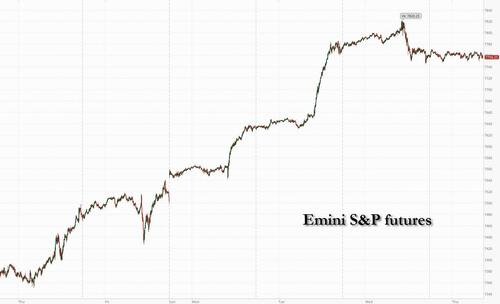

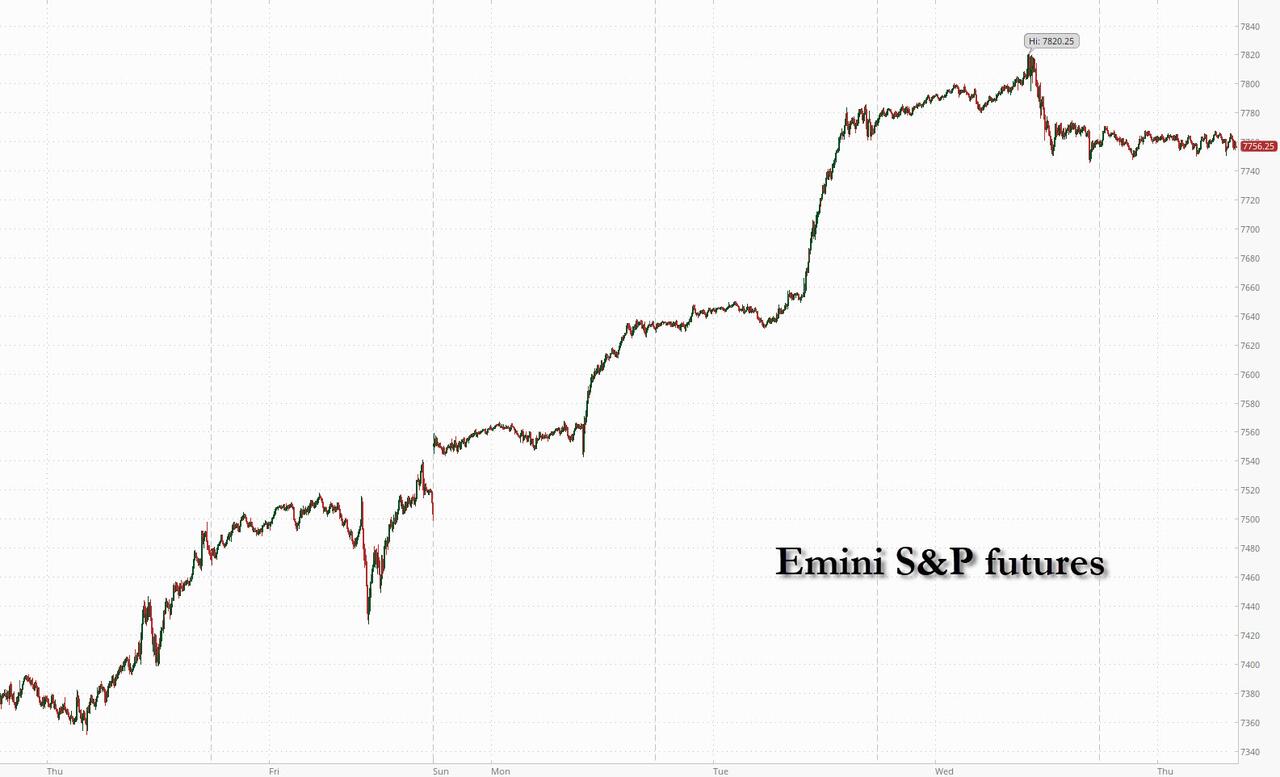

Futures Flat As Tech Slides After Memory Stocks, Korea Tumble

US futures are mixed with S&P futures modestly higher offset by a slide in tech: as of 8:00am ET, S&P futures are up 0.1% while Nasdaq futures drop 0.5%, hit by a plunge in Sandisk (down 9% in pre-market), and rival Western Digital which tumbled 15%, after both companies reported earnings. AppLovin also slumped 16% after missing revenue estimates while DataDog tumbled as much as 18% after guidance wasn't strong enough, and pushed Nasdaq to session lows. Mag 7 stocks are mixed (AAPL +1.0% and GOOGL +0.7% are among the outperformers). Asian stocks declined, led by losses in heavyweight chipmakers following earnings reports from US peers that renewed concerns over the stretched rally in memory-related shares. European shares were more resilient and advanced for a 4th day on hopes of an Iran deal (that was supposed to happen two days ago) as strong earnings boosted sentiment, with WPP Plc leading gains in the media sector. Bond yields are 1-2bp higher. Commodity prices were mostly higher: base metals are all higher this morning; gold +0.6%, while silver -0.4%. Overnight, not many incremental updates on US/Iran, with investors waiting for the details of the Iran/Oman deal around the Strait of Hormuz.

In premarket trading, Mag 7 stocks are mostly higher, offseting a plunge in chip/memory names (Apple +1.1%, Amazon +0.7%, Meta +0.5%, Alphabet +0.5%, Nvidia +0.6%, Tesla unchanged, Microsoft -0.6%)

- Albemarle (ALB) gains 3% after the chemicals company reported second-quarter adjusted earnings per share that beat the average analyst estimate on strong lithium prices.

