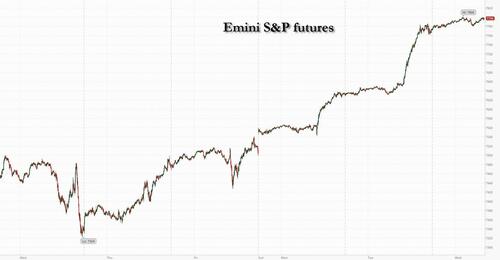

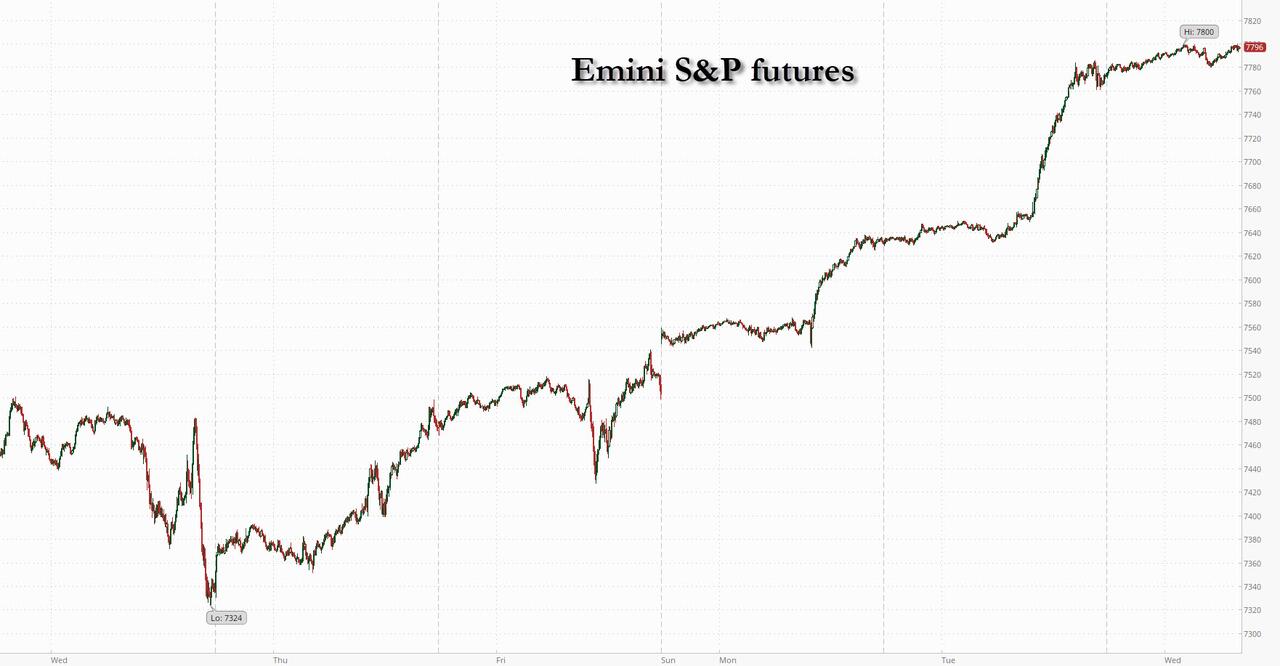

Futures Hit New Record High On Strong Earnings Following Historic Call Buying Frenzy

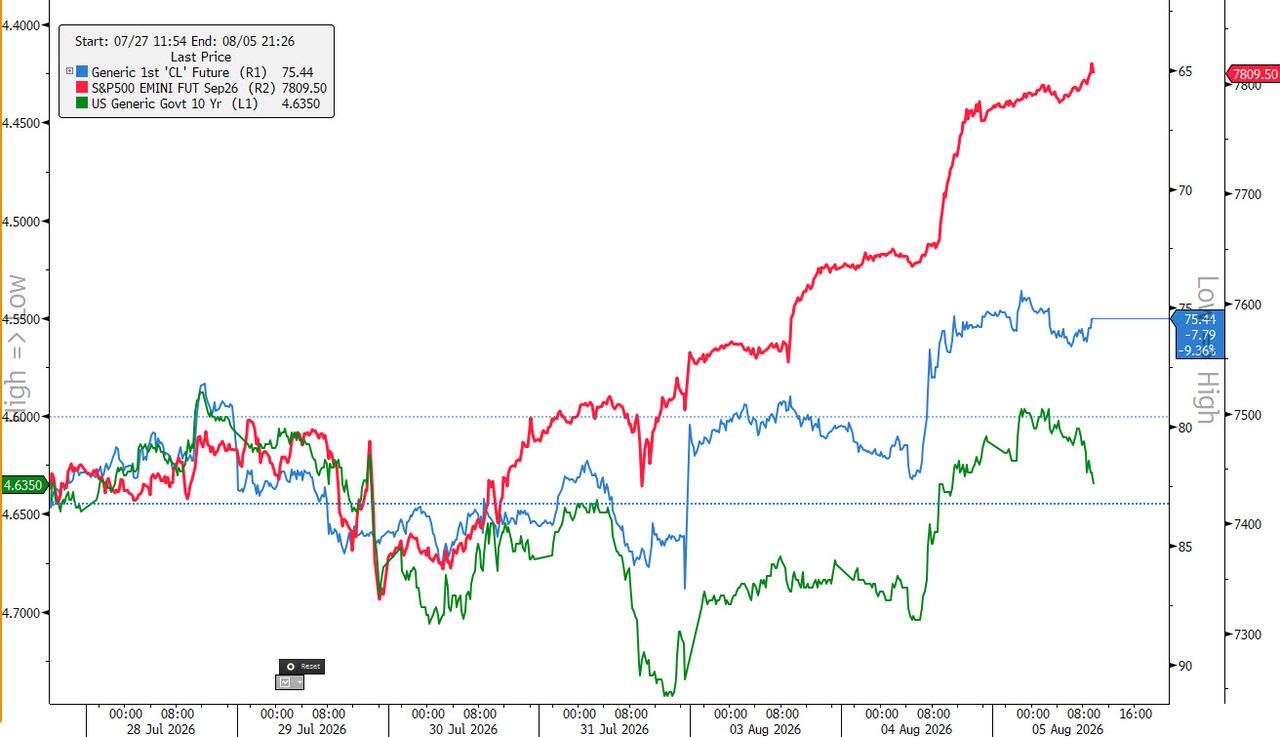

S&P 500 futures are up following yesterday’s first ATH since June; both tech and small caps are lagging, pointing to another potential broadening. A jump in US tech stocks is holding too, with Nasdaq-100 contracts rising after a 3.3% surge in the session before, powered by semiconductor stocks and blowout Palantir earnings. S&P futures are up 0.4%, just shy of 7800, a new all time high, while Nasdaq futures underperform, rising 0.2%, as results from AMD and SpaceX failed to impress, sending shares in both lower in after-hours trading. AMD’s forecast didn’t meet high expectations, while SpaceX investors focused on the hikes being made to its AI spending. Semis/memory are lower with some likely profit-taking after yesterday’s surge; NVDA/GOOG are leading Mag7 names higher as it appears that squeeze portion of this rally has room left to run, as JPM says keep an eye on IGV as the squeeze may turn into a narrative shift flipping one of the lightest owned sub-sectors into a leader in the near-term. Germany’s Infineon, up 69% this year, picks up the baton for European semiconductor sector results Wednesday. Tuesday gains have fed into a bounce for the Kospi and Nikkei 225 in Asia. Euro Stoxx 50 futures are also up 0.4%. The mood in stocks and in bonds has been bolstered by oil prices continuing to ease off, with Brent slipping below $79/bbl before rising above $80 as Houthi rebels threaten Saudi shipping north of the Red Sea and the UKMTO reported a ship sunk off Yemen after it was attacked by an unmanned craft. Qatar said a proposal had been drafted and both American and Iranian officials sounded hopeful about reopening the Strait of Hormuz.

