"The Polycrisis Of 2026 Whirls Like A Demon-Infested Storm Overcoming This Human Project..."

Authored by James Howard Kunstler,

Struggle session“. . .there is no saving the Left. There is only saving America from them.” — Sasha Stone

The polycrisis of 2026 whirls like a demon-infested storm overcoming this human project of ours like a medieval panorama of the world’s end. Everything is fraught, tilting toward hazard, menace, ruin. Even under a summer sun, the mind sees only darkness everywhere it looks.

Apocalypse now, it seems like.

You almost can’t blame the doomers, the black pill-ers, lost in their transports of dread.

But I tell you, we will get through this.

Is it a surprise that the IRGC has a death wish for its host, Iran? They’ve been advertising it loudly for half a century, yearning for martyrdom, the bliss of paradise, marriage to multiple perfumed virgins, all the pomegranates you could ever want, and perpetual dreamtime beside a gently burbling fountain in the palace of eternity. Trouble is, to get there you must have your head blown off.

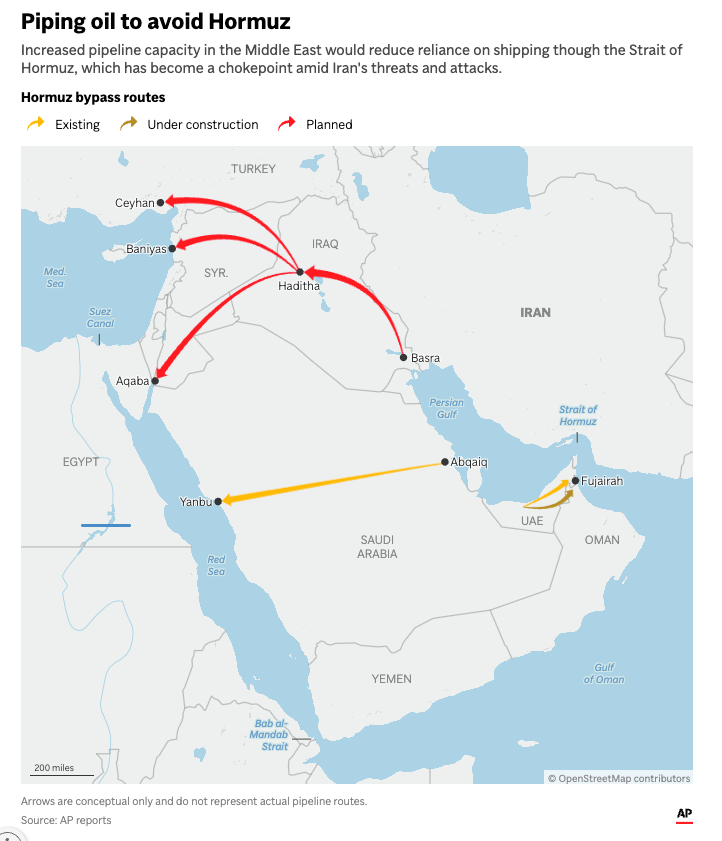

That’s exactly what the IRGC is asking for, though the millions of ordinary Iranians probably have their doubts about the ask. They are hostages of the IRGC regime, which refuses to just stop being a problem for the world. Mr. Trump’s proffer for Iran still abides: become a normal nation, sovereign and all, only without atom bombs. Let ships sail through Hormuz unmolested. Sell your oil, make some money, trade with the other fellas across the Persian Gulf, have a nice civilized life with all the refinements of age-old Persian culture, even with its Islamic overlay. Be happy!

The USA does not seek to occupy Iran, steal its resources, subjugate its people, force them to buy Minnie Mouse plush toys, play baseball, eat Jimmy Dean sausage for breakfast, strum banjoes, or wear cowboy hats. Just stop projecting violence and discord all over the Middle East.

You can’t make us, the IRGC says. Yes, we will, the USA replies. And so it goes. Next up: bridges and power plants. Plus, every ship you damage, we’ll deduct the cost of repair from your frozen assets held in our banks. This is where things stand after the thirteenth night of strategic bombing against the IRGC’s launch sites, drone factories, missile storage caverns, and shoreline military installations. Iran prepared assiduously for this death-scene for decades, building hidey-holes here, there, and everywhere. But every time they launch something now, our satellites mark the coordinates, and boom, now there’s one less hidey-hole.

Iran’s currency, the rial, has an exchange rate against the US dollar of about 1,900,000 to one dollar. There is hardly a functioning economy left. The people are flat broke. Everyday life must be hell now. Could be the IRGC was getting tons of munitions and material for free from China, but days ago we blew up the railroad bridge at Aq Tekeh-Khan that was China’s main connection to Iran, so that’s over with.

