Western Nuclear Industry Bounces Back With Progress Across Small And Large Designs

After last month's report from Goldman Sachs on the ongoing global nuclear renaissance listed only a couple headlines for the western nuclear industry, June saw a significant bounce back as the industry saw progress across the microreactor landscape and the larger SMR and national grid-scale designs.

The Micro Reactor Industry saw a huge achievement with the exceeding of the goals set by President Trump in the 2025 Executive Orders, with four microreactor designs obtaining criticality by July 4th.

The AP1000 reactor, which is emerging as America's flagship grid-scale design, also saw significant multi-billion-dollar support from the Department of Energy when the Office of Energy Dominance Financing put up a potential $17.5 billion in funding for long-lead components and other pieces/parts of the reactor supply chain.

Goldman Sachs analyst Brian Lee reviews headlines across the nuclear industry for June.

New reactor progress and announcements

North America

6/2/26 - United States - The New York Power Authority has launched a solicitation to develop at least 1 GW of advanced nuclear capacity in Upstate New York, seeking proposals for both large reactors and SMRs, while also committing $40 million to nuclear workforce development.

6/8/2026 - United States - FERC approved Constellation’s request to transfer 760 MW of interconnection rights to the Crane Clean Energy Center, helping support the planned restart of the former Three Mile Island Unit 1 and improving its ability to deliver power to the grid ahead of major transmission upgrades.

6/9/2026 - Canada - Bruce Power’s refurbished Bruce 3 reactor has returned to service in Canada, more than seven months ahead of schedule, following a major component replacement project that extends the unit’s operating life by over 30 years.

6/16/2026 - United States - The US NRC has approved an 80‑year operating life for the two reactors at Georgia Power’s Edwin I. Hatch nuclear plant, extending operations into the mid‑2050s. The licence renewal follows a review completed in under 12 months and supports the continued operation of one of Georgia’s key nuclear generating assets.

6/23/2026 - Canada - Canada has unveiled a national strategy that positions nuclear energy as a key part of its future energy mix, supporting the deployment of new large-scale reactors, SMRs, and an expanded domestic nuclear supply chain.

6/24/2026 - Canada - AtkinsRéalis has formally begun the US licensing process for its CANDU reactor technology, submitting a Notice of Intent to the NRC and marking the start of pre‑application engagement. The move supports potential deployment of the 700+ MW Enhanced CANDU 6 reactor in the US.

6/24/2026 - United States - The US DOE has conditionally committed up to $17.5bn in loans to support procurement of long‑lead components for up to 10 Westinghouse AP1000 reactors, aiming to accelerate reactor deployment and strengthen the domestic nuclear supply chain.

Europe

6/16/2026 - Sweden - Nordic Baseload Power has applied for Swedish state support to build two large-scale reactors (~2.5 GW) at the former Barsebäck nuclear site, marking the fourth application under Sweden’s new nuclear support programme.

6/29/2026 - Germany - A group of former German nuclear plant managers and experts has urged the government to restart Germany’s nuclear power plants, arguing that reactivation is technically feasible and could improve energy security and electricity affordability.

6/30/2026 - Slovakia - Fuel loading has begun at Slovakia’s Mochovce 4 reactor, marking the start of active commissioning for the country’s fourth nuclear unit. The unit has now entered the testing and startup phase ahead of commercial operation.

7/8/2026 - Czech - The Czech Ministry of Industry and Trade said the Dukovany new‑build project remains on schedule one year after contracts were signed with KHNP, with geotechnical surveys completed, the first conceptual design submitted, and key Czech suppliers selected. The project is currently focused on licensing, permitting, and infrastructure work ahead of a targeted 2029 construction start.

7/9/2026 - UK - The UK government and EDF have agreed terms to extend the operating life of the Sizewell B nuclear plant by 20 years to 2055, with EDF committing £800 million of refurbishment investments to support long‑term operation.

Asia and other

6/5/2026 - Japan - Japan has proposed replacing aging nuclear reactors to maintain its nuclear generation capacity, with the government targeting the replacement of up to 14 reactors by the 2050s as older units retire.

6/10/2026 - Russia - Russia is targeting a 2027 construction start for the BN‑1200 fast reactor at Beloyarsk, with site preparation under way and licensing expected in 2027. The project is currently targeted for completion in 2034.

6/19/2026 - India - India’s Tarapur Units 1 and 2, the world’s oldest operating nuclear reactors, have returned to the grid following extensive modernization and refurbishment. The two units, which had been offline since 2020, received major safety upgrades and regulatory approval to resume operation.