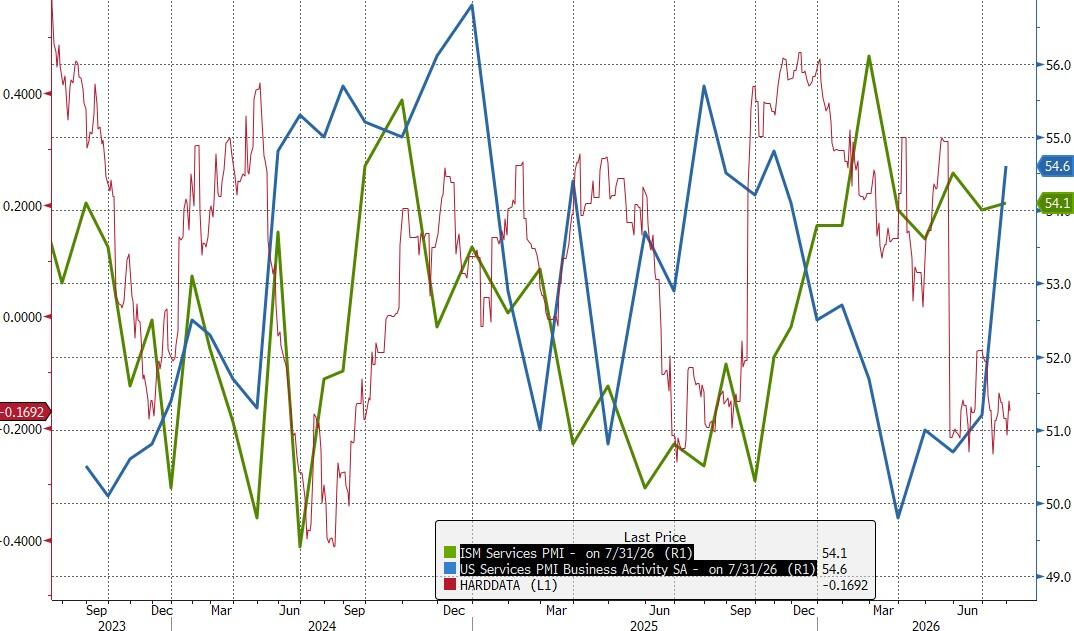

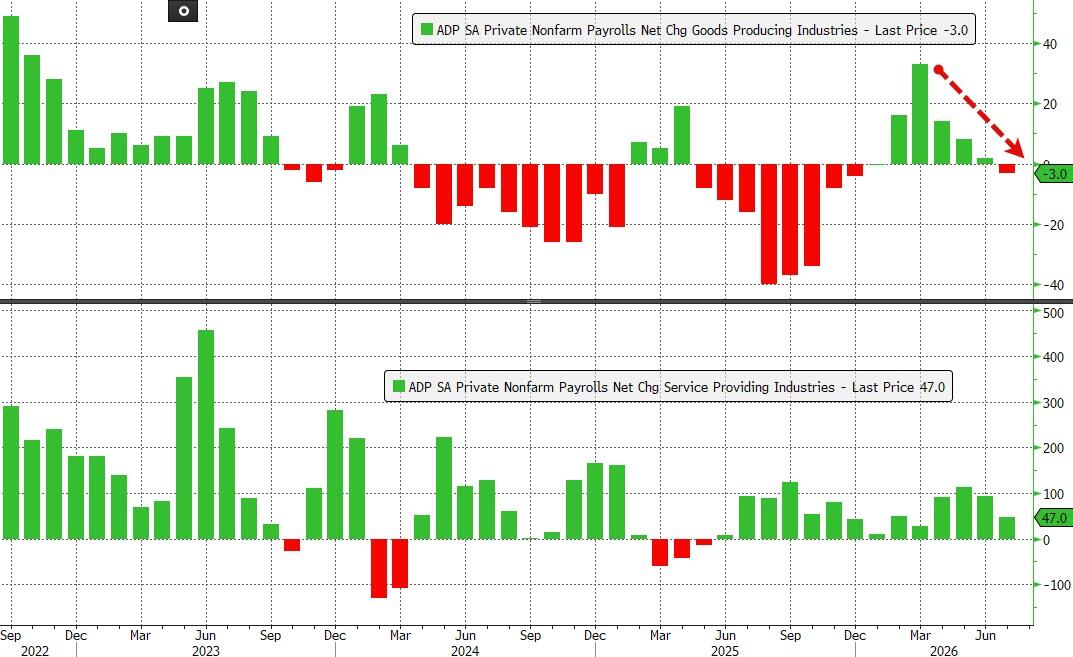

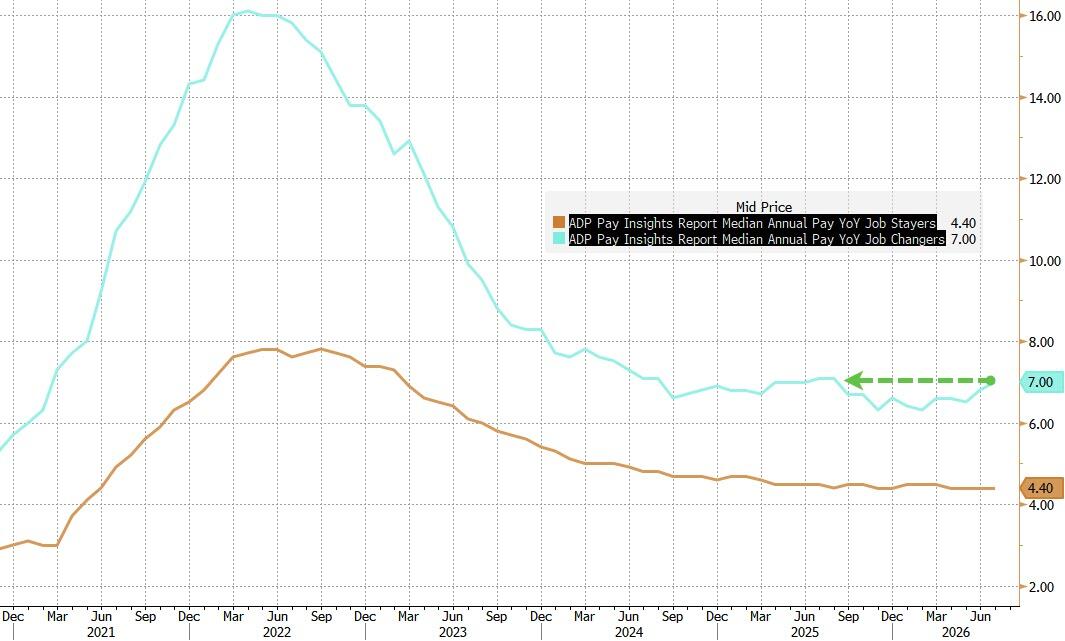

Treasury yields are dipping, while yields are down in Japan, Australia and New Zealand, the latter after weak quarterly jobs data. The Bloomberg Dollar Spot Index is softer, with the Swiss franc and Swedish krona leading gains among major currencies and the kiwi the laggard. Asia FX is green across the board.Commodities are bid, led by Precious Metals; WTI seeing support around $75/bbl though that could change following the expected formal announcement of a new deal between the US and Iran. Today's US economic data calendar includes July ADP employment change (8:15am), July final S&P Global US services PMI (9:45am) and July ISM services index (10am). Fed speakers scheduled include Cook (4:05pm) and Daly (8:35pm)

In premarket trading, Nvidia leads Mag 7 stocks higher, poised to extend gains for a fifth consecutive session, after SPCX announced an exclusive partnership to build its future AI infrastructure entirely on NVIDIA’s platforms. Meanwhile, Tesla is underperforming the cohort as SpaceX’s debut earnings after IPO disappoints. Other Mag 7 names are mostly higher (Nvidia +1.8%, Alphabet +1.2%, Apple +0.9%, Amazon +0.7%, Meta +0.5%, Microsoft +0.2%, Tesla -1.2%)

- AMD (AMD) falls 7% after the chipmaker’s third-quarter sales forecast underwhelmed investors expecting a stronger performance amid healthy demand.

- Arista Networks (ANET) jumps 12% after the cloud-networking company forecast better-than-expected revenue for the third quarter. Analysts note that demand remains very healthy.

- Booking (BKNG) is up 7% after the online travel agency reported gross bookings for the second quarter that beat the average analyst estimate. The company said healthy global travel trends continued into the third quarter despite the ongoing conflict in the Middle East.

- CVS Health (CVS) rises 3% after the health insurer boosted its adjusted earnings per share guidance for the full year.

- Digital Turbine (APPS) soars 27% after the mobile network company boosted its revenue guidance for the full year that topped the average analyst estimate and first-quarter results beat the consensus.

- Elanco Animal Health (ELAN) gains 6% after the animal health firm boosted its revenue and adjusted profit guidance for the full year, following better-than-expected results for the second quarter.

- Everus Construction (ECG) climbs 9% postmarket after raising its year revenue and Ebitda outlook. Second-quarter results topped expectations, with revenue growing 34% from the year-ago period.