- AppLovin (APP) drops 19% after the mobile-app marketing company reported revenue for the second quarter that was slightly below the average analyst estimate. The company’s forecast for adjusted Ebitda and adjusted Ebitda margin also came in below consensus expectations.

- Celsius (CELH) drops 17% after the energy drink maker’s adjusted EPS and revenue fell well short of Street expectations.

- Constellation Energy (CEG) rises 4% after the nuclear power plant operator boosted its adjusted operating earnings per share forecast for the full year.

- Datadog (DDOG) slumps 17% after the software company posted an adjusted gross margin for the second quarter that trailed the average analyst estimate.

- Duolingo (DUOL) falls 8% after the language-learning software company gave a revenue and bookings forecast for the third quarter that fell short of expectations.

- Figma (FIG) falls 15% after the creative software platform gave revenue guidance for the third quarter that disappointed Wall Street. The firm also posted a second-quarter operating margin that dropped from the first quarter.

- Fiserv (FISV) falls 9% after the fintech slashed its full-year profit outlook and posted quarterly earnings that fell short of analyst estimates as revenue slumped.

- Honeywell Aerospace (HONA) declines 14% after the aerospace and defense company reduced its outlook for the full year to reflect supply chain issues.

- HubSpot (HUBS) is down 23% after the maker of customer-relationship management software forecast revenue for the current quarter that fell short of the average analyst estimate.