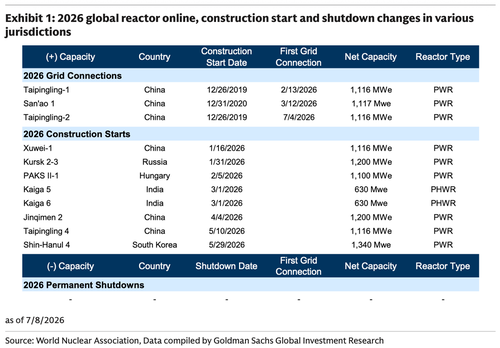

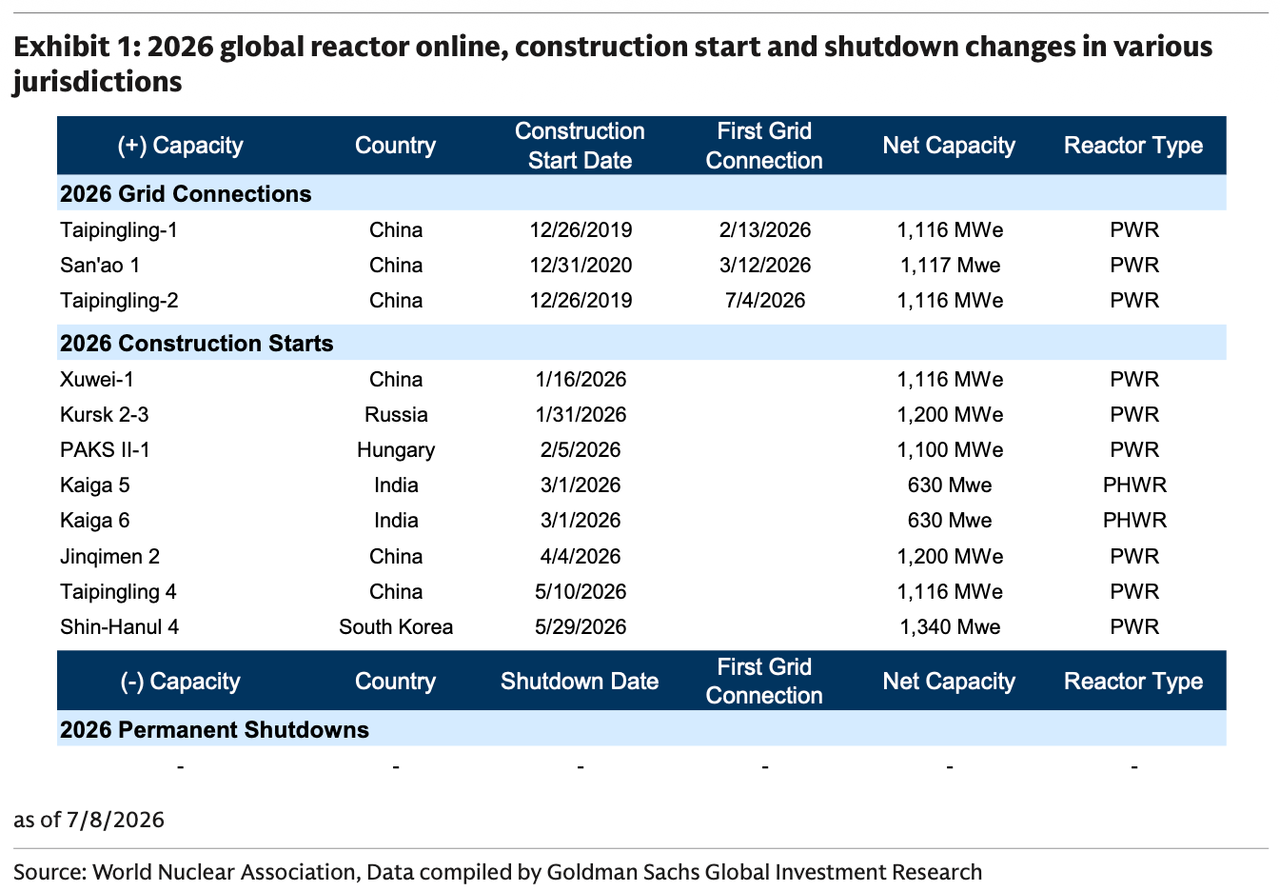

7/6/2026 - China - Taipingling Unit 2 has been connected to China’s grid for the first time, marking a key commissioning milestone for the 1,116 MWe Hualong One reactor. The unit is the second of six planned reactors at the Guangdong site and is expected to enter commercial operation in 2H26.

7/13/2026 - China - Changjiang Unit 3 has achieved first criticality, marking the startup of the 1,100 MWe Hualong One reactor at the Changjiang nuclear plant in China’s Hainan province. The unit has now entered the commissioning phase ahead of grid connection and commercial operation.

SMR announcement tracker

6/3/2026 - UK - X‑energy has submitted its Xe‑100 high‑temperature gas‑cooled reactor for the UK’s GDA process, marking the start of formal regulatory review. The submission supports X‑energy and Centrica’s plans to develop up to 6 GW of new nuclear capacity in the country.

6/4/2026 - United States - US SMR developers announced a series of partnerships to advance reactor deployment, including Day & Zimmermann supporting pre‑construction and above‑ground construction for Deep Fission’s Gravity reactor, while Sciaky will manufacture components for NX Atomics’ SMR platform using additive manufacturing technology.