- Flutter (FLUT), the parent of the FanDuel, falls 5% after the company cut its US revenue guidance for the full year and appointed President Dan Taylor as chief executive officer from Oct. 1.

- Kratos (KTOS) gains 10% after the defense contractor boosted its revenue guidance for the full year, topping the average analyst estimate.

- Match Group (MTCH) drops 8% after providing a revenue forecast for the current quarter that narrowly missed analysts’ estimates, suggesting its dating sites still need to attract more younger users.

- New York Times (NYT) falls 8% after the news company reported second-quarter results.

- Pinterest (PINS) drops 9% after the social media platform’s revenue outlook for the current quarter disappointed investors.

- Shopify (SHOP) climbs 28% after the e-commerce platform operator reported revenue for the second quarter that beat the average analyst estimate.

- SpaceX (SPCX) falls 11% after it disclosed higher-than-expected spending on its artificial intelligence business, overshadowing an inaugural quarterly report that broadly surpassed Wall Street forecast.

Other corporate news includes Paramount Skydance posting a surprise surge in profits with cost-cutting from its merger last year continuing to pay off. Lucid is targeting $1.4 billion in cash savings this year, as the EV maker’s new CEO says “tough medicine” is needed to fix the troubled firm.

Overnight, the micro highlight was SpaceX's first earnings report as a public company, which could have gone... better: shares are 10% lower in premarket trading after it disclosed higher-than-expected spending on its AI business, dampening a report that broadly surpassed forecasts. Overall capex jumped to about $18.4 billion in the quarter, more than double its $7.8 billion revenue, and the company said the next two quarters of spending will be similar. Meanwhile, Musk lived up to his reputation for making bold predictions, including that SpaceX would reach a $100 billion annual run-rate revenue by year’s end, and $1 trillion annual revenues by 2030. SpaceX also fleshed out its plans to take on AT&T, Verizon and T-Mobile by complementing its satellite-based internet service with land-based infrastructure (telecom stocks tumbled).

The next catalyst for tech - and probably the entire market - comes in the form of results from memory chip makers Sandisk and Western Digital later. Through Monday’s close, Sandisk has been the single best performing S&P 500 constituent year-to-date, and the 13th largest points contributor, while Western Digital also ranks highly on both measures.

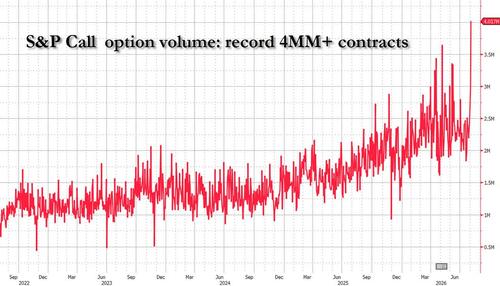

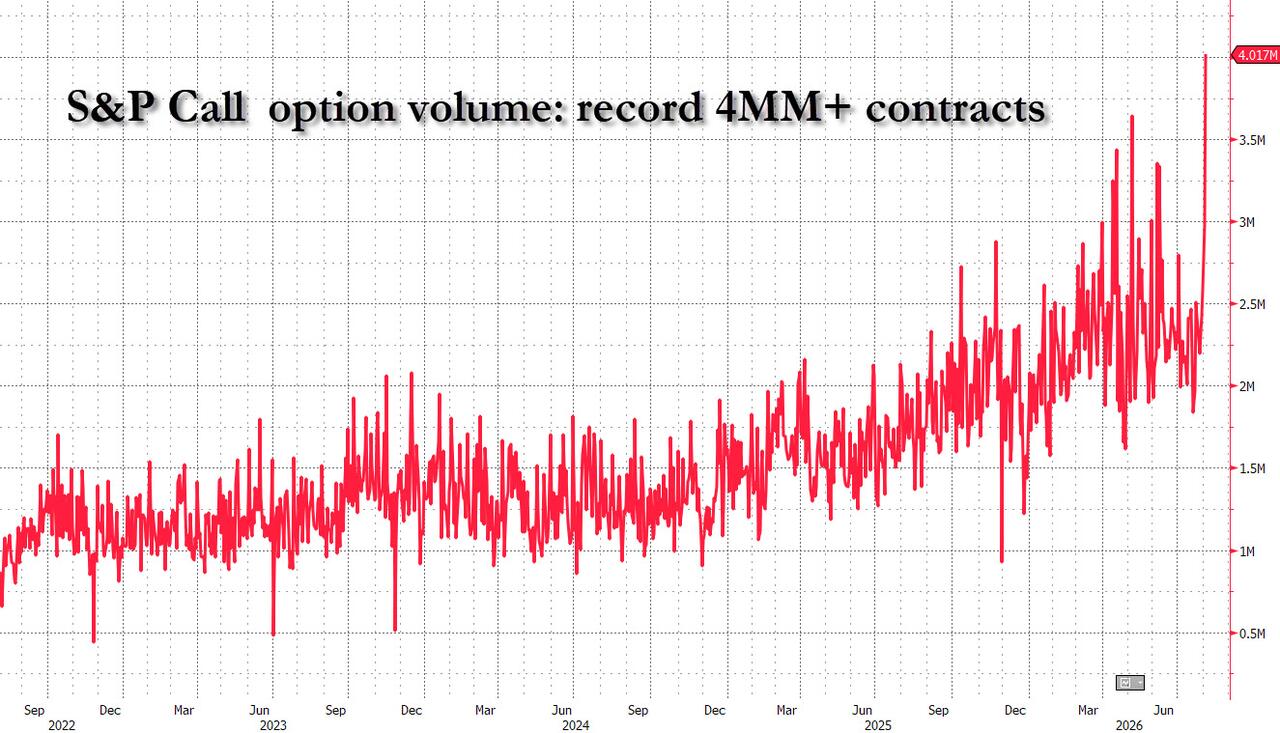

Last month’s heavy deleveraging means that fast-money actors like hedge funds have now covered a lot of their shorts, leaving the setup looking increasingly positive. At the same time, broadening has continued globally and a strong earnings season has accelerated the sector rotation that was already underway. One way to see this week's euphoria: on Tuesday we saw the highest ever amount of S&P call futures bought.

The recent correction in tech stocks has brought valuations to more reasonable levels, helping to restore investor confidence after a bout of volatility triggered losses at several hedge funds last month. The MSCI World Semiconductor Index had tumbled more than 20% from its peak in June, driven by worries around the sustainability of AI spending boom and progress in China’s advanced chipmaking. The gauge has rebounded 15% since then.

“Albeit there was some disappointment on the micro level, the numbers are still confirming that the overarching macro trend is intact as they confirm the durability of the compute build-out,” said Stephan Kemper, chief investment officer at BNP Paribas Wealth Management Germany. “Thus, tech as a whole can benefit even if single players suffer.”

Geopolitical tensions are easing as President Donald Trump said the US had “good” discussions with Iran. Qatar said a proposal has been drafted and both American and Iranian officials sounded hopeful about reopening the Strait of Hormuz. “Sentiment seems to have improved,” though it is likely due to a better risk backdrop than a fundamental change, said Haris Khurshid, chief investment officer at Karobaar Capital. “Lower oil, easing geopolitical tensions and stronger tech sentiment are all helping.”

Brent crude reversed some of Tuesday’s 5.3% plunge after Yemen’s Houthi militant group threatened to escalate attacks on Saudi vessels in the northern Red Sea. Still, the commodity held around $80 a barrel after Axios reported that Washington, Tehran and Oman were nearing an agreement to resume oil flows through the Strait of Hormuz. That’s easing inflation fears and upward pressure on Treasury yields.

“As oil prices come back to the $75-$80 dollar range, markets can focus on fundamentals, which remain robust,” said Mohit Kumar, a strategist at Jefferies International. “Earnings have been solid and there is still a lot of liquidity out there. Positioning is very clean, which sets a nice backdrop for a further rally in risky assets.”

In other assets, Fed’s Schmid suggested higher rates are needed to achieve the Fed’s price stability goals. Bloomberg Economics notes the divergence in global monetary policy outlooks due to energy price volatility, showing “the fog global central banks face as they try to limit the inflationary consequences of the Middle East conflict.” Meanwhile, the cost of hedging against a rise in Treasury yields has surged since last week.

In politics, Trump administration officials are moving toward another temporary extension of a waiver of a century-old shipping law that made it easier to move oil, fuel and fertilizer around the US. The White House has told top US AI companies that open-weight models being developed in China won’t be subject to government testing under the Trump administration’s new AI safety framework. And a potential US ban on Chinese data center components risks straining the countries’ fragile trade truce.