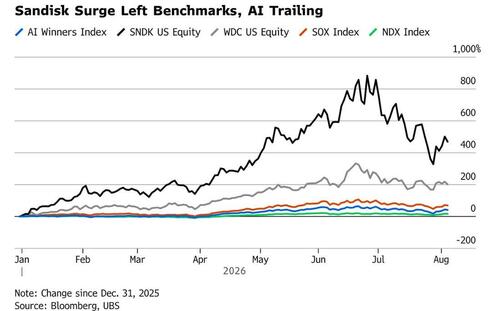

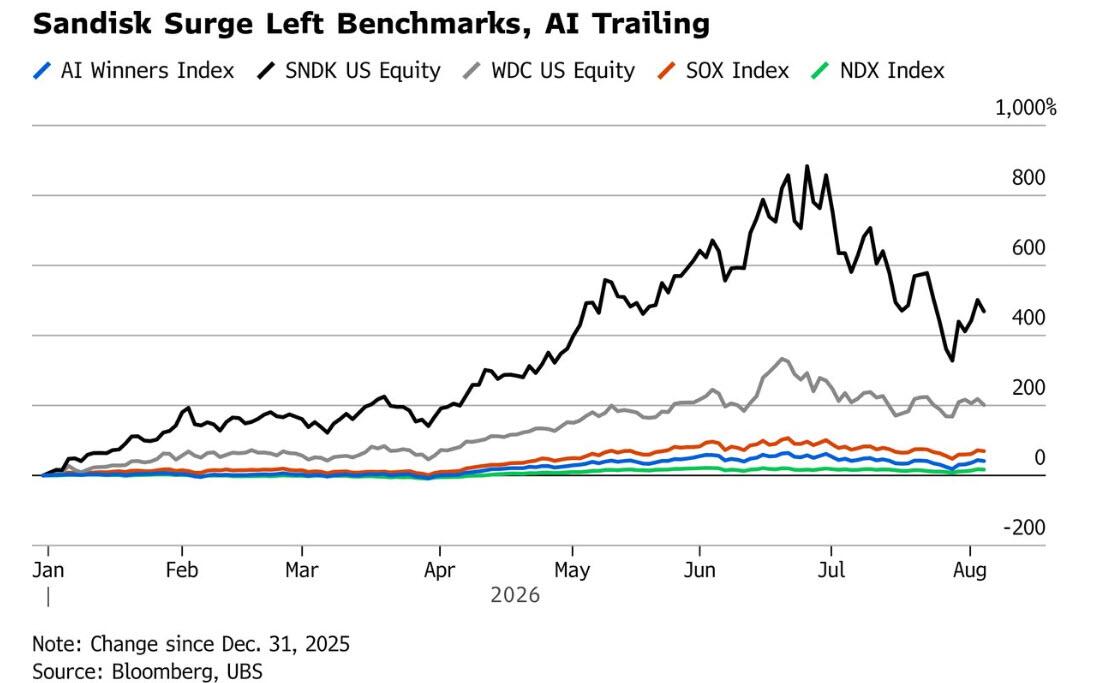

- Sandisk (SNDK) is down 9% after the computer hardware company’s revenue forecast for the first quarter missed the average analyst estimate.

- Six Flags Entertainment (FUN) falls 3% after the amusement-park operator reported net revenue for the second quarter that missed the average analyst estimate.

- SoundHound AI (SOUN) jumps 26% after the software company reported better-than-expected second-quarter revenue.

- Sunrun (RUN) drops 12% after the home solar company cut its guidance for full-year cash generation, citing factors including reduced volumes from affiliate channels.

- Warby Parker (WRBY) falls 4% after the eyeglass company’s second quarter sales trailed the consensus estimate.

- Western Digital (WDC) falls 16% after the computer hardware and storage company forecast revenue for the first quarter that missed the average analyst estimate at the midpoint. Analysts note the company’s performance lags that of peer Seagate.

- Zillow Group Inc. (Z) is down 11% after the online real estate platform provided revenue forecast for the third quarter that missed the average analyst estimate.

In other AI news, DeepSeek plans to implement a significant price increase across its AI services, an unusual shift from the disruptive Chinese player. OpenAI said the AI models behind the Hugging Face hack began working together to break out of their testing environment as early as May. And Meta Platforms said one of its AI models accessed the internet and hacked into an outside service’s systems during cybersecurity testing. In other corporate news, CME and FanDuel are scaling back a joint effort to take on prediction market startups. MercadoLibre shares are sliding in premarket trading as worries about the e-commerce giant’s spending plans are outweighing an estimate-beating quarter.

After big gains to start the week, stocks may be stuck in a holding pattern until Friday’s payrolls, while recent economic policy decisions are also causing some nervousness about US assets. AI concerns related to elevated capex, ROI and circular financing had dissipated in recent trading sessions, but seem to be back in focus; this is now a weekly thing with Risk On/Risk Off becoming AI Math on/AI Math off. SoftBank results showed a big investment gain on its Intel shares but muted gains in the value of its OpenAI investment and declines inside the Vision Fund portfolio. Microsoft is also making headlines, with disclosures showing it generates most of its AI revenue from OpenAI.

Sandisk and Western Digital both gave tepid revenue forecasts for next quarter, renewing concerns over the stretched rally in memory-related shares. The pair have been big contributors to S&P 500 gains this year, as we noted yesterday; both are sharply lower this morning, and this is a reminder how Wall Street analysts are zero signal and all noise: "Sandisk Corp PT Cut to $1,750 from $3,000 at Jefferies."