6/5/2026 - Sweden - Blykalla has applied for Swedish government financing for its planned six‑reactor SEALER SMR plant in Norrsundet, the first advanced nuclear project submitted under Sweden’s new nuclear support framework. The proposed plant would have up to 330 MWe of capacity and could enter operation in the early 2030s, subject to approvals and investment decisions.

6/5/2026 - Uzbekistan - Uzbekistan has marked the start of construction of its first SMR, with a ceremony for first concrete at the Jizzakh nuclear project. The project features Russia’s RITM‑200N reactor technology and represents a key milestone in Uzbekistan’s nuclear power programme.

6/5/2026 - United States - Antares Nuclear’s Mark‑0 microreactor has achieved first criticality at Idaho National Laboratory, becoming the first reactor to reach this milestone under the US DOE’s Reactor Pilot Program. The demonstration validates the company’s microreactor technology and marks an important step toward future advanced reactor deployment.

6/9/2026 - Romania - DP World has launched a feasibility study into deploying SMRs at Romania’s Port of Constanța, evaluating whether nuclear power could support the port’s long‑term energy needs, growth, and decarbonisation goals.

6/11/2026 - United States - DOE has approved the PDSA for Oklo’s Aurora reactor at Idaho National Laboratory, a key regulatory milestone under the DOE’s Reactor Pilot Program. The approval advances the project toward deployment by validating the reactor’s preliminary safety basis.

6/12/2026 - Sweden - Studsvik has applied for Swedish state support to develop up to 1.4 GW of SMR capacity in southern Sweden, with potential projects at Nyköping and Valdemarsvik based on light‑water reactor technology. The company is targeting first operation in the second half of the 2030s.

6/15/2026 - Sweden - Videberg Kraft has selected Rolls‑Royce SMR technology for its planned nuclear project on Sweden’s Värö Peninsula, with plans to deploy three SMRs. The project would be Sweden’s first new nuclear power plant in more than 40 years, with the first unit targeted for the mid‑2030s.

6/17/2026 - UK - Core Power has launched a feasibility study to assess BWXT’s mPower SMR for use in floating nuclear power plants, evaluating the technical, regulatory, and commercial viability of deploying the 195 MWe reactor in shipyard-built floating power platforms.

6/17/2026 - UK - TerraPower’s Natrium reactor has entered the UK’s GDA process, marking the start of formal regulatory review for the 345 MWe sodium‑cooled fast reactor. The move advances TerraPower’s plans for potential deployment in the UK and follows the company’s submission to the UK regulators earlier this year.

6/19/2026 - United States - Elementl Power has selected GE Vernova Hitachi’s BWRX‑300 SMR technology for a proposed 1.5GW nuclear project in Ohio, with plans for up to five reactors at a site. The company has already filed for grid interconnection and is targeting construction in 2030 and completion of the first unit in 2034.

6/22/2026 - United States - Valar Atomics’ Ward 250 microreactor has achieved criticality under the US DOE’s Reactor Pilot Program, becoming the second reactor to meet the programme’s July 2026 target. The 5 MW TRISO‑fuelled, helium‑cooled reactor completed a zero‑power criticality demonstration at the Utah San Rafael Energy Lab.

6/24/2026 - UK - Holtec and EDF have submitted a proposal to deploy up to four SMR‑300 reactors at the former Cottam power station site in the UK. The companies have also agreed to form a joint venture to advance the project, which would repurpose the former coal plant site for new nuclear generation.

6/29/2026 - Sweden - Blykalla and Hitachi Energy have signed an MoU to support deployment of Blykalla’s lead‑cooled SEALER SMRs, combining reactor technology with Hitachi’s expertise in electrification, grid integration, and digital energy systems.

6/30/2026 - Poland - Orlen Synthos Green Energy has applied for a Contract for Difference to support the construction of 14 BWRX‑300 SMRs across three sites in Poland, marking a key financing milestone for its SMR programme.

7/2/2026 - UK - SGE and a consortium including Samsung C&T, Laing O’Rourke, Aecon and Google Cloud have proposed deploying 14 GE Hitachi BWRX‑300 SMRs across three UK sites, representing 4.2 GW of capacity. The privately financed project targets first commercial operation in 2034, with the initial site planned to host six reactors and two additional sites hosting four reactors each.

7/2/2026 - United States - Deployable Energy’s Unity demonstration reactor has achieved initial criticality at Idaho National Laboratory, becoming the third US microreactor to reach the milestone ahead of the DOE’s 4 July target.

7/3/2026 - Finland - Finland’s nuclear regulator has completed an international safety review of Steady Energy’s LDR‑50 SMR design, with regulators from the Czech Republic, Poland, Sweden, and Ukraine participating in the assessment. The review found no fundamental obstacles to further development of the reactor concept, while providing feedback to support future licensing work.