In hedge funds, the losses that forced Situational Awareness to sell stocks at deep discounts appear to be the result of highly concentrated positions in crowded trades, rather than a concerted effort by short-sellers, according to S3 Partners. Whale Rock’s flagship hedge fund had a 21.7% drop in July, erasing about half of its gains for the year.

The upside in oil sapped broader risk sentiment with the Stoxx 600 erasing an earlier advance that took it to a record high.Mining and retail shares leading gains while banks and consumer products stocks are the biggest laggards. Here are the biggest movers Wednesday:

- Sandoz shares gain as much as 8.6%, the most since Feb. 25, after the Swiss maker of generic drugs posted strong sales in the US and at its biosimilars unit

- Glencore rallied as much as 5.4% in London trading, the most since January, after reporting 1H adjusted Ebitda that beat analyst estimates due to surging prices for its key commodities

- Heineken shares gain as much as 3.1% after the Dutch brewer posted a strong set of second-quarter figures, with analysts highlighting outperformance in Asia-Pacific, led by Vietnam

- Nexans shares jumped as much as 7.4% after JPMorgan upgraded the stock to overweight, saying that the French cable manufacturer would be able to achieve its 2028 targets while M&A could bring further upside

- Fresenius jumps as much as 9.3%, the most since October 2022, after the German healthcare group lifted its full-year earnings forecast, following strong second-quarter performances at its hospitals and Kabi drugs business

- Infineon shares drop as much as 5.9% after the chipmaker’s 4Q margin outlook missed estimates, with the firm citing temporary operational and inventory-related effects in the green industrial power segment

- Novo Nordisk shares fall as much as 4.6% in Copenhagen after the Danish drugmaker’s new Wegovy weight-loss pill failed to top analysts’ expectations

- Verisure’s stock slid as much as 7.4% to €9.826 after a shareholder sold a stake for roughly €198.4 million in an overnight placing

- OTP Bank shares drop as much as 1.5% after the Hungarian lender reported total income for the second quarter that missed the average analyst estimate

- Wolters Kluwer shares fall as much as 5.8% after the Dutch information services company reported revenue for the first half-year that met the average analyst estimate

Earlier, Asian stocks rose to the highest in a month, led by a rally in heavyweight chipmakers as sentiment improved following prospects of an interim US-Iran deal. The MSCI Asia Pacific Index gained 2.1%, boosted by TSMC, SK Hynix and Samsung. Tech-heavy markets including Korea, Taiwan and Japan climbed, while Australian shares advanced to an all-time high. A guage of Asian semiconductor stocks rose 4.5%, tracking overnight gains in US peers. SK Hynix got an extra boost amid speculation the Korean firm may soon unveil buybacks and other details of a broader shareholder return plan. Elsewhere, optical stocks in China fell, while those in Japan, India and South Korea rose, after Reuters reported that the US is drafting a ban on imports of some Chinese data center components to protect AI infrastructure.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The kiwi is the weakest of the G-10 currencies, falling 0.5% against the greenback after the New Zealand jobless rate rose more than expected.

In rates, treasuries are steady with front-end lagging rest of the curve slightly, following muted price action during Asia session and London morning. Oil prices erased declines after Yemen’s Houthi militant group’s latest threat against Middle East shipping. US session includes quarterly refunding announcement and July ISM services gauge. Treasury front-end yields are about 1bp cheaper, tracking gains in oil, while rest of US curve is little changed, with bunds and gilts also broadly steady. Treasury’s quarterly refunding announcement at 8:30am New York time is expected to leave in place guidance on steady auction sizes for at least the next several quarters, according to bond dealers. IG dollar issuance slate empty so far. AbbVie’s $10b deal headlined a $17.3b calendar Tuesday. Issuers paid about 5bps in new issue concessions on deals that were 5.2 times covered. Two issuers continue to monitor the market, both with size aspirations exceeding AbbVie’s transaction

In commodities, WTI crude oil futures are up about 0.5% near session highs after erasing declines after Yemen’s Houthi militant group said it would attack Saudi oil tankers in the northern Red Sea. Precious metals jump with spot silver up over 3%.

Today's US economic data calendar includes July ADP employment change (8:15am), July final S&P Global US services PMI (9:45am) and July ISM services index (10am). Fed speakers scheduled include Cook (4:05pm) and Daly (8:35pm)

Market Snapshot

Top Overnight News

- The US, Iran and Oman are preparing to announce a 60-day agreement on shipping through the Strait of Hormuz as soon as today. Donald Trump said talks with Iran are “moving along very nicely.” BBG

- Donald Trump’s administration has paid out about $100bn in tariff refunds since the US Supreme Court struck down its use of emergency powers to levy duties on its trading partners earlier this year. The sum, which is 60 per cent of the $165bn collected from the president’s “liberation day” tariffs, was reported by US customs officials to judges at the US Court of International Trade on Tuesday. FT

- White House is excluding open-models from its framework to test advanced AI capabilities: Axios.

- China’s services activity expanded at its weakest pace in nearly two years, a private survey showed, with businesses turning more cautious about an economy that’s increasingly showing signs of further weakness. BBG

- Shares of SK Hynix Inc. advanced, lifted by an overnight rally in US chipmakers and speculation that the Korean firm may soon unveil buybacks and other details of a broader shareholder return plan. BBG

- China tightened its exports controls on drones to the US and sanctioned multiple American companies in a series of retaliatory measures against Washington’s widening tech curbs. BBG

- UK firms continued to cut jobs in July, extending the labor market slump to its longest since the global financial crisis, a PMI survey showed. Businesses cited cost-cutting and greater use of AI. BBG

- Kansas City Fed President Jeff Schmid said Tuesday that the Federal Reserve’s inflation problem isn’t only about energy, and bringing inflation down to the Fed’s 2% objective will require tighter policy. WSJ

- Progressive Abdul El-Sayed is projected to win Michigan’s Democratic US Senate primary, according to NBC. He’ll face Republican Mike Rogers in November in a contest critical to Democrats’ hopes of regaining the Senate. BBG

- OpenAI and Anthropic AI models carried out “potentially harmful” actions, including hacking a website, UK government safety tests found. Separately, the White House was said to have told US AI firms that open-weight models developed by their Chinese rivals won’t be subject to government testing. BBG

- V-Shaped: Nasdaq now up ~945 bps in just 4 sessions (since last Thursday), punching back above its 50-dma to the upside. This 4-day move stacks up with how Tech has traded out of (or during) other notable market “events” over the last 20 years (GFC, COVID, ’22 Hiking Cyle, Liberation Day, et al).: Goldman

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher as the region took its cue from the rally on Wall Street, where the S&P 500 and Dow printed fresh record highs, although the Nasdaq was the outperformer on tech strength, while yields and oil prices declined amid hopes of a Hormuz deal. ASX 200 traded in the green, with the upside led by outperformance in miners, materials and tech, which picked up the slack from the weakness in energy, utilities and the top-weighted financial sector. Nikkei 225 rallied back above the 66,000 level amid the tech strength, with SoftBank shares among the biggest gainers, and are up by a double-digit percentage owing to its heavy AI exposure. KOSPI rallied amid the tech momentum and with earnings results also providing tailwinds for stocks. Hang Seng and Shanghai Comp were mixed, with the Hong Kong benchmark flat amid weakness in the energy sector, while the mainland conformed to the upbeat mood despite disappointing RatingDog Services PMI data, although Chinese optical stocks were pressured as the US mulls an import ban.

Top Asian News

- US Treasury Secretary Bessent said the uptick in Japan's inflation was the result of weak yen and energy prices, as energy prices come down and we no longer have excess yen weakness, will contribute to inflation coming down.

- Japanese Finance Minister Katayama said they will not rely on new debt issuance to fill tax revenue shortages, will review budget spending and revenue to fill tax revenue shortages.

European bourses continue to climb, with gains broadly seen across the board. Focus will be on the potential announcement of the reopening of the Strait of Hormuz. On the data front, EZ and UK final PMIs printed a tick higher. For the EZ figure, S&P highlighted that the rise in the headline output index indicates quarterly GDP growth of 0.3%. For the ECB, S&P Global stated that, with the renewed flare-ups in the Middle East leading to upside risks to inflation, it should put policymakers in a more hawkish stance. However, with the PMI price gauges dropping markedly, it may provide a window for a delay of further hikes. Sectors point to a positive bias. Basic Resources top the sector pile, with Retail and Utilities rounding out the sector outperformers. To the downside is Consumer Products & Services, with Banks and Real Estate completing the bottom 3 laggards.

