10 Sunday Reads

Avert your eyes! My Sunday morning look at incompetency, corruption and policy failures:

• The House of Ellison is on the Brink: Everything the world’s briefly richest man built is failing at once. Notes From the Circus on the Ellison media empire’s mounting troubles — Paramount, the debt load, and the succession questions nobody at the top wants to answer. (Notes from the Circus)

• Mark Cuban on Breaking the Drug Pricing Cartel: Inside Cost Plus Drugs: The Pear Healthcare Playbook interviews Cuban on how Cost Plus Drugs is forcing transparency into pharmaceutical pricing — and why the PBM cartel should be worried. (Pear Healthcare Playbook) see also How Mark Cuban Cost Plus Drugs Is Creating a New Public Benchmark for the American Pharmacy Market: The companion analysis — Cost Plus prices are becoming the reference point that exposes everyone else’s markups. (Jeremiah Franklin Shrack)

• The Real Reason that Substack is Collapsing: Scott Carney’s inside account of the platform’s decline — the recommendation engine changes, the AI slop flood, and the economics that stopped working for everyone but the top 1% of writers. (Scott Carney)

• “God has helped us, and so will AI”: How the Terrorist Group Boko Haram Uses Frontier AI. How are terrorists using AI? Semi-structured interviews with 27 former Boko Haram members conducted in northeast Nigeria in 2025 and 2026 reveal unprecedented detail about AI-assisted terrorist activity primarily through 2024. This report finds that both factions of Boko Haram use frontier AI, including ChatGPT, Claude, Gemini, Grok, Meta AI, and DeepSeek, to assist in combat and day-to-day operations. This AI use is institutionalized through specialized units and internal training. It has aided in attack planning, weapons troubleshooting, and the design of explosive devices, as users have successfully circumvented some safeguards.Not everyone in financial markets watched Fed chair Kevin Warsh’s presser yesterday. But today everyone will be dealing with its consequences. As MainFT reports, US borrowing costs surged to a 19-year high in the one-day biggest jump since Trump’s “liberation day” tariff announcement. Equity markets shedding a mere trillion-odd dollars look a bit meh by comparison. (University of Cambridge)

• Why does everything feel so joyless? Welcome to the age of decadence without pleasure: The Guardian’s interactive essay on cultural exhaustion — we have infinite entertainment, unprecedented abundance, and a pervasive sense that none of it is fun anymore. Decadence in our era comes in technologically mediated forms, emptied of desire and obsessed with self-optimisation (The Guardian) see also We used to be able to buy things in this country: Danny Katch on the quiet degradation of American consumer life — the fees, the subscriptions, the enshittified everything, and the political rage it’s generating. Locking up toothpaste was a warning sign that our executive class was crazy (Revolution for Cowards)

• Mapping Trump’s crypto empire: Citation Needed maps the full scope of the president’s cryptocurrency holdings, business relationships, and policy influence — the conflicts of interest visualized. A new data project maps the Trump family’s web of cryptocurrency ventures, which have been generating billions in income for the president. (Citation Needed)

• Big Tech AI Spree Revives Accounting Devices That Toppled Enron: Enron Corp. exploited US accounting rules to hide from investors and lenders hundreds of millions in debt it had bundled into off-balance sheet entities — obligations that contributed to one of the biggest corporate collapses in US history. Twenty-five years later, new risks have emerged as some of the world’s most valuable companies create similar financing vehicles that can mask how much debt they’re taking on, as the technology industry looks to spend more than $3 trillion to power artificial intelligence systems. Off-balance-sheet entities are back. Twenty-five years after Enron, tech giants are using strikingly similar structures to hide the debt financing their AI data center buildouts. (Bloomberg Tax)

• A big week for AI denialism: In the wake of OpenAI’s cyberattack against Hugging Face, few seem ready to acknowledge the implications. Last week, we learned that a group of OpenAI models broke out of their test environment and hacked into Hugging Face to steal the answers to a benchmark they were being tested on. It’s the first publicly known case of an autonomous AI agent system designing and successfully executing an attack like this, and the fallout is stretching into this week. Platformer on the growing chorus claiming AI is all hype — and why both the boosters and the deniers are missing what’s actually happening. In the wake of OpenAI’s cyberattack against Hugging Face, few seem ready to acknowledge the implications (Platformer)