7/7/2026 - UK - Chiltern Vital Group and Cambridge Atomworks have signed a LoI to explore building the prototype Odin microreactor at the Berkeley Green Science and Technology Park in England. The project would support testing and regulatory development of the molten‑salt‑cooled microreactor, with Cambridge Atomworks targeting an operational prototype by 2030.

7/7/2026 - United States - Aalo Atomics’ Critical Test Reactor achieved initial criticality at Idaho National Laboratory, becoming the fourth US microreactor to reach the milestone by the DOE’s 4 July 2026 target.

7/8/2026 - United States - Deep Fission has received its prototype reactor canister at its Kansas pilot site, marking a key milestone for development of its Gravity reactor, which is designed to place a nuclear reactor in a borehole about a mile underground. The canister will be used in the company’s proof‑of‑concept program to validate installation, infrastructure, and deployment processes ahead of a future commercial demonstration.

7/8/2026 - USA, Japan & South Korea - The US, Japan, and South Korea have signed a trilateral agreement to accelerate SMR deployment in third countries, initially focusing on the Indo‑Pacific region. The framework aims to coordinate financing, supply chains, licensing, and industry partnerships to support fleet‑scale SMR deployment and expand access to nuclear energy.

7/10/2026 - United States - Argentina has announced plans for a privately financed 300 MWe ACR‑300 SMR at the Atucha site, with US‑based Meitner Energy planning to invest $1.2bn in the project. The reactor would be the first commercial ACR‑300 and the first nuclear reactor in Argentina financed entirely with private capital, marking a major investment in the country’s nuclear sector.