You must doubt that Russia is capable of sending arms to Iran at this point. Russia needs every drone and missile it can fabricate now that Ukraine is sending drones clear into Moscow and St. Petersburg on a regular basis. Of course, that war is being stoked by NATO, which perforce includes the USA. A bill (H.R. 2913 — the Ukraine Support Act) that would furnish $1.3-1.8 billion in direct security, military, and reconstruction assistance for Ukraine plus $8 billion in loans was passed by the House in June, but languishes in the Senate. President Trump has threatened to veto it, as running counter to the administration’s preference for negotiations with Russia to end the Ukraine War rather than extend it.

These two conflicts must seem intractable for now, but the mojo driving them has clear and present limits.

If the USA does not underwrite Ukraine’s war effort, then that leaves the EU nations, who are increasingly broke, and for all their idle talk are really incapable of mounting a major arms production campaign.

The UK especially is skating on thin ice these days as Mr. Trump methodically cancels its long-running command and control of global finance through the City of London (as its “Wall Street” is called). In fact, it looks as if the floundering UK — with dopey Andy Burnham rolling in as Britain’s seventh Prime Minister in a decade — has passed the ball of globalist leadership to its forward striker (and all-purpose fixer) Mark Carney the Prime Minister of Canada.

Carney, who was previously chief of the Bank of England, has played a series of losing games against President Trump the past year, while Mr. Carney is busy wrecking the Canadian economy for the sake of the globalist “green” flimflam, a sustained high volume of third world immigration, and outlandish DEI activism that includes giving vast tracts of real estate back to Canada’s First Nations people, their Indians. Carney has also very actively played footsie with the CCP to a degree that is seriously pissing off Mr. Trump. Among all the other shocks and surprises upcoming, you might imagine him having to send the 82nd Airborne up to Ottawa to inform PM Carney that there will be no globalist seat of operations in North America.

Yes, things are getting that strange. And then, continuing the clean-up operation south of our border, there is Cuba to straighten out. Cuba is obviously next. Our patience with that failing state’s communist export project is particularly thin, now that the Democratic Party here is entertaining Marxist-Leninist dreams of glory.

On top of all that, we have serious concerns with the financial markets and the widening income inequality that drives the younger generations’ yen for “socialism” (free rent, free medicine, free stuff).

Financialization concentrates and compounds wealth while the salary-mule class stagnates, suffers, goes broke, and nurses its grievances.

We’re pushing into the season of financial train wrecks. AI has cornered all the free capital in the land — for something that appears to be an existential menace as much as any potential economic benefit — and it is wildly perverting the equity market. The bond market groans under the debt burden and the impossibility of fiscal prudence. Capitalism that can’t self-correct invites financial and political violence.

It’s probably a greater threat to us than the faraway wars, bad as they are. Mr. Trump, Secretary Bessent, and others in charge surely know this — that the American ownership class has become tiny, and that the cure for that is getting the vast dis-owned, forsaken middle-class back into businesses that they will own, in an economy based on production of real goods, not on playing games with money.

There is so much to be done and we can get it done if we screw our heads back on.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of ZeroHedge.

Tyler Durden Fri, 07/24/2026 - 16:20

Handout satellite image courtesy of Vantor shows tunnel entrances at a missile complex in Isfahan, in central Iran. via Vantor/AFP

Handout satellite image courtesy of Vantor shows tunnel entrances at a missile complex in Isfahan, in central Iran. via Vantor/AFP

Chickens, turkeys, and cows at Polyface Farms, in Swoope, Va., and The Family Cow, in Chambersburg, Pa., in these file photos. The regenerative farms are part of a growing push for “food emancipation”—neighbors feeding neighbors. Courtesy of Polyface Farms, Courtesy of The Family Cow

Chickens, turkeys, and cows at Polyface Farms, in Swoope, Va., and The Family Cow, in Chambersburg, Pa., in these file photos. The regenerative farms are part of a growing push for “food emancipation”—neighbors feeding neighbors. Courtesy of Polyface Farms, Courtesy of The Family Cow Customers wait at Raising Canes Chicken Fingers in Washington on March 12, 2026. In 2025, Americans spent around 55 percent of their food dollars on items prepared outside the home at restaurants, fast-food chains, and through takeout delivery services. Madalina Kilroy/The Epoch Times

Customers wait at Raising Canes Chicken Fingers in Washington on March 12, 2026. In 2025, Americans spent around 55 percent of their food dollars on items prepared outside the home at restaurants, fast-food chains, and through takeout delivery services. Madalina Kilroy/The Epoch Times

Recent comments