Top European News

- Italian Economy Minister Giorgetti said they will be asking the EU to increase energy spending by 0.6% and defence spending by 0.9% of GDP. The minister added that they will be presenting to parliament a formal request to increase the deficit between September and October, following on from EU talks.

FX

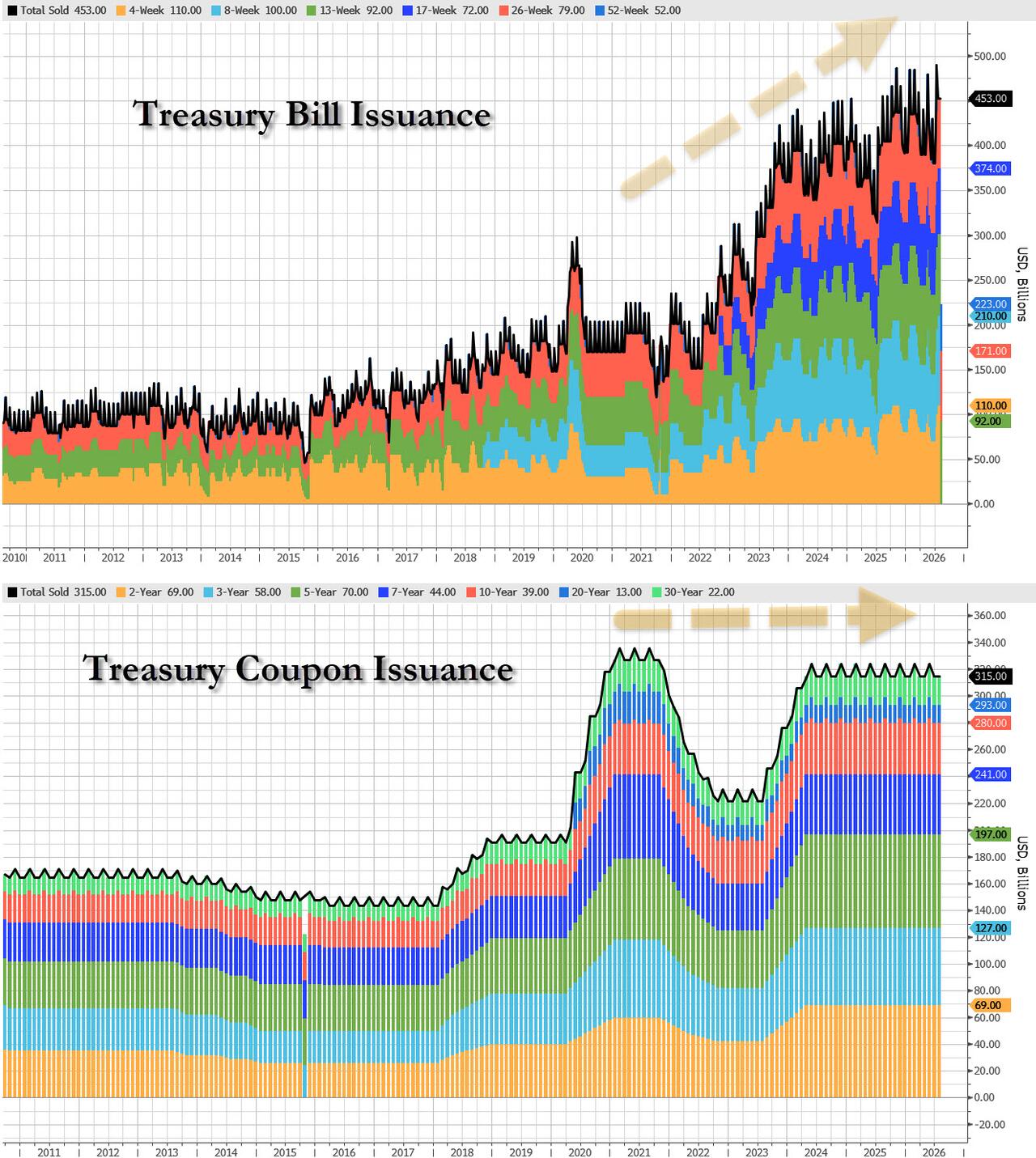

- USD lacks direction with DXY just below 100.00 as the positive risk environment is weighed against a bounce in energy benchmarks; Brent +USD 1/bbl. Several scheduled releases today, including ISM services and ADP jobs ahead of Friday's NFP, while the Treasury is slated to release its QRA; focus is on whether guidance retains language that coupon and FRN auction sizes will hold “for at least the next several quarters.” Further on that, JPM flags a USD 3.7tln four-year funding gap, and argues the wording should be tightened, but expects the Treasury to hold fire ahead of November’s midterms to avoid unsettling long-end rates. On the speaker slate, Fed's Cook is set to speak.

- GBP is the marginal outperformer despite a Times article overnight suggesting the government would look to exploit a Reeves-era fiscal rules loophole to increase government borrowing by as much as GBP 9bln. Perhaps a factor soothing markets is how both Burnham and Healey have previously expressed willingness to utilise flexibility in the fiscal rules. Elsewhere, UK Final PMIs were confirmed in expansion though revised modestly lower. GBP/USD trades within a narrow 1.3340-1.3470 range, with all significant DMAs between 1.3350 and 1.3400, likely to provide support; 1.3500 will likely prove resistance.

- EUR conforms to price action across the G10 space and is essentially unchanged against the Buck in quiet trade. ING today notes how the heatwave, impacting water levels and nuclear power, means the single currency has been unable to capitalise on the stronger-than-expected data over the past week. Today, EZ PMIs, like those seen across the channel, did not deviate enough from prelim figures to spark a EUR reaction. EUR/USD flat with 50 and 100 DMAs either side at 1.1476 and 1.1570, respectively.

- NZD is the clear underperformer after the unemployment rate firmed at a faster rate than was expected. Kiwi was pressured immediately after the data and continued lower throughout the morning, surpassing recent 0.5860 support and potentially on track to test 0.5850.

Fixed Income

- A firmer start for the space, led higher by the initial downside in energy given the overnight geopolitical updates and the potential for a Hormuz deal to arise in the next 24hrs or so. Albeit, reporting this morning has been somewhat less constructive, and as such crude has reverted back into the green, and fixed has waned from best.

- Gilts briefly eclipsed 88.00 by six ticks and with gains of 44 at best. Upside a function of the initial energy pressure, catch-up to the overnight moves in fixed and on domestic fiscal reporting. On the latter, The Times scooped that Ministers are looking at utilising a Reeves-era adjustment to the fiscal rules, when the former Chancellor made it so the government can count spending on equity/infrastructure as assets, which can then be offset against borrowing costs. Such an approach could allow GBP 9bln/yr to be raised, without PM Burnham or Chancellor Healey having to adjust the rules themselves.

- Bunds also bid, but off best. Peaked at 125.51 in APAC trade, firmer by near 50 ticks at the time, but has since essentially halved that as energy moves. For Germany, specifics have been and are scheduled to be relatively light aside from Green supply due shortly. Elsewhere, from the bloc, EZ June PPI was cooler-than-expected M/M but in-line Y/Y; no move to the series.

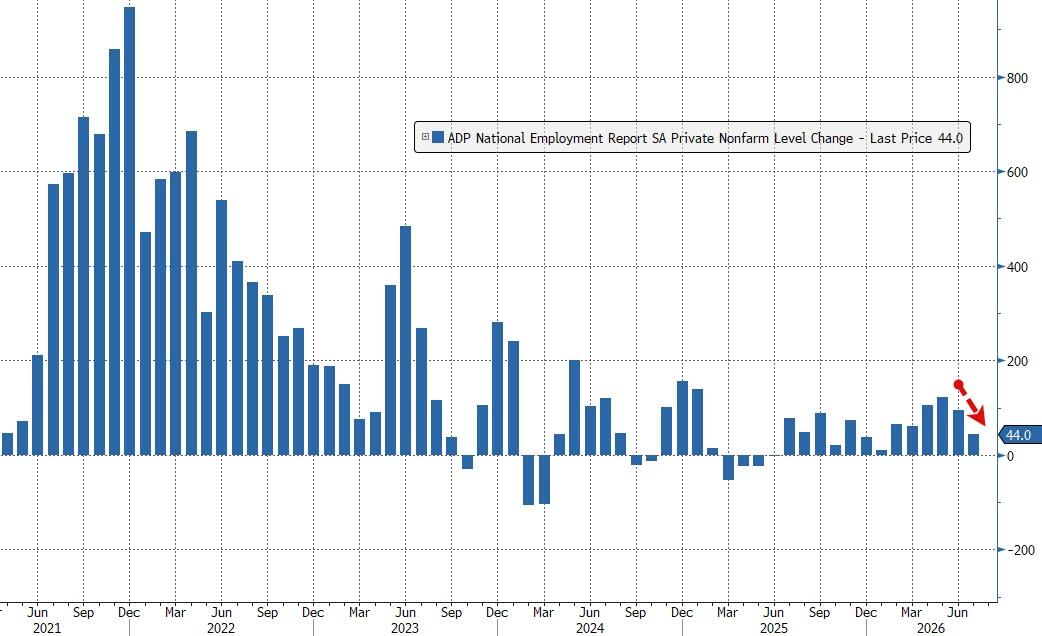

- USTs in-fitting, modestly firmer in narrow 108-26 to 109-01 confines. A busy docket ahead, in addition to potential geopolitical updates. Firstly, ADP prints before Friday’s NFP, seen at 70k (prev. 98k), vs 91k (prev. 57k) for the BLS series. Thereafter, the Chicago indicator hits alongside the Quarterly Refunding Announcement, focus is on the language around coupon and FRN sizes. Next up, we have the US Final PMI and ISM Services read for July, before potential commentary from Fed’s Cook (voter).