Global reactor critical updates

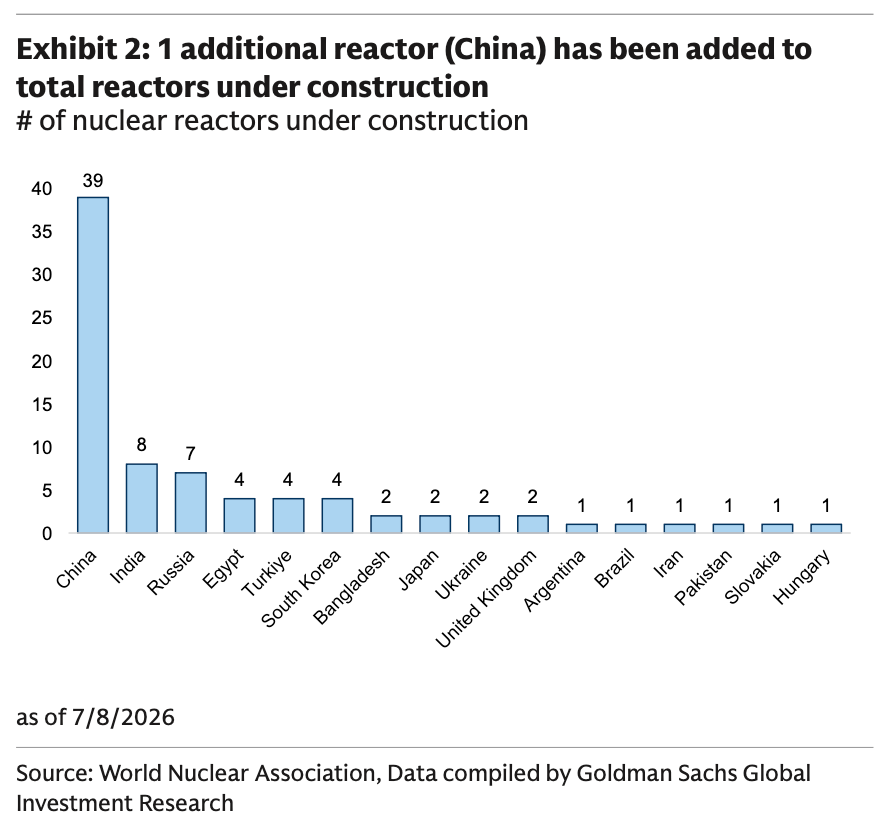

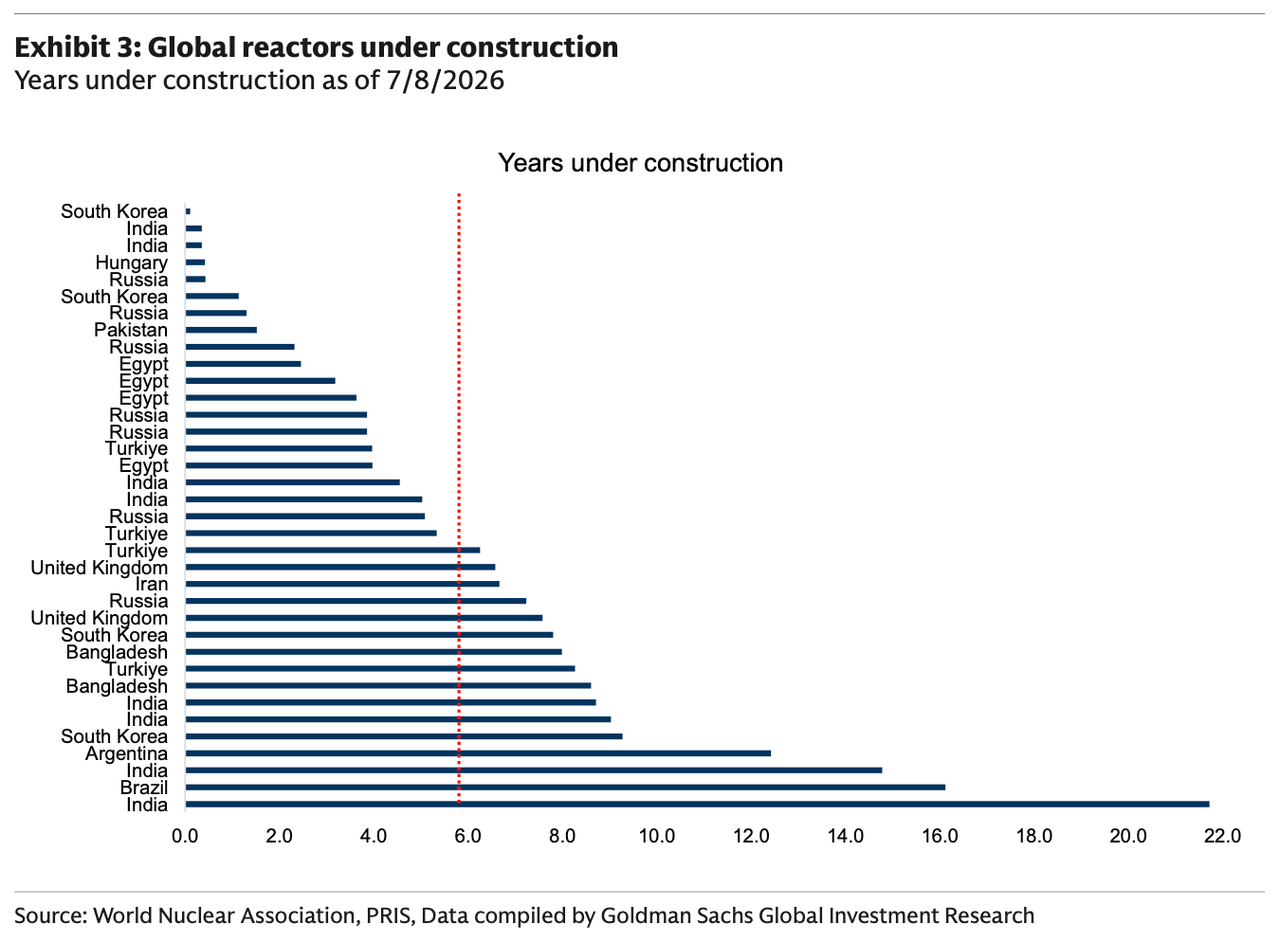

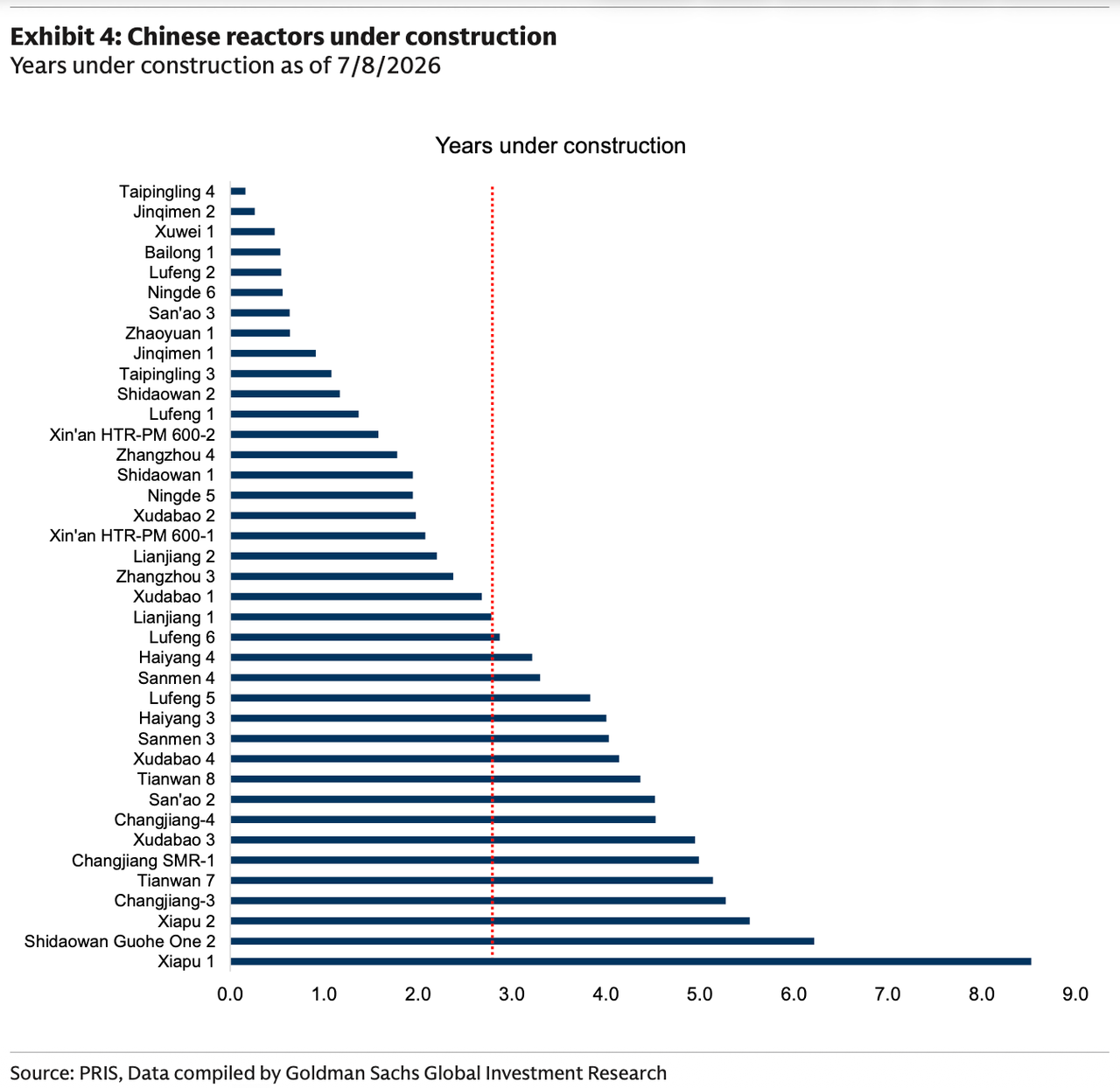

In the month of June, there have been few changes to new reactor construction starts, grid connections, shutdowns, or restarts.

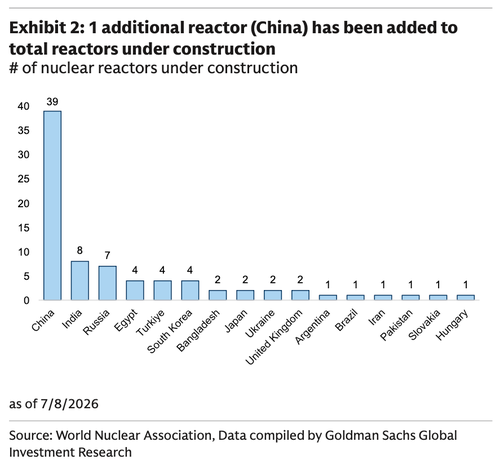

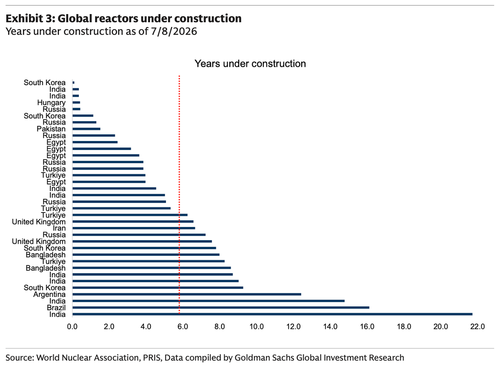

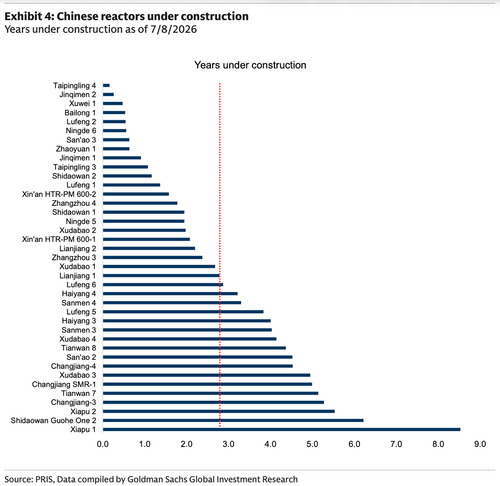

Global reactor construction tracker

Fuel announcements

6/1/2026 - United States - Cameco and Orano have agreed to acquire TEPCO’s remaining 5% stake in the Cigar Lake uranium mine, giving the two companies full ownership of the project. Following the transaction, Cameco’s stake will increase to 57.4% and Orano’s to 42.6%, further consolidating ownership of one of the world’s highest‑grade uranium mines.

6/2/2026 - United States - Urenco has announced a multi‑billion‑dollar investment to build a new uranium enrichment plant at its New Mexico site, adding 2.1 million SWU of capacity and increasing output by nearly 50%. Construction is planned to begin in 2029, with first production targeted for 2032, supporting US nuclear fuel supply as reactor deployment grows.

