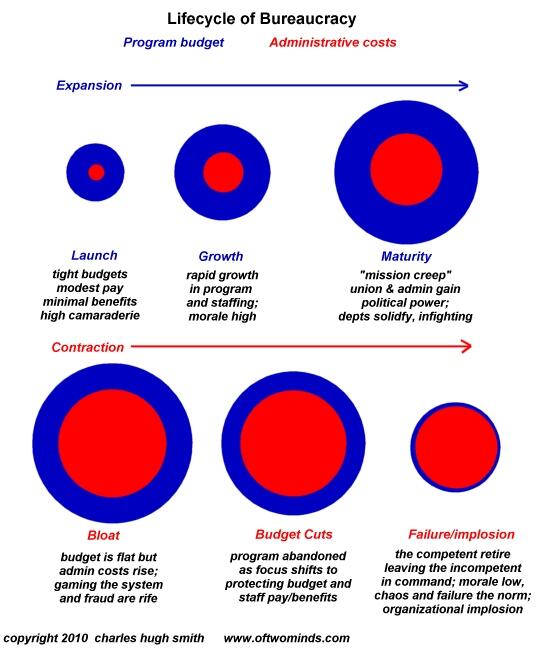

What we do know is that things have internal structures with dynamics that operate whether we "like" them or not. I put together this chart of the Lifecycle of Bureaucracies some years ago to illustrate how institutions decay as self-interest replaces the original purpose of the organization. This leads to implosion - collapse. Again, whether we "like" it or not.

Greer's forecast of the end of white-collar symbolic work may well be prescient. Costs are funny things. We can play games with "money" and think we've solved the problem of costs, but costs are weirdly embedded in the real world, and so thinking that we can overcome all those costs by requiring everyone to wear Silly Hats doesn't actually work.

As Peter Drucker observed, enterprises don't have profits, they only have costs. This is also true of governments, households, institutions and, well, everything else. Calling tulip bulbs "wealth" works like magic for a time, and then reality intrudes.

* * *

My book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition). Introduction (free). Become a $3/month patron of my work via patreon.com. Subscribe to my Substack for free

Tyler Durden

Tue, 07/21/2026 - 16:20

American whiskey is seen on the shelves of a SAQ liquor store in Montreal on March 4, 2025. The Canadian Press/Christinne Muschi

American whiskey is seen on the shelves of a SAQ liquor store in Montreal on March 4, 2025. The Canadian Press/Christinne Muschi

Michigan Gov. Gretchen Whitmer speaks at an event in National Harbor, Md., on May 4, 2023. Kevin Dietsch/Getty Images

Michigan Gov. Gretchen Whitmer speaks at an event in National Harbor, Md., on May 4, 2023. Kevin Dietsch/Getty Images A cup of coffee in Culver City, Calif., in a file photograph. Kevork Djansezian/Getty Images

A cup of coffee in Culver City, Calif., in a file photograph. Kevork Djansezian/Getty Images

Recent comments