Commodities

- In terms of Middle Eastern geopolitics, developments suggest momentum towards a diplomatic agreement to reopen the Strait of Hormuz, although negotiations remain ongoing. US President Trump said in a Fox News interview that the Strait could reopen very soon, describing discussions with Iran as productive after an all-day round of negotiations and stating there is still ample time to reach a deal, while warning that Iran would face severe consequences if it withdrew from talks again. He later added that negotiations were progressing well and that more clarity would emerge within 48 hours.

- Regarding to the potential Hormuz agreement, Axios reported that the US is targeting a Wednesday announcement of a Hormuz agreement under which inbound vessels would transit through a northern lane in Iranian waters and outbound vessels through a southern lane in Omani waters, with no transit fees during an initial 60-day period and joint efforts to clear naval mines from the median lane within 30 days before negotiating a permanent arrangement between Oman and Iran.

- Energy futures have tilted higher during the European morning following a subdued APAC session, with gains seen after the Yemeni Houthis announced that they have targeted a Saudi tanker in the North of the Red Sea. This essentially amounts to an expansion of the Houthi blockade that threatens to completely choke off Saudi Arabia's alternative energy export routes. Prices thereafter saw modest downticks on reports that the Pakistan PM Sharif and Army Chief Munir will visit Saudi Arabia tomorrow. Meanwhile, upticks were seen once again following reports that Israeli strikes were reported in Southern Lebanon, which is seen as a headwind for US-Iran negotiations. WTI Sep’26 resides towards the top end of a USD 74.24-76.47/bbl range (vs yesterday’s USD 75.11-82.33/bbl range) while Brent Oct’26 trades in a USD 78.11-80.80/bbl range (vs yesterday’s 78.67-86.33/bbl parameter). Dutch TTF is softer intraday but in choppy trade, printing on either side of the EUR 55/MWh mark in a current ~EUR 54.50-55.75/MWh range.

- Metals are firmer as DXY price action is once again somewhat contained despite the volatility across energy. Spot gold trades towards the top end of a USD 4,065-4,180/oz range after topping the 22nd July high (USD 4,166/oz) to match the 7th July peak (USD 4,180/oz). Spot silver has mounted USD 60/oz once again to trade towards the upper end of a USD 59.40-61.90/oz range at the time of writing.

- Base metals also cheer the relatively stable dollar against the backdrop of energy volatility. 3M LME copper holds above USD 14k/t in a USD 13,974.45- 14,104.00/t range at the time of writing.

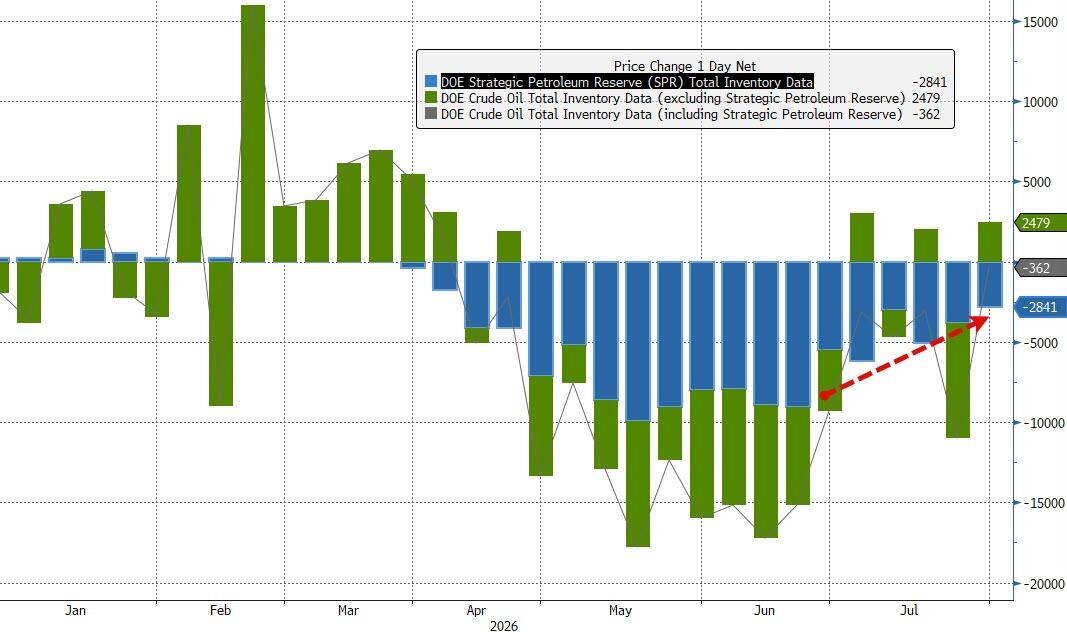

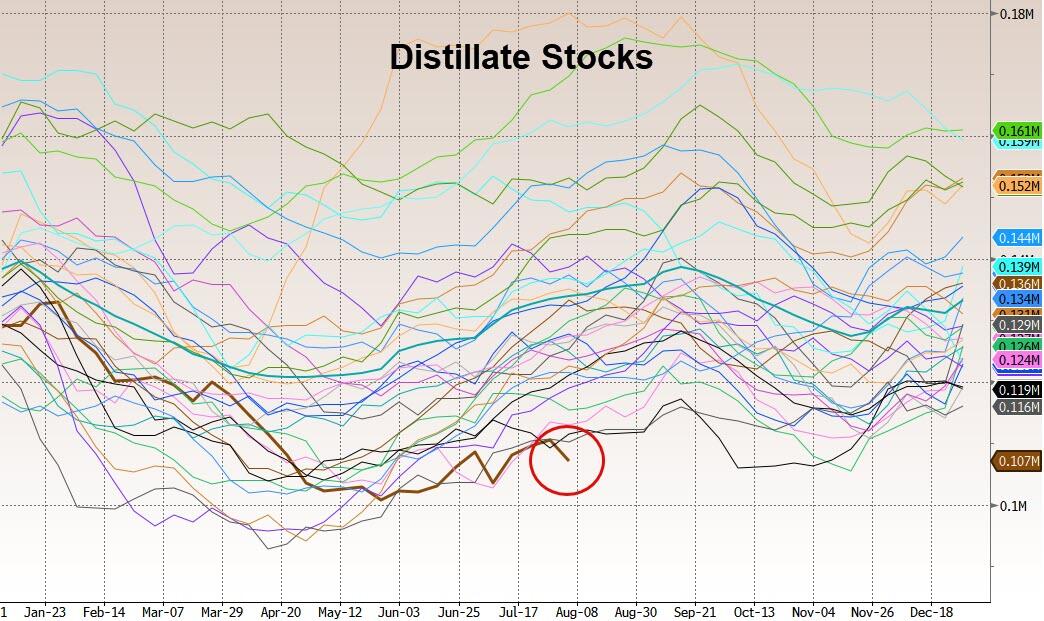

- US Private Inventory Data (bbls): Crude +2.7mln (exp. -2.0mln), Distillates -1.2mln (exp. -0.1mln), Gasoline +0.2mln (exp. -1.3mln), Cushing +2.4mln.

- US Energy Secretary Wright said the extension of Jones act waiver is likely and has resulted in lower energy prices in California and the US East Coast.

- Ferrexpo (FXPO LN) said they have decided to temporarily suspend production of iron ore products from its mining and pelletising operations in Ukraine and are currently able to supply its European customers from existing inventory stockpiles.