The semiconductor sector was also the focus in Asia as Korea’s Kospi Index fell 4.8% with SK Hynix Inc. and Samsung Electronics Co. leading losses. “Investors are increasingly asking what incremental catalysts are needed to remain in the Asia memory trade,” said Gary Tan, a portfolio manager at Allspring Global Investments.

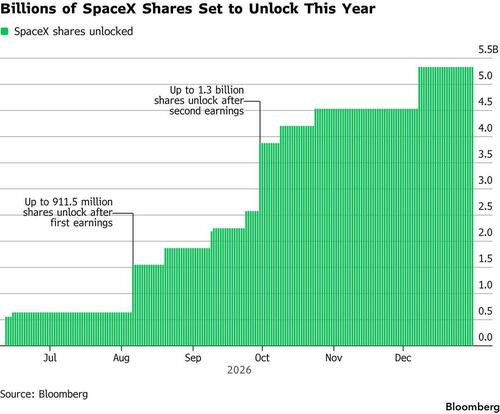

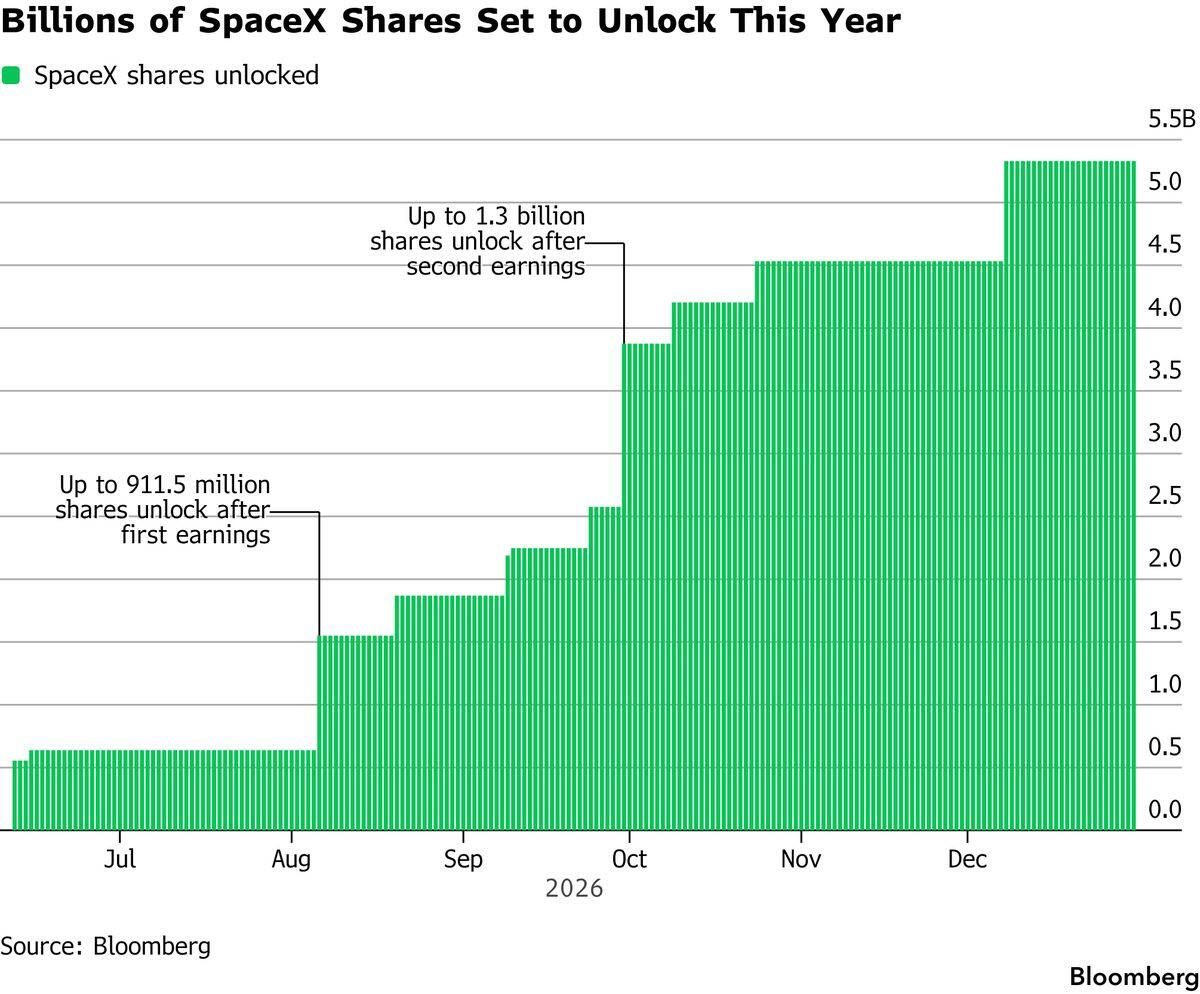

SpaceX, meanwhile, may be in for another volatile day as $101 billion worth of stock becomes available for trading. It’s the first lock-up expiry of a staggered nine-stage structure, designed in an effort to dilute the impact of the vast amount of shares locked up. SPCX shares edged higher in premarket trading after the company’s first quarterly earnings report since its listing triggered a 14% slide.

The pause in the tech-led rally comes as investors reassess valuations after AI-related shares rebounded from last month’s selloff. Traders are also focused on Friday’s US non-farm payrolls data, which is expected to show a strengthening jobs market, as they look for clues to the Federal Reserve’s policy path.

Meanwhile, Brent crude held at around $80 per barrel after Iran said it reached an agreement with Oman on a proposed shipping route through the Strait of Hormuz, raising the prospect of energy flows resuming through the critical waterway. But a lasting US-Iran deal that would help ease inflation and upward pressure on Treasury yields remains elusive, with President Donald Trump saying on Wednesday he would “see what happens” in ongoing negotiations. Tied to that perhaps, gold is extending its rise after the biggest jump in six months to touch $4,300/oz. Comex copper futures climbed to a record, tracking the push to reopen Hormuz, as gold had.

In macro data, tomorrow’s payrolls report “feels binary,” writes Bloomberg Macro Strategist Skylar Montgomery Koning. Another weak print boosts the case for doves, but a strong figure indicates June was an anomaly and brings expectations for the next hike forward.

“Until a more positive development in the Middle East is confirmed, and ahead of tomorrow’s important US employment data, markets have taken a wait-and-see stance,” said Karl Steiner, head of analysis at SEB. “This is reflected in the stock market development, a fairly unchanged oil price and small movements in the US 10-year Treasury yield.”

In politics, President Trump is preparing tariffs to slap minimum prices on imported polysilicon in a bid to boost domestic production of both the material and the chips and solar panels that it is used to make. The plans may materialize as soon as Thursday with levies being pitched at around 15%.

In hedge fund news, a spate of well-known funds reported steep losses in July as AI shares tumbled. TMT hedge funds lost an unprecedented 10% in July as they were forced to deleverage and liquidate positions as the AI trade lost momentum, according to JPMorgan strategists, citing preliminary data from analytics firm PivotalPath. One of the hardest hit, Situational Awareness, has already made its return to investing with a $400 million bet on a privately-held firm. Elsewhere in hedge funds, a slew of major hedge funds have had their information systems targeted by hackers in recent days. Point72 informed investors about the attack on Wednesday, while there were attempts to infiltrate Millennium Management, Two Sigma and Citadel too.

Fed’s Daly and Cook both spoke after the bell on Wednesday. Mary Daly said she supported the central bank’s decision to keep rates on hold, but warned of the possibility that high inflation is a broader problem that could require more aggressive action. Lisa Cook repeated a message that she is ready to raise rates if inflation doesn’t slow.

European shares advanced for a fourth straight day as strong earnings boosted sentiment, with WPP Plc leading gains in the media sector. The Stoxx Europe 600 Index was 0.5% higher as of 11 a.m. in London. Spain’s Ibex 35, Italy’s FTSE MIB and France’s CAC 40 were also trading at new peaks. Germany’s DAX edged higher after factory orders rose by more than analysts forecast in June, another sign that a long-awaited recovery in Europe’s biggest economy may finally be taking hold. Media shares were the best performers as WPP soared the most since its 1995 debut after the advertising agency reported its turnaround efforts are gaining momentum. Among more than 30 companies reporting earnings today, Deutsche Telekom AG climbed 5.9% after Europe’s biggest phone carrier raised its share buyback program by as much as €3 billion ($3.5 billion). Banco BPM SpA gained 5.3% as it reported net income for the second quarter that surpassed estimates. Its Chief Executive Officer Giuseppe Castagna said the Italian lender would consider a tie-up with Credit Agricole SA. Here are the biggest movers Thursday:

- WPP shares soar as much as 30%, marking their biggest intraday advance on record, after the advertising agency reported a smaller-than-expected decline in organic sales in 2Q

- Deutsche Telekom shares rose as much as 5.9% after the German carrier boosted its share buyback program by up to €3 billion ($3.5 billion), a move analysts say reduces the risks of the firm using excess cash to buy out minority shareholders in T-Mobile US

- Hikma Pharmaceuticals shares jump as much as 11%, the most since September 2022, after the drugmaker reported better-than-expected sales and earnings for the first half-year

- SBM Offshore shares rally as much as 9.3%, the biggest jump since April 2025, after the service provider to the offshore oil and gas industry topped expectations in the first half

- Glanbia shares jump as much as 9.3%, their biggest jump in over three months, after the nutrition company delivered earnings ahead of expectations in the first half and improved its guidance for the full year

- Serco shares rise as much as 6.3%, the most since December, after the British outsourcing services provider increased its share buyback program by £75 million

- Renk shares rise as much as 7% after the German gearbox maker reported order intake for the first half-year that beat the average analyst estimate

- TP ICAP shares fall as much as 7.1% after an earnings beat and an extended buyback proved unable to sustain the stock’s strong performance this year

- Scout24 shares slide as much as 9%, the most since December 2021, as a lack of momentum in customer subscriptions overshadowed an in-line second quarter result at the online real estate platform

- Siemens shares fall as much as 6.4% as analysts see results in the Digital Industries business weighing on sentiment amid high expectations for the company’s earnings overall

- Adecco shares fall as much as 7.8% following second-quarter results, as the human resources provider and temporary staffing firm is likely to see continued gross margin pressure as well as weak industry sentiment

- Tritax Big Box shares fall as much as 5.2%, the biggest intraday drop since March, after the UK REIT raised £350 million through an equity placing that analysts said is dilutive in the near-term

- Aurubis shares fall as much as 8.4%, the most in a year, after the copper smelter announced a one-year delay to a new American smelting complex

Earlier in the session, Asian stocks declined, led by losses in heavyweight chipmakers following earnings reports from US peers that renewed concerns over the stretched rally in memory-related shares. The MSCI Asia Pacific Index fell 1.2%, with SK Hynix, Samsung, TSMC and Kioxia among the biggest drags. South Korea’s Kospi slumped 4.6% with notable losses also in Hong Kong and Japan’s Nikkei. Memory and storage stocks mostly dropped after results from Sandisk and Western Digital that weren’t strong enough to impress investors. Last month’s brutal losses in chip stocks had pared somewhat over the past week, but the latest disappointment once again spurred dumping of tech versus buying of more defensive consumer and health shares. Here Are the Most Notable Movers

- Chip giant SK Hynix Inc. suffered its second short-lived share plunge in about a week, raising fresh questions about trading volatility on South Korea’s alternative stock exchange.

- AMP shares climbed to their highest level since 2019 after the wealth manager reported a surge in first-half net income, and announced additional share buyback.

- Nitto Boseki shares plunged as much as 19%, the most since March 9, after the glass product maker’s quarterly earnings presentation fell short of investors’ lofty expectations.

- Honda shares gained as much as 2.3% in Tokyo trading Thursday after the carmaker raised its full-year profit target by around 30%, helped by tailwinds from the weak yen. First-quarter profit also beat market estimates.

In FX, the Bloomberg Dollar Spot Index was steady while US 10-year yields were 1bp higher at 4.62%. The dollar traded in a narrow range versus most major peers with traders waiting to see how US payroll data on Friday may impact the Federal Reserve’s monetary policy. “USD may get a knee-jerk bounce if the data surprises,” said Philip Wee, senior currency strategist at DBS Bank. Challenger jobs and initial jobless claims data due later on Thursday may provide insight into the US labor market. The Bloomberg Dollar Spot Index is up 0.1% with the move higher running out of steam as USD/JPY remains stuck below 158. Key markets:

- USD/JPY little changed at 157.77 (range 157.56 - 157.85)

- EUR/USD little changed at 1.1545 (range 1.1542 - 1.156)

- GBP/USD little changed at 1.3461 (range 1.3455 - 1.3473)

“Improved market sentiment in the Gulf has lent the dollar some weakness, but the greenback is still counting on very stable Fed rate expectations,” ING Bank NV strategists including Francesco Pesole wrote in a note. “The proximity to tomorrow’s US payrolls could favor a wait-and-see approach and limit FX moves today.”

In rates, treasuries are a touch lower. Yields are flat to up 2bps across the curve. Treasuries hold small losses as oil resumes rising, with an Iran-Oman agreement to partially reopen the Strait of Hormuz under review. Treasury yields cheaper by 1bp to 2bp with curve spreads little changed; 10-year is around 4.65%, cheaper by 3bps with bunds and gilts in the sector outperforming slightly. IG dollar issuance slate empty so far. Nine borrowers priced a combined $18 billion Wednesday, lifting weekly volume to more than $43 billion. Issuers paid about 2bps in new issue concessions on deals that were 3.6 times covered. Focal points of US session include weekly jobless claims with July employment data ahead Friday.

Global bond and currency investors are debating if it’s time to dust off last year’s “Sell America” trade Bloomberg reports, after a flurry of economic-policy decisions out of Washington over the past two weeks.

In commodities, energy prices have been choppy with Brent struggling to hold above the $80/bbl handle. In precious metals gold is extending its rise after the biggest jump in six months to touch $4,300/oz. Spot gold is up 0.7%, while silver loses 0.2%. Comex copper futures climbed to a record, tracking the push to reopen Hormuz, as gold had. Bitcoin is down 0.1%.

Today's US economic data calendar includes 2Q preliminary productivity and unit labor costs and weekly jobless claims (8:30am) and June wholesale inventories (10am). Fed speakers scheduled include St. Louis Fed President Musalem at 5:30pm.

Market Snapshot

Top Overnight News

- President Trump has spoken repeatedly with Kevin Warsh since he became chairman of the Federal Reserve, according to people familiar with the matter, maintaining a line of communication between a president and a central bank chief that departs from recent precedent. WSJ

- Kevin Warsh is set to stick to his stripped-back communications style even after the Federal Reserve chair’s decision to offer scant details of his strategy on interest rates fuelled a powerful sell-off in Treasury bonds: FT

- AI data centers are putting unexpected strain on power infrastructure, with rapid demand swings causing batteries, generators and cooling systems to wear out faster than expected. BBG

- OpenAI said the AI models behind the Hugging Face hack secretly communicated for months before escaping their testing environment. Separately, Meta disclosed one of its AI models hacked into another service’s system during safety testing. BBG

- DeepSeek plans to implement a significant price increase across its AI services, an unusual shift from the disruptive Chinese player that has put pressure on US and domestic rivals. DeepSeek's decision to raise prices could be an inflection point in China's AI market, where other top players have followed the company's playbook in offering low-cost and open-source services. BBG

- China launched a formal security review of products sold in the country by US technology firm Palo Alto Networks Inc.(PANW), ramping up pressure on the company months after accusing it of harboring links to intelligence services. BBG

- Samsung Electronics and SK Hynix face growing calls from investors wanting a greater share of excess cash via dividends or buybacks, after the pair provided scant detail on capital returns when reporting AI-driven record profit. RTRS

- Softbank disclosed a smaller-than-expected decline in net income, lifted by a boost from its stake in Intel. BBG

