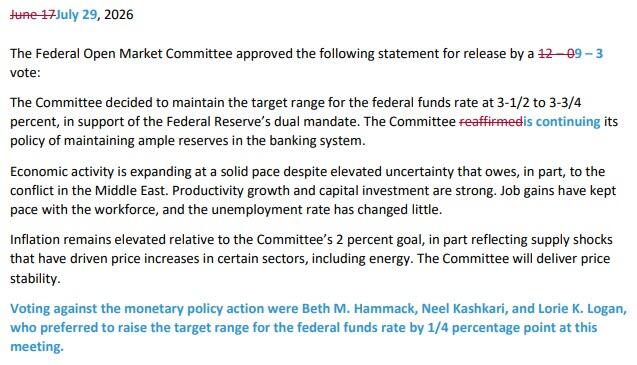

Idaho's High Desert Becomes Hot Spot For Nuclear Power Revolution

Authored by John Haughey via The Epoch Times,

History was made with the flip of a switch at 12:30 a.m. on June 4, under partly cloudy skies and a waning three-quarter moon in Idaho's Arco Desert, when a prototype reactor sustained a nuclear chain reaction, becoming the first new design to achieve "criticality," or viability, in the United States since 1973.

In that midnight milestone's wake, the future is following fast. Since Antares Nuclear's Mark-0 design was validated in early June, three other novel reactor designs have met the U.S. Department of Energy's criticality requirements and, according to Energy Secretary Chris Wright. Up to four more could do so by year's end.

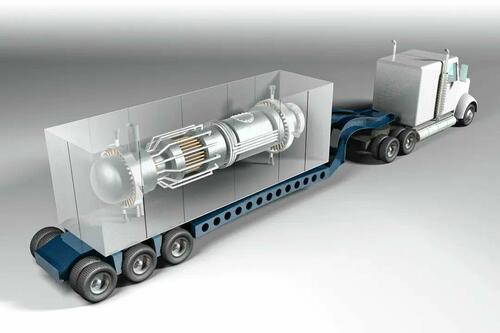

While technologies, fuels, and applications vary, these prototypes share common traits. All are far smaller than the conventional reactors with massive cement cooling towers, and all are designed to be mass-produced, portable, and scalable. Several can fit in the bed of a pickup truck.