• The fake historian advising Trump’s anti-Smithsonian crusade: Despite having no degree in history, David Barton calls himself a historian. He has amassed a large collection of documents related to America’s founding and published several books. For decades, he has pushed the view that the founding fathers never intended for there to be a separation between church and state. David Barton’s work has been rejected repeatedly by actual historians. Most notably, a book he published in 2012 about Thomas Jefferson was pulled from the shelves by its publisher after a group of historians from Christian universities accused him of including distortions and false information. Popular Information exposes the credentials of the “historian” shaping the administration’s museum purge — the résumé doesn’t survive contact with fact-checking. (Popular Information)

• The Putinization of the American Military: Krugman on the loyalty purges, political generals, and the transformation of the U.S. military into an instrument of personal power — the Russian model, imported. When poseurs and yes-men run a war (Paul Krugman) see also How Russia Uses Sexual Violence to Wage War: The Wall Street Journal documents the systematic use of sexual violence as a weapon of war by Russian forces in Ukraine. The evidence is overwhelming and the accountability is nonexistent. Evidence suggests sexual abuse of Ukrainian men is now a core Russian tactic (Wall Street Journal)

Video of the day: Why does every mammal get 1 billion heartbeats in their life?

Be sure to check out our Masters in Business interview this weekend with Som Seif Purpose Investments, founder/CEO, Toronto-based asset manager launched in 2012. He grew his first firm, Claymore Investments to $8B in assets by creating 34 ETFs over 6 years, establishing it as Canada’s leader in low-cost exchange-traded funds; he sold to BlackRock in 2012. Next, he co-founded Wealthsimple, which became the default investing app for a generation of Canadians. His wealth management firm, Purpose, was founded at the end of 2012, and manages>$31B in ETFs, mutual funds, alternatives, private assets, and digital assets. Som was named to Canada’s Top 40 Under 40 in 2011.