Trade/Tariffs

- US President Trump's administration is considering blocking Chinese imports of optical transceivers from China.

- China's MOFCOM said it will impose countermeasures on six US entities and will take countermeasures against US compliance-testing firms.

- Chinese embassy in the US said Washington should stop threatening Chinese companies and slammed the Trump administration's plan to ban certain electronic equipment used in data centres.

Central banks

- Fed's Schmid (2028 voter) said tight monetary policies are needed to get inflation back to the 2% target, and that inflation is currently too high and is worrisome. The current stance of Fed policy is not restrictive and the recent relief on energy prices may prove temporary. Schmid added that the economy is performing well overall and growth is resilient, while welcoming the recent inflation data. However, it is too soon to say if it is easing. He ended by stating that the job market appears to be roughly in balance, and AI investment is driving up inflation, which the Fed should not ignore.

- RBI keeps Repurchase Rate unchanged at 5.25%, as expected, via unanimous decision, while policy stance is kept at neutral. Growth continues to be supported by domestic demand, while there is a need for greater clarity on inflation before taking policy action. Sees FY27 real GDP growth of 6.7% (prev. 6.6%) and FY27 CPI at 5.0% (prev. 5.1%).

- BoJ Minutes from the June Meeting stated most members share the view economy is moving in line with the baseline scenario, and there were risks underlying inflation may overshoot the BoJ's 2% target. Members agreed it was appropriate for the BoJ to continue raising rates. Few members said the BoJ must maintain guidance that the BoJ will keep rising rates if the economy and prices move in line with its forecasts.

Geopolitics: Middle East

- An Iranian source familiar with the direct Iran-Oman talks has told CBS News the discussions between Tehran and Muscat are now focused largely on the mechanics of reopening the Strait of Hormuz and that broad outlines have largely been agreed. Under the current proposal, ships entering the Strait would use the channel closest to Iran, with Iran coordinating inbound traffic, while vessels leaving the strait would use the Omani side, with Muscat managing outbound traffic. The proposal also includes a "service fee," with the revenue split between Iran and Oman. According to the source, the broad outlines have largely been agreed upon, with the remaining discussions focused on implementation and timing. Axios reported something similar, in which the US is nearing a Hormuz deal. Axios added that no tolls or fees would be charged during the 60-day period and the parties would work on clearing naval mines from the median lane of the strait within 30 days.

- US President Trump said in a Fox News interview that the Strait is going to be open very soon and that they are having very good discussions with Iran, while he warned if Iran backs out again, they'll be hit very hard. Trump also commented that they had a very good day with Iran and had an all-day negotiation today, while he also said they have plenty of time to reach an agreement with Iran. Furthermore, Trump separately commented that they are moving along very nicely regarding Iran and we will know in 48 hours on Iran.

- US Central Command said that the southern route through the Strait of Hormuz remains free and open for all commercial vessels seeking to transit the international waterway.

- Israeli media citing unnamed Israeli sources reported that US President Trump and his advisers are seeking a deal with Iran at any cost, according to Al Jazeera.

- Israel, Lebanon and the US are discussing which country or countries will be responsible for verifying Hezbollah's removal from pilot zones, with Italy being one of the options, according to three sources familiar with the talks cited by i24's Stein.

- Israeli strikes reported in Southern Lebanon, Tasnim reported.

- Pakistani sources said Pakistan PM Sharif and Army Chief Munir will visit Saudi Arabia tomorrow, Al Hadath reported.

- Yemeni Houthis said they attacked a vessel in the Red Sea, with the spokesman adding they attacked a Saudi oil tanker off the Yanbu with missiles.

- Saudi Arabia reportedly attacked Yemen's capital of Sanaa with explosions heard, according to Fars News Agency.

- Saudi official said no talks are taking place between the Saudis and the Houthis via mediators, according to Al Arabiya.

Geopolitics: Ukraine

- Air attack reported on Ukraine's capital, Kyiv, with explosions heard amid reports of a ballistic missile attack.

Geopolitics: Other

- North Korea leader Kim's sister criticised Japan's recent test firing of a Tomahawk missile and said they will be forced to add more military options in response to Japan's strengthening of defence capabilities.

- US Pentagon is drafting a new US nuclear strategy in case of regional war with China or Russia, NBC sources report.

US Event Calendar

- 7:00 am: Jul 31 MBA Mortgage Applications, prior -6.4%

- 8:15 am: Jul ADP Employment Change, est. 65k, prior 98k

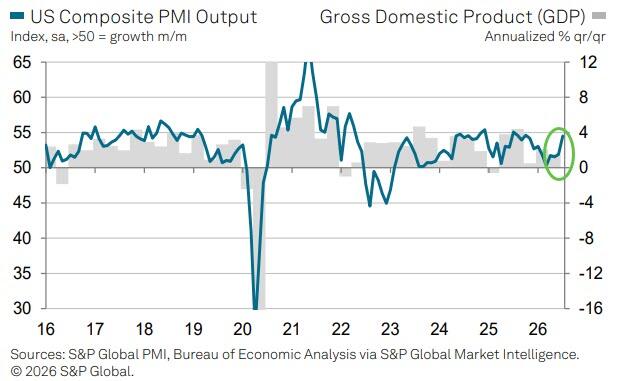

- 9:45 am: Jul F S&P Global US Services PMI, est. 53.6, prior 53.6

- 9:45 am: Jul F S&P Global US Composite PMI, prior 53.6

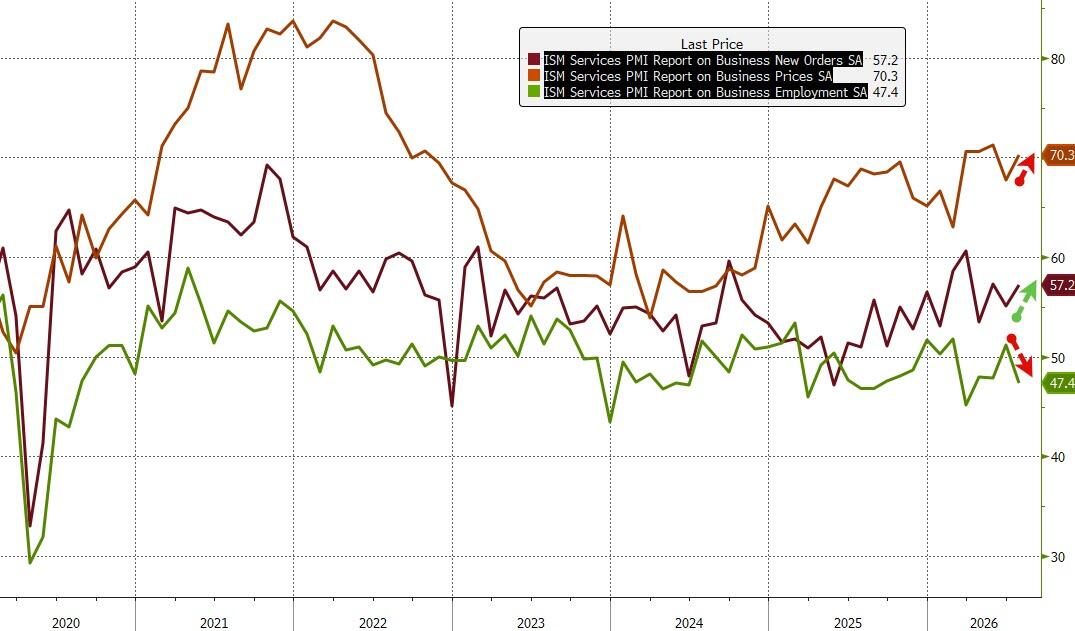

- 10:00 am: Jul ISM Services Index, est. 54.5, prior 54

DB's Jim Reid concludes the overnight wrap

As recently as last Friday, investors were debating whether a renewed Middle East energy shock would be the soundtrack of the late summer. By yesterday's close, Brent crude had fallen back below $80/bbl, short-term inflation expectations had moved to multi-month lows, bond yields had continued to retreat, and the S&P 500 (+1.79%) and the Stoxx 600 (+0.73%) had moved to fresh record highs. At the same time, the AI trade continued to regain momentum, with semiconductors enjoying another strong session and investors increasingly willing to lean back into the capex theme that looked under pressure during July's volatility. These themes have held up overnight, with oil and Treasury yields edging lower, while Asian equities are rallying.