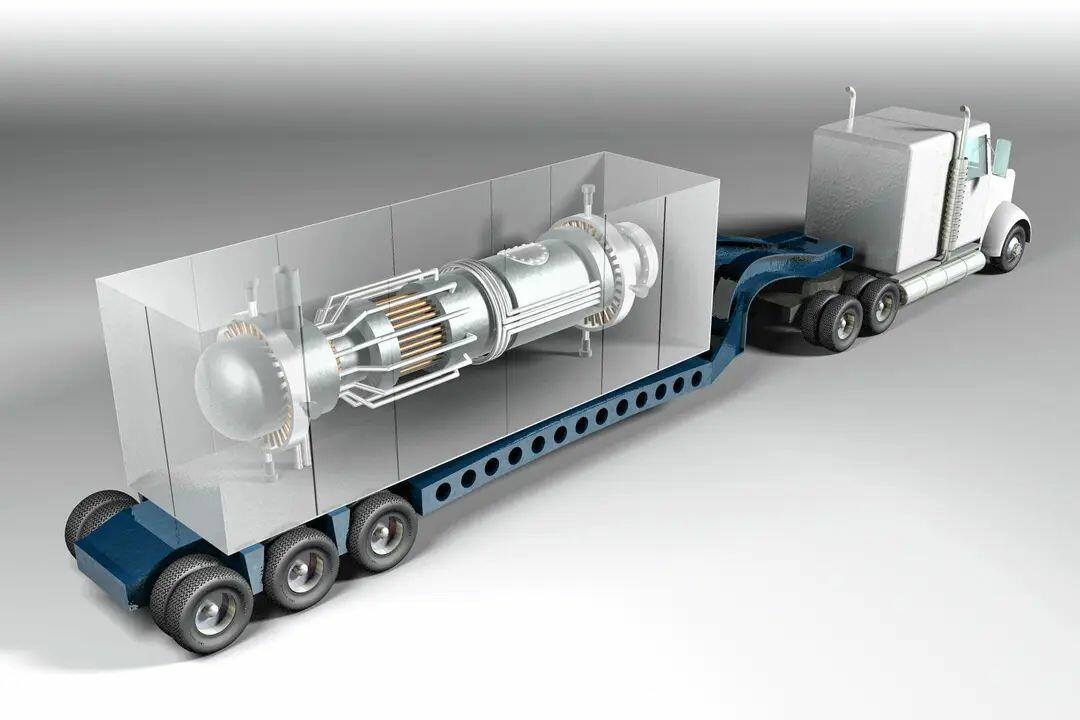

Most microreactor designs could be built in factories and shipped in cargo containers to locations around the world. Idaho National Laboratory

Most microreactor designs could be built in factories and shipped in cargo containers to locations around the world. Idaho National Laboratory

The nuclear energy surge is a convergence of rare bipartisan accord with stymied science and spiking electricity demand, spurred by power-hungry data centers and the integration of artificial intelligence and quantum computing into an electron-dependent world where the average U.S. home has 21 digital devices.

High-tech investors and hyperscalers are financing much of the innovation and pressuring the energy department to accelerate approvals to bring these new energy sources to market.

Not next decade.

Next year.

First-Movers

Antares Nuclear is one of 10 companies selected by the Department of Energy in August 2025 to develop "first mover" innovations under a reactor pilot program authorized by President Donald Trump. In four executive orders in May 2025, the president called for licensing 10 new reactors by 2030 and quadrupling the nation's nuclear energy capacity by 2050.

The United States maintains the world's largest nuclear power industry, with 96 reactors across 28 states that produce nearly 20 percent of the nation's electricity, according to the U.S. Energy Information Association.

But since 1990, while 18 reactors have been retired, only two new ones have been built in the United States, largely because of costs, long timelines, regulatory entanglements, and public perception after the Three Mile Island, Chernobyl, and Fukushima nuclear accidents.

Although deployments have languished for a half-century, nuclear technologies have advanced, with U.S. companies developing more than 30 new reactor designs. Meanwhile, successive administrations and Congress - in scarce consensus - have been deregulating and subsidizing the industry since 2024's ADVANCE Act adoption to meet a projected 25 percent increase in electricity demand by 2030 and more than 70 percent increase by 2050.

Criticality, a no-power proofing of theoretical physics, is generally the first step in being licensed by the Nuclear Regulatory Commission to produce and sell commercial nuclear reactors.

Trump's executive orders overhaul the commission and streamline approvals, meaning new reactors could be for sale within six months to a year, Wright said on June 25 in Idaho Falls after meeting with developers at the Idaho National Laboratory.

Qualifying for the pilot reactor program launched by Trump's executive orders, or for enrollment in the energy department's newly established nuclear launchpad program, gives developers access to the Idaho National Laboratory, an 890-square-mile sagebrush sprawl in the Arco Desert, where atomic power was first used to create electricity in 1951. Specifically, they gain access to the Materials and Fuels Complex, a 40-minute drive from the lab's Idaho Falls administrative offices.

Prototypes by Aalo Atomics and Valar Atomics also reached criticality under the pilot reactor program, while Deployable Energy did so as a launchpad participant. On criticality's "cusp" at the national lab and elsewhere are micro-reactors from Radiant Industries, Natura Resources, Last Energy, Atomic Alchemy, Deep Fission, and Oklo.

Antares Nuclear's Mark-O

When Antares's Mark-0 achieved functional viability on June 4, it became the 53rd reactor to reach criticality at the Idaho National Lab and the first non-lightwater reactor licensed in the United States since 1973.

The Torrance, California startup's shipping container-sized prototype, which utilizes sodium heat pipes for cooling without relying on external power, could produce up to 20 megawatts of electricity, or enough to power 15,000 homes, by 2027.

At the national lab on June 25, Wright told Antares CEO Jordan Bramble that seeing a structure where "wetted" sodium waste was treated transformed into a reactor test site in less than a year had made him so happy, he cried.

"I got emotional - emotional! - today to see the humans, the reactors, the steel, the action that's happening" at the lab site, he said. "To think on June 4 - less than 13 months after [Trump's executive orders] - that reactor ran critical [because] a three-year-old company said, 'Yes, we can. Yes, we will,' and leaned in."