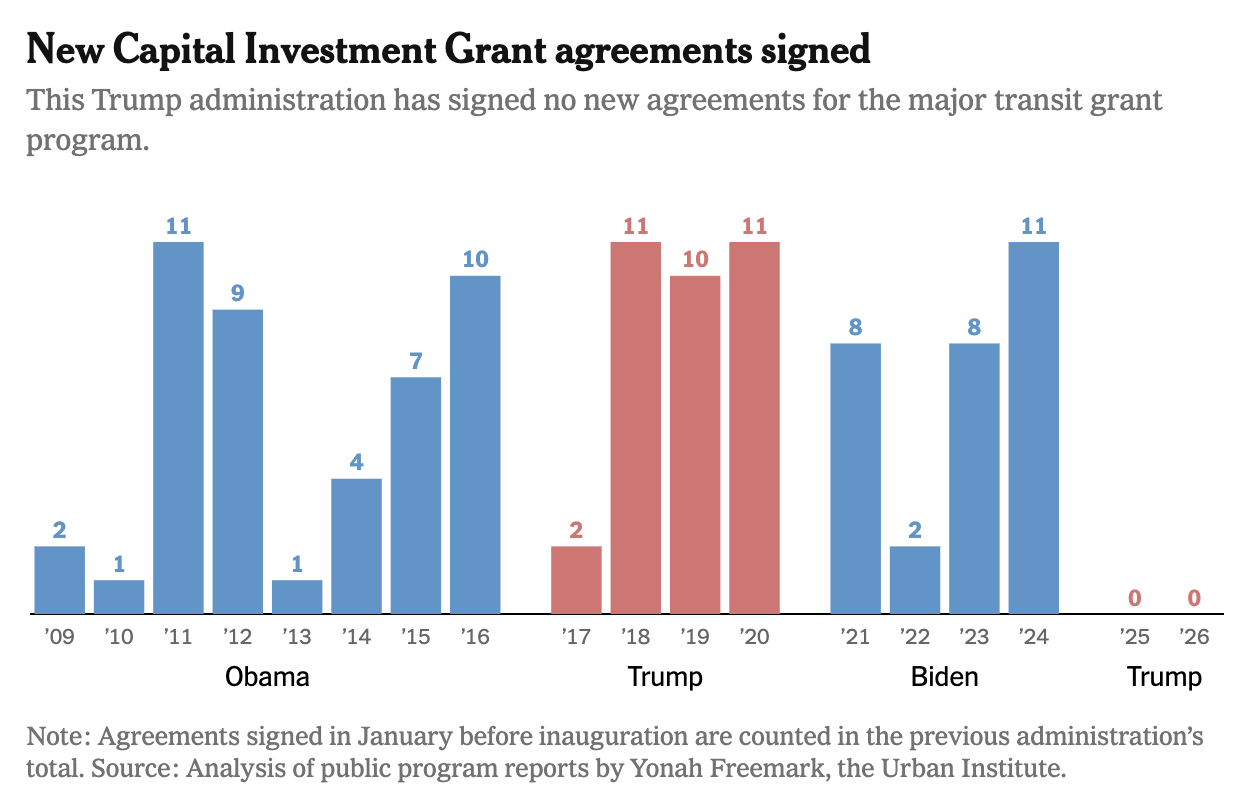

Congress Budgeted Billions for Big Transit Projects. Trump Isn’t Spending It.