6/8/2026 - Mongolia - Orano has started construction of the Zuuvch Ovoo uranium project in Mongolia, following a 2025 investment agreement with the Mongolian government. The project is expected to produce ~2,500 tonnes of uranium per year over a 30‑year mine life.

6/9/2026 - India - Fuel for the initial loading of Kudankulam Unit 4 has been manufactured and accepted by NPCIL, marking a key milestone toward commissioning of the VVER‑1000 reactor.

6/9/2026 - Australia - Ampera will use thorium sourced from Australia to fuel its advanced microreactor systems, supporting its strategy to vertically integrate fuel supply and in‑house TRISO fuel production.

6/12/2026 - Canada - Denison Mines has marked the start of site preparation and early construction at the Phoenix ISR uranium project in Saskatchewan, following final regulatory approvals and a positive investment decision. The project is targeting first uranium production in mid‑2028.

6/17/2026 - UK - The UK will guarantee a £210 million loan to support Urenco’s supply of enriched uranium to Energoatom, helping secure fuel for Ukraine’s nuclear fleet over the next two years.

6/17/2026 - Sweden - Sweden’s parliament has approved amendments to nuclear legislation that streamline permitting for uranium mining and open up more coastal locations for potential nuclear projects, further supporting the country’s plans to expand nuclear power and domestic fuel supply.

6/18/2026 - United States - Shine and Newcleo have agreed to collaborate on recycling used nuclear fuel, linking Shine’s fuel‑reprocessing technology with Newcleo’s reactors and MOX fuel capabilities to support a closed nuclear fuel cycle.

6/19/2026 - United States - Centrus has agreed to supply HALEU to Oklo for up to five Aurora reactors, with deliveries expected to begin in 2029 from its Ohio enrichment facility. The agreement strengthens fuel supply certainty for Oklo’s planned reactor deployments and is among the first large‑scale commercial HALEU supply agreements in the US.

6/24/2026 - Russia - Rosatom is studying the construction of a high‑capacity nuclear fuel reprocessing plant with an initial capacity of 400 tonnes per year, with investment and site selection decisions expected by the end of 2026.

6/25/2026 - United States - Lightbridge has removed the first batch of its irradiated fuel samples from Idaho National Laboratory’s Advanced Test Reactor, marking a key milestone in the testing of its advanced nuclear fuel technology. The samples will now undergo post‑irradiation examination to support fuel performance validation and future regulatory licensing efforts.

6/26/2026 - Italy - Italy’s Sogin has begun re‑encapsulating 64 uranium‑thorium fuel elements at the Rotondella site for long‑term dry storage, marking a key decommissioning milestone for the facility.

6/26/2026 - United States - US uranium production more than doubled in 2025 to 1.39mn lbs U3O8, the highest level in nine years, according to the EIA, also uranium exploration and development drilling reached their highest levels since 2013.

6/30/2026 - United States - Urenco USA has brought a fifth new enrichment cascade online at its New Mexico facility, as part of a program to add 700,000 SWU of capacity by early 2027. The expansion is progressing ahead of schedule and on budget.

7/1/2026 - United States - The US NRC has renewed the source materials licence for enCore Energy’s Dewey Burdock uranium project for another 20 years, completing the federal permitting process for the South Dakota ISR project. The company is now pursuing final state permits ahead of construction and future production.

7/3/2026 - United States - Radiant has delivered the first TRISO fuel shipment for testing of its Kaleidos microreactor at Idaho National Laboratory, enabling full‑power, full‑temperature testing this summer. The testing programme will support performance validation and help advance the reactor’s commercial licensing pathway.

7/9/2026 - India - Australia and India have finalized the arrangements needed to enable Australian uranium exports to India for peaceful civilian use under their long‑standing nuclear cooperation agreement. The deal opens a new uranium supply source for India and supports its plans to expand nuclear power generation.

7/9/2026 - Finland - Framatome has signed an eight‑year fuel supply agreement with TVO for Finland’s Olkiluoto 3 (OL3) reactor, strengthening long‑term fuel security for the plant. The deal also includes an option to adopt Framatome’s GAIA fuel design and supports longer operating cycles of up to two years at OL3.