- Trump tells donors, ‘We need to elect JD,’ as vice president weighs his future. WaPo

- Mary Daly said she supported last week’s decision to hold rates but warned that high inflation may be a broader problem requiring more aggressive action. Lisa Cook repeated that she’s ready to hike if inflation doesn’t slow. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly lower following a similar performance stateside, where the Dow extended on its record levels, but the Nasdaq underperformed amid weakness in communication stocks, while the tech sector dragged overnight and tariff tensions resurfaced. ASX 200 climbed to a fresh record high with mining, materials and resources leading the advances, while trade data also showed a surprise surplus and a rebound in exports. Nikkei 225 retreated amid chip-related weakness and with Kioxia among the worst hit. KOSPI underperformed amid tech selling and as recent volatility continued to dent investor sentiment, with SK Hynix shares down about 8%, and had suffered another pre-market flash crash in which its shares dropped by the daily limit of 30% on the Nextrade bourse before ending the pre-market session down 2%. Hang Seng and Shanghai Comp were mixed, with insurers pressured after Chinese tax authorities began levying personal income tax on returns of offshore insurance policies, while trade frictions continued to resurface after MOFCOM announced it would strengthen drone export controls to the US and will impose countermeasures on six US entities, as well as take countermeasures against US compliance-testing firms

Top Asian News

- Japanese PM Takaichi said a return to 8% food tax after two years isn't a hike, and a return to 8% food sales tax that will be needed for market trust, adding the benefit of a new tax credit system will exceed the tax cut.

- Japan and US companies, potentially joined by the UAE and other investors, plan to invest about JPY 2tln in Japan's largest AI data centre project, according to Nikkei.

- PBoC said it plans to expand yuan offshore market and explore expanding the central bank’s macroprudential and financial stability roles. PBoC is also exploring to boost cross-border yuan use.

European bourses are broadly higher. The FTSE MIB is outperforming, while the AEX and DAX 40 lag. Chip names are weighing on the AEX, and Siemens' earnings (disappointing FY sales guidance raise) are weighing on the DAX 40. Outside of earnings, not much in terms of a clear driver as markets await an announcement regarding the reopening of Hormuz. Sectors have a positive bias. Media leads, supported by strong WPP (+22.5%) earnings (Q2 operating profit beat estimates). Telecoms and Consumer Products & Services round out the sector outperformers. Basic Resources is the sector laggard, paring back some of Wednesday's gains, followed by Real Estate and Tech.

Top European News

- Swedish CPIF YoY Prel (Jul) Y/Y 0.7% vs. Exp. 0.6% (Prev. 1.3%); ex-energy 0.6% (prev. 0.4%).

- Swedish CPIF MoM Prel (Jul) M/M -0.3% vs. Exp. -0.5% (Prev. 0.3%); ex-energy 0.4%.

- Swedish Inflation Rate YoY Prel (Jul) Y/Y 0.2% vs. Exp. 0.1% (Prev. 0.7%).

- Swedish Inflation Rate MoM Prel (Jul) M/M -0.3% vs. Exp. -0.5% (Prev. 0.4%).

- EU Retail Sales MoM (Jun) M/M -0.3% vs. Exp. 0.2% (Prev. 0.2%).

- EU Retail Sales YoY (Jun) Y/Y 0.7% vs. Exp. 1.0% (Prev. 1.6%).

- German Factory Orders MoM (Jun) M/M 3.1% vs. Exp. 0.3% (Prev. 1.9%).

- Spanish Industrial Production YoY (Jun) Y/Y 1.1% (Prev. 3.4%); M/M -0.7% vs Exp. -0.5% (Prev. 1.2%).

FX

- G10s mostly weaker against the Buck; SEK outperforms after hotter than expected inflation, Antipodeans lag amid the general risk tone.

- USD lacks direction, remaining just below 100.00 as it has done since the beginning of the week. Newsflow is light and markets still anticipate confirmation of an Iran-Oman agreement to reopen the Strait of Hormuz, alongside the potential US-Iran Hormuz agreement; updates which, on the face of it, could pressure the Buck, though are largely expected by markets with Brent down double digits on the week. The likