Jamie Dimon To Hold "Live Interactive Discussion" With Super-Rich Clients As SpaceX IPO Roadshow Commences

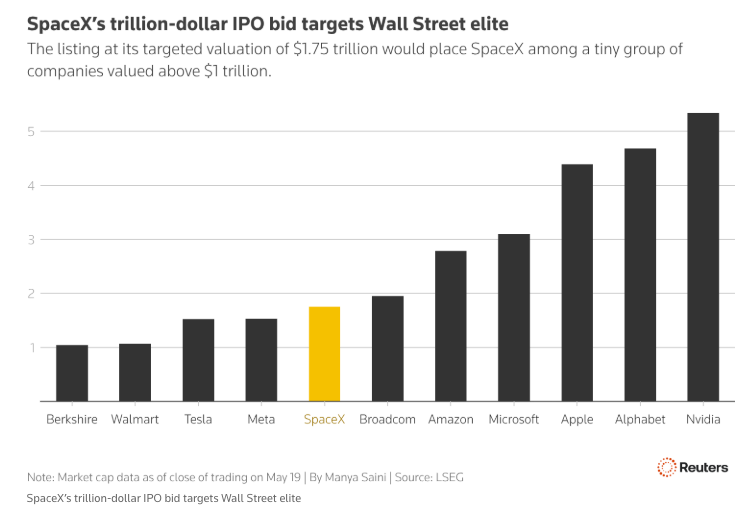

SpaceX is reportedly targeting a valuation of about $1.8 trillion as it prepares to go public next Friday, trading on the Nasdaq exchange under the ticker symbol SPCX.

Last month, Goldman Sachs was selected as the lead bank for the SpaceX listing, alongside Morgan Stanley. JPMorgan, Bank of America, and Citigroup are also among the 23 banks working on what will be the largest-ever listing, expected to raise a staggering $75 billion by selling about 555.6 million shares. The planned IPO price is about $135 per share.

Retail investors will be able to participate at the same prices as the big institutions. Expected SPCX price of $135 per share → https://t.co/eKBA0tzXbH

— SpaceX (@SpaceX) June 4, 2026

On Wednesday, we told readers that SpaceX's roadshow for institutional investors was set to begin on Thursday.

A new Bloomberg report states that JPMorgan CEO Jamie Dimon is set to hold a "live interactive discussion" later today. He will be joined by Mary Callahan Erdoes, CEO of the bank's asset and wealth management division, and two SpaceX executives: President Gwynne Shotwell and Chief Financial Officer Bret Johnsen.

The event will be streamed to 90 JPM locations across 26 states, according to Bloomberg sources, with more than 2,500 of the bank's clients expected to watch.

JPMorgan's nationwide roadshow for SpaceX shows that demand is extending deep into the private-wealth client base for this once-in-a-generation listing.

With the SpaceX roadshow underway, Morningstar equity analyst Nicolas Owens attempted earlier this week to temper the hype around the listing by publishing a note saying, "We think the company has been significantly overvalued and investors will have opportunities to buy the stock at more attractive levels after the IPO."

Meanwhile, Polymarket odds for "SpaceX IPO closing market cap above ___?" currently stand at 89% for a market cap above $1.8 trillion.

//--> //--> SpaceX IPO closing market cap above $1.8T?Yes 89% · No 12%

View full market & trade on Polymarket.

SpaceX's listing next week will pave the way for other mega IPOs, such as those of chatbot makers OpenAI and Anthropic.

Tyler Durden Thu, 06/04/2026 - 09:30

Recent comments