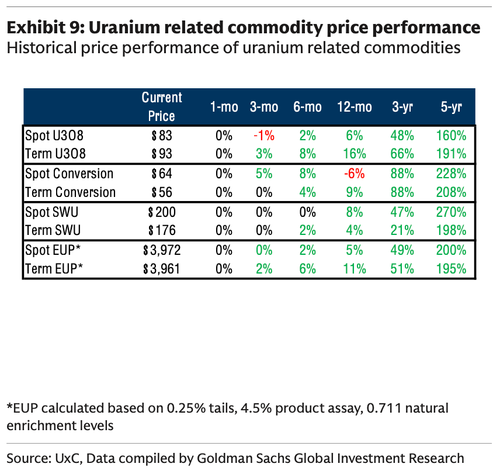

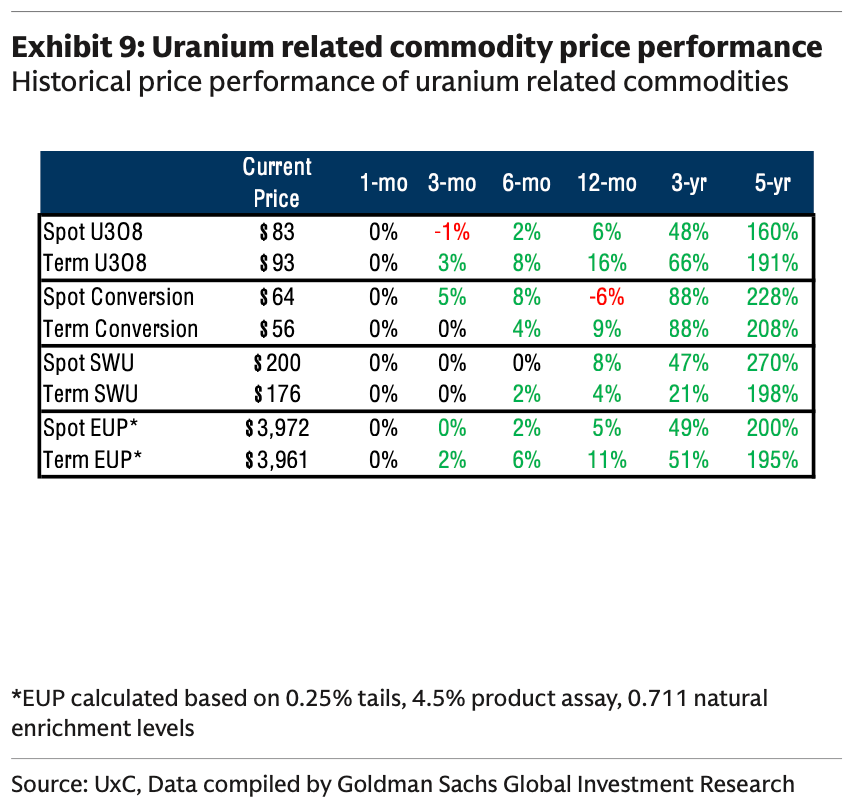

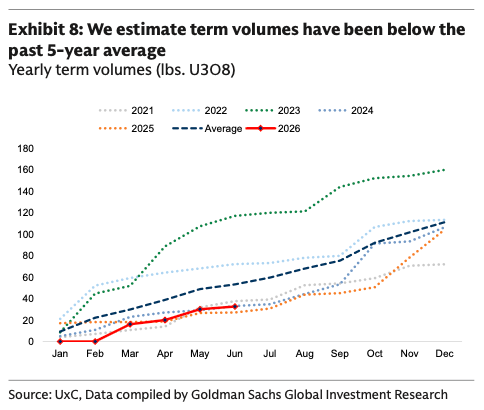

Uranium pricing and volume trackers

Spot pricing remained broadly range-bound. Spot U3O8 prices softened through early June, easing from ~$86/lb to the mid‑$84s before recovering into the mid‑$85s through the middle of the month. Prices drifted modestly lower again toward month‑end, finishing June around ~$85/lb and remaining largely unchanged through early July. Market activity was subdued throughout the period, with trading volumes concentrated in a limited number of transactions and overall price movements remaining relatively narrow.

Term pricing firm. Term pricing strengthened through June, with the long‑term price increasing to $94/lb by end of June from $93/lb at the start of the month, reinforcing the view that longer term pricing remains well supported despite softer spot market activity. Market engagement continued across the term market, with utilities evaluating mid‑ and long‑term supply requirements and several new contracting opportunities emerging. Overall, longer‑dated price indicators remained resilient, with forward prices continuing to reflect supportive long‑term market fundamentals.

Tyler Durden

Mon, 07/20/2026 - 05:45

In a supplied image, fish found on board Chinese longlining vessel, the Lu Rong Yuan Yu 138, at the time it was detained for alleged illegal fishing in NA, Tuvalu on July 9, 2026 PR Image/Supplied by Sea Shepard

In a supplied image, fish found on board Chinese longlining vessel, the Lu Rong Yuan Yu 138, at the time it was detained for alleged illegal fishing in NA, Tuvalu on July 9, 2026 PR Image/Supplied by Sea Shepard

A United States Border Patrol agent enters through the United States border wall outside of San Diego, on Jan. 20, 2026. John Fredricks/The Epoch Times

A United States Border Patrol agent enters through the United States border wall outside of San Diego, on Jan. 20, 2026. John Fredricks/The Epoch Times

Amy Kremer is the cofounder of Women for Trump and Women for America First. Now she's taking on AI data centers. Jacquelyn Martin/AP

Amy Kremer is the cofounder of Women for Trump and Women for America First. Now she's taking on AI data centers. Jacquelyn Martin/AP

via Bloomberg

via Bloomberg

Recent comments