Fueled by high-assay low-enriched uranium, Antares's prototype is in a 26-foot-deep, 26-foot-wide chamber and "over-shielded" under 11 cement slabs collectively weighing more than 200 tons.

Antares Communications Manager Kayla Haas said that when the company was founded in 2023, there were "three big things on the agenda": in 2026, secure Mark-0 criticality; in 2027, "produce electricity" with the next-generation Mark-1; and in 2028, "deploy reactors on customer sites."

"We're super excited to have checked the 2026 box," Haas said. "Now, we are shifting focus to our Mark-1 electricity-producing reactor that we'll test in 2027."

Backed by more than $140 million in private financing, Antares Nuclear owns a 322,000-square-foot plant in Southern California and offices in Aiken, South Carolina, and Idaho Falls. Its Mark-0 and Mark-1 reactors are ideally designed for defense and space applications.

The June 4 demonstration was conducted in partnership with Department of Defense nuclear fuels contractor BWX Technologies Inc. and observed by Pentagon officials. Antares is under contract to deliver micro-reactors to the U.S. Air Force's Joint Base San Antonio in 2027 and to the U.S. Army by September 2028.

Since 2025, Antares Nuclear has also been testing a 100-kilowatt reactor - enough juice for 65 homes - at NASA's Marshall Space Flight Center in Redstone Arsenal, Alabama, for potential use in space travel and as a moon base power plant.

The prototypes all share the same "base design," Antares Licensing Director Jason Andrus said, but testing in California, Idaho, and Alabama allows the company to integrate "learnings" into evolving designs and "do really kind of nerdy, nukey things."

Valar Atomics' Ward 250

Valar Atomics became the second to gain criticality, when its Ward 250 high-temperature, helium-cooled reactor sustained generation on June 18 at the San Rafael Energy Lab in Emery County, Utah. It is the only one of the four not to do so at the Idaho lab.

The El Segundo, California-based developer's 75-foot-long, 15-foot-wide micro-reactor could generate up to five megawatts of electricity, enough to power 5,000 homes, and be portable by truck, train, or plane. In February, the 120-ton Ward 250 was transported from California to Utah in a U.S. Air Force C-17.

Ward 250 is designed to be planted up to 80 feet underground and, because it is fueled by TRISO - a uranium fuel designed to prevent radioactive release - there's no need for large cement containment structures.

Valar followed criticality by using Ward 250 on July 1 to briefly power a website hosted on an Nvidia Blackwell AI chip. Nvidia is building a data center complex near Valar's factory in Orangeville, Utah, and has agreed to purchase up to 30 megawatts of electricity from the company by decade's end.

Deployable Energy's Unity

Houston-headquartered Deployable Energy's Unity reactor was the third new design, and second at the Idaho National Lab, to attain criticality in June, when it achieved operability at 11:55 p.m. on June 30.

Deployable founder and CEO Bobby Gallagher hauled Unity's reactor core, designed to fit in a 20-foot shipping container, from Texas to Idaho in a Ford F-150 pickup bed, proving its portability just by showing up at the lab.

The high-temperature, water-moderated, helium-cooled one-megawatt reactor - generating enough to power around 800 homes - is fueled with standard low enriched uranium, was built in partnership with Texas A&M University, and has drawn more than $10 billion in letter-of-interest queries "ranging from data centers to remote island community power," it maintains.

While one megawatt is not a lot of electricity, isolated communities, emergency responders, military installations, and industrial developers will see value in a reactor that can be "dropped in wherever you need it and left alone," Deployable Energy co-founder and Chief Commercial Officer Sanjay Mukhi said in late June, four days before Unity achieved criticality.

Deployable, which was only incorporated in 2025, was banking on that prospect when it was accepted into the reactor pilot program and arrived at the Idaho National Lab "150 days ago," he said, building a 340,000-square-foot structure dubbed "Studio 54," because it houses the 54th new reactor type to reach criticality at the lab.

Mukhi said one-megawatt reactors can be "scaled out" to meet tailored needs.

"We can deploy many at a time to meet the actual power requirements of specific sites," he said. "If you require 122 megawatts, instead of getting a 350-megawatt unit, you could actually get the exact power requirement and a little bit more."

The reactor, anchored in a 19-foot-deep basement chamber, looks like a laundry wash drum serrated by 696 holes where uranium rods will radiate heat in 63 gallons of water.

"It doesn't require a lot of water," Deployable co-founder and Chief Operating Officer Lance Maul said. "That's one of the other benefits to being able to go into different markets that have water restrictions."

Deployable's goal, he said, is to produce 1,000 reactors a year by decade's end and "by the mid-30s, 10,000 a year."

"That's the idea," Mukhi said. "From order to delivery, six months."

Aalo Atomics' Aalo-X

After Aalo Atomics of Austin, Texas, was selected to participate in the pilot program at the lab, the three-year-old startup's 200 employees built a 3,600-square-foot structure in 36 days. Then, over the next 40 days, they installed a 10-megawatt test reactor, which reached criticality 20 minutes into July 4.

"From founding to fission in under three years," Aalo spokesperson Ashley Cohen said. "One of the fastest reactor builds in modern American history."

It was the second-fastest build in history for a first-of-a-kind reactor, clarified Aalo co-founder and CEO Matt Lozak, and the swiftest in 80 years since Clementine, the world's first plutonium-fueled fast-neutron reactor, achieved criticality in November1946.

The test reactor is a full-scale prototype of its 20-foot-tall, 10-foot-wide Aalo-X micro-reactor - small enough to haul on a tractor trailer flatbed, big enough to power 10,000 homes.

Lozak projects that Aalo will be selling its next-generation 10-megawatt, 4.95 percent LEU-fueled Apollo X reactors at "commercial-scale" in 2027, and assembling its Aalo Pod power plants, which can house up to five 10-megawatt reactors, for commercial buyers by 2029 at its 40,000-square-foot Texas factory.

The Aalo Pod power plant will be mobile, won't need refurbishment for 40 years, and will be purpose-built to specifications - attributes the company says make it ideal for military, disaster response, and industrial applications.

Aalo co-founder and President Yasir Arafat noted that the Department of Energy has approved the company's request to build a data center on its national lab site.

"These things go hand-in-hand," he said. "AI is so power-hungry, and there's no better way to power AI than nuclear."

During a tour of the company's 2-acre site at the national lab, Lozak and Arafat said reaching criticality by July 4 would prove concepts key to their commercial model.

Mission accomplished.

"We proved all the major hard questions," Lozak said. "Can you construct? Yes. Can you build your reactor in a factory? Yes. We built our reactor in four weeks, did 80 percent of the installation within the first week in the factory, and shipped it across the country in two days."

Radiant Nuclear's Kaleidos

El Segundo, California-based Radiant Nuclear's one-megawatt Kaleidos reactor, designed to fit inside a 20-foot shipping container, is expected to reach criticality and then follow up with a 150-hour demonstration of sustained "hands off" operability this summer.

Kaleidos is installed in the Idaho lab's Demonstration of Microreactor Experiments (DOME), a 100-foot-tall structure on the Materials and Fuels Complex, where micro-reactors up to 20 megawatts were tested in the 1960s and '70s.

Radiant Nuclear President Tori Shivanandan said in late June that the company was engaged in "rigorous component testing on every single part of this system" it built inside the DOME.

The reactor's helium circulator, for instance, has received more than 150 start-stops "as though [it] just lost power" so the company can "understand that data prior to the system even shipping," she said. "We're still 'iterating' on the product."

There are five phases to reactor testing, Shivanandan said, "and we pause, we review the data, between each one."

Some Kaleidos components have undergone extensive testing at university labs nationwide, "but this will be the first time they're receiving dose under the full system, and so we want to again see 150 hours of what we call 'hands-off operations,' and monitor the environment, see what's going on," Shivanandan said.

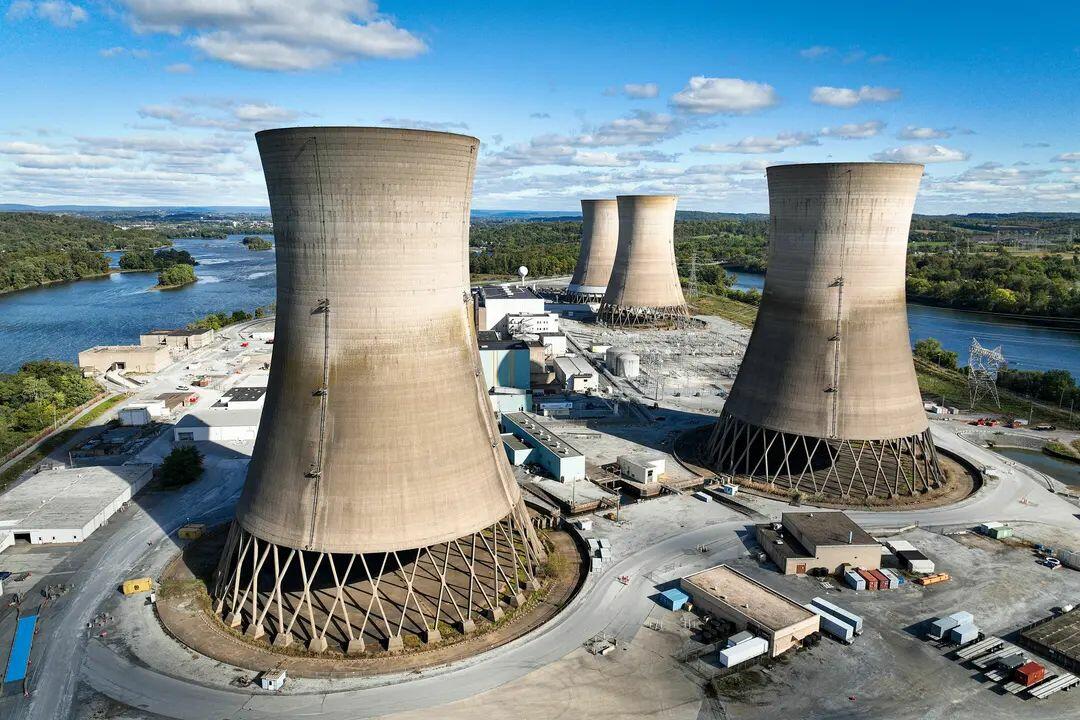

The shuttered Three Mile Island nuclear power plant stands in the middle of the Susquehanna River near Middletown, Pa., on Oct. 10, 2024. Since 1990, only two new nuclear reactors have been built in the United States, in large part because of public perception after nuclear accidents such as the 1979 partial meltdown at the plant. Chip Somodevilla/Getty Images

Tyler Durden

The shuttered Three Mile Island nuclear power plant stands in the middle of the Susquehanna River near Middletown, Pa., on Oct. 10, 2024. Since 1990, only two new nuclear reactors have been built in the United States, in large part because of public perception after nuclear accidents such as the 1979 partial meltdown at the plant. Chip Somodevilla/Getty Images

Tyler Durden

Wed, 07/29/2026 - 09:30

Lifeguards rescue boy at California beach amid intense waves

Lifeguards rescue boy at California beach amid intense waves

Aftermath of strikes on the Saudi Aramco refinery in Jizan from days ago, via AFP

Aftermath of strikes on the Saudi Aramco refinery in Jizan from days ago, via AFP

via Mappr

via Mappr

Most microreactor designs could be built in factories and shipped in cargo containers to locations around the world. Idaho National Laboratory

Most microreactor designs could be built in factories and shipped in cargo containers to locations around the world. Idaho National Laboratory

The shuttered Three Mile Island nuclear power plant stands in the middle of the Susquehanna River near Middletown, Pa., on Oct. 10, 2024. Since 1990, only two new nuclear reactors have been built in the United States, in large part because of public perception after nuclear accidents such as the 1979 partial meltdown at the plant. Chip Somodevilla/Getty Images

The shuttered Three Mile Island nuclear power plant stands in the middle of the Susquehanna River near Middletown, Pa., on Oct. 10, 2024. Since 1990, only two new nuclear reactors have been built in the United States, in large part because of public perception after nuclear accidents such as the 1979 partial meltdown at the plant. Chip Somodevilla/Getty Images

Recent comments