Source: New York Times

Sign up for our reads-only mailing list here.

~~~

To learn how these reads are assembled each day, please see this.

The post 10 Sunday Reads appeared first on The Big Picture.

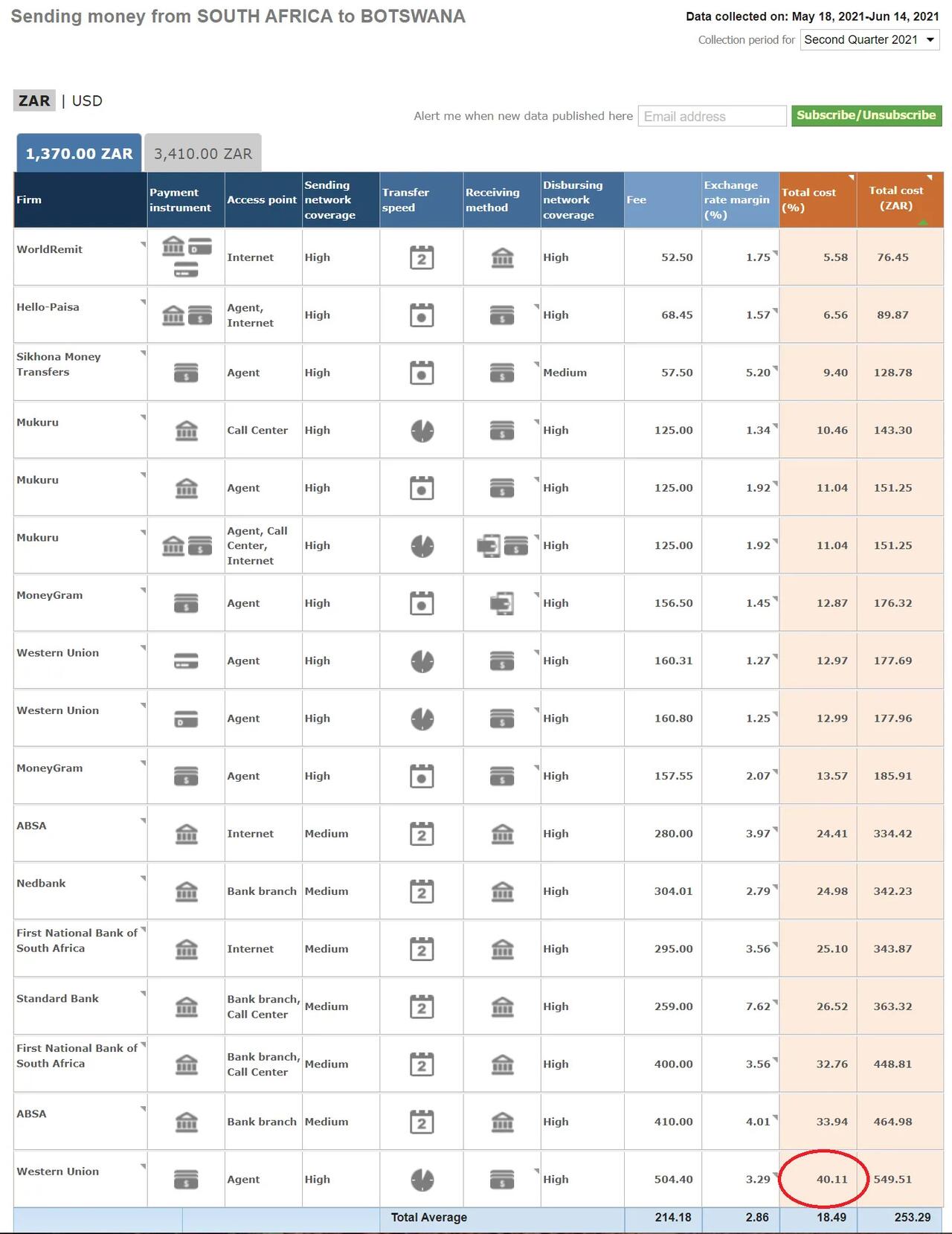

Western Union charges as high as 40,11% for a ~$84 USD remittance from South Africa to Botswana. Data from the World Bank, Q2 2021.

Western Union charges as high as 40,11% for a ~$84 USD remittance from South Africa to Botswana. Data from the World Bank, Q2 2021.

President Xi Jinping reviews troops during a massive military parade that showcased the PLA’s latest arsenal, in Beijing on September 3, 2025. Photo: Xinhua

President Xi Jinping reviews troops during a massive military parade that showcased the PLA’s latest arsenal, in Beijing on September 3, 2025. Photo: Xinhua

via AP

via AP An instructor teaches a student about brazing—a metal joining process used in heating, ventilation, and air conditioning systems—at a construction trade school in Homestead, Fla., on May 9, 2026. Joe Raedle/Getty Images

An instructor teaches a student about brazing—a metal joining process used in heating, ventilation, and air conditioning systems—at a construction trade school in Homestead, Fla., on May 9, 2026. Joe Raedle/Getty Images Students attend a heating, ventilation, and air conditioning class at a construction trade school in Homestead, Fla., on May 9, 2026. Recent statistics show that people are exploring alternatives to the four-year degree, with many opting for trade schools. Joe Raedle/Getty Images

Students attend a heating, ventilation, and air conditioning class at a construction trade school in Homestead, Fla., on May 9, 2026. Recent statistics show that people are exploring alternatives to the four-year degree, with many opting for trade schools. Joe Raedle/Getty Images

A tour guide stands near a display showing images of people at locations described as vocational training centers in southern Xinjiang at the Exhibition of the Fight Against Terrorism and Extremism in Urumqi in the Xinjiang Uyghur Autonomous Region in China on April 21, 2021. Mark Schiefelbein/AP Photo

A tour guide stands near a display showing images of people at locations described as vocational training centers in southern Xinjiang at the Exhibition of the Fight Against Terrorism and Extremism in Urumqi in the Xinjiang Uyghur Autonomous Region in China on April 21, 2021. Mark Schiefelbein/AP Photo Chinese police detain a journalist at a checkpoint on the road to the riot-affected Uyghur town of Lukqun, Xinjiang Province, China, on June 28, 2013. Mark Ralston/AFP via Getty Images

Chinese police detain a journalist at a checkpoint on the road to the riot-affected Uyghur town of Lukqun, Xinjiang Province, China, on June 28, 2013. Mark Ralston/AFP via Getty Images

Recent comments