The latest catalyst was another day of encouraging headlines around the Strait of Hormuz. Qatar said that a draft proposal had been circulated between the parties, whilst Treasury Secretary Bessent suggested that an agreement to reopen shipping flows could be reached “today or tomorrow”. Axios then reported last night that the US is hoping for a Wednesday announcement of an interim deal that would see a temporary 60-day arrangement between Iran and Oman under which Gulf-bound vessels would pass through Iranian waters, whilst vessels leaving the Gulf would be able to travel through Omani waters with no fees being charged during the 60-day period. Similar details were reported earlier by the Wall Street Journal, though both reports leave unclear whether a long-term arrangement between Iran and Oman might then involve charging a toll for using the Strait. And as I write this around 5am LDN time, Trump just told reporters that talks were “moving along very nicely” and “we’ll know in 48 hours”, though he also told Fox News earlier that “they're going to get hit very hard” unless the Strait is open “very soon”.

Markets have seen plenty of false dawns throughout this conflict, so plenty of attention will be on whether a deal is announced imminently and its details. As of now, investors are increasingly pricing a solution, with the most obvious positive reaction coming in energy markets. Brent crude fell another -5.26% to $79.36/bbl yesterday, whilst WTI declined -5.69% to $75.77/bbl. European natural gas futures also fell -2.75% to their lowest level in almost three weeks. Brent is another -0.66% lower this morning. The speed of the reversal has been impressive with Brent now down by more than -10% since Friday.

The associated move in inflation pricing was arguably even more noteworthy. The US 1yr inflation swap fell another -6.4bps to 1.80%, its lowest since 2024, whilst the Eurozone equivalent declined -9.5bps to 2.27%. US 5yr inflation swaps fell -4.8bps to 2.36%. Markets are clearly dismantling a sizeable portion of the near-term inflation premium that had built up as the conflict intensified through July.

Government bonds also continued to benefit. The 10yr Treasury yield fell -6.3bps to 4.61%, and while breakevens led the decline, real yields moved lower too, with the 30yr real yield falling -3.8bps to 2.97%. The Treasury curve is a touch lower again overnight, with 10yr yields down -0.8bps overnight, even as Kansas City Fed President Schmid struck a hawkish tone yesterday evening, saying that “bringing inflation down to the Fed’s 2% objective will require tighter policy”.

In Europe, bund yields declined -4.5bps to 3.11%, while gilts rallied a further -5.7bps to 4.90%, extending the strong performance seen since oil began reversing lower at the start of the week. Peripheral debt also performed strongly, with 10yr BTP yields falling -7.1bps to 3.86%, with a -15.8bps decline so far this week marking their best two-day run since May.

Importantly however, the bond rally wasn’t fueled by weaker growth. The JOLTS survey for June did show job openings easing to 7.36 million from 7.54 million previously, but most of the survey’s details remained constructive, with hiring picking up, layoffs staying subdued, the quits rate stable at an upwardly revised 2.0% (vs 1.9% expected) and the ratio of vacancies to unemployed workers little changed at 1.04 (vs. 1.03 prev.). In addition to this steady labour market signal, June durable goods orders were revised up to +0.5% mom (+0.3% exp.) with core capital goods orders rising +1.2% (+0.9% exp).

That combination of lower oil prices, falling inflation expectations and still-resilient US data proved an ideal backdrop for risk assets. The S&P 500 rose +1.79%, closing at an all-time high for the first time in two months. Tech stocks outperformed, with the Nasdaq up +2.59%, though the Mag-7 (+0.73%) underperformed. The AI complex was even stronger, with the Philadelphia Semiconductor Index surging +6.55%, its strongest daily gain since March and extending its rise since last Wednesday to +16.58%, its biggest 4-day advance since 2020.

So the rebound in semiconductors continues to gather pace. After enduring a correction of more than -20% during July, investors appear increasingly willing to re-engage with the AI trade. Helping sentiment were Palantir's (+29.45%) strong outlook, reports of Anthropic agreeing a $10bn computing infrastructure deal to meet demand for its models, and Caterpillar (+5.60%) raising sales guidance whilst pushing back on concerns that data-centre demand is slowing. Together, that helped rebuild investor confidence in the broader AI capex cycle after July's turbulence.

Another interesting AI-related development came from the networking space. Reuters reported that the Federal Communications Commission is drafting a ban on imports of new Chinese optical transceivers, critical components that allow information to travel through fibre-optic cables inside data centres. The news boosted US optical-networking names, with Marvell Technology up +12.81% and Coherent gaining +12.35%, as investors anticipated a shift in demand towards domestic suppliers. While a niche story on the surface, it is another reminder of how AI supply chains are part of broader strategic competition between the US and China.

A bit of shine came off the tech performance overnight following results from SpaceX and AMD. SpaceX fell by over -7% after-hours after reporting higher AI capex spending, though that decline was smaller than the +9.43% jump in yesterday’s regular session. AMD shares also slid in extended trading as the chipmaker’s Q3 revenue guidance ($13bn vs $12.5bn) came in slightly ahead of consensus but below the more optimistic estimates. This leaves NASDAQ futures (+0.11%) underperforming those on the S&P 500 (+0.32%), but the overall equity mood remains positive overnight.

Optimism is also visible in Asian markets this morning. Across the region, the KOSPI (+4.32%) and the Nikkei (+3.32%) are leading gains. Mainland Chinese stocks are moving higher with the Shanghai Composite (+1.34%) outperforming the CSI 300 (+0.99%), while the Hang Seng (+0.11%) is little changed. The China market performance hasn’t been helped by the RatingDog Services PMI for July, which fell from 54.1 to 50.4 (vs 53.7 expected). That’s its lowest level since September 2024, pointing to still soft domestic demand in China. Meanwhile, the S&P/ASX 200 (+0.71%) is on course to eclipse its record high reached back on March 2, helped by a strong June household spending print (+0.8% MoM vs +0.2% expected).

Elsewhere, European equity indices continued to push into record territory yesterday. The Stoxx 600 (+0.73%), DAX (+0.77%), CAC (+0.61%) and FTSE MIB (+1.26%) all reached new all-time highs, while the FTSE 100 (+0.20%) is just 0.3% below its own historic peak. So beyond the US, investors are increasingly embracing the combination of lower oil prices and easing inflation concerns.

Another market theme worth watching remains the yen. During his CNBC interview yesterday, Bessent said that the US would do "whatever it takes" to support Japan and argued that excessive yen weakness risked broader instability across Asia. He also said that it would be reasonable for the Fed to upsize the FIMA repo facility, a point that our rates strategists have sympathy with (see their take here). In his extensive comments, Bessent also said he believed the BoJ Governor “will do what is needed”. Note that our FX strategists see faster BoJ hikes as necessary for a more sustained recovery in the yen. Following Bessent’s remarks, the yen rallied from intraday lows, though it still finished yesterday’s session -0.36% lower at ¥157.75 per dollar. However, that’s significantly stronger than the roughly ¥163 level seen before last week's intervention efforts. The yen is little changed against the U.S. dollar this morning.

This morning’s minutes from the BoJ’s June policy meeting revealed that several board members expect consumer inflation to receive a notable boost in the second half of the current fiscal year and showed that two of the eight board members advocated for a faster pace of interest rate hikes. The latest Japan wage data this morning is likely to maintain the pressure for BoJ hikes, showing nominal wage growth at +3.4% yoy in June (in line with expectations after a revised +3.3% rise in May), marking the fifth consecutive month of gains above 3% and the longest such streak in 34 years. A more stable wage indicator, which excludes bonuses, overtime payments, and sampling distortions, rose +2.9% for full-time employees (vs +2.7% expected). Real wages increased +1.6%, extending gains to a sixth consecutive month, the longest run since 2021.

To the day ahead now, data releases include the US July ADP report, where our US economists expect employment growth of +60k after +98k previously. We will also get ISM services, UK July new car registrations, France June industrial production, Italy July services PMI, Eurozone June PPI. Tomorrow, the Fed’s Cook will also speak. Earnings include Eli Lilly, Walt Disney, CVS Health, eBay, Block, and Global Payments.

Tyler Durden

Wed, 08/05/2026 - 08:20

Crash Override gets his ass handed to him by Acid Burn (Hackers)

Crash Override gets his ass handed to him by Acid Burn (Hackers)

Michigan Democratic Senate candidate Abdul El-Sayed speaks at a rally in Canton, Mich., on July 29, 2026. Jacob Burg/The Epoch Times

Michigan Democratic Senate candidate Abdul El-Sayed speaks at a rally in Canton, Mich., on July 29, 2026. Jacob Burg/The Epoch Times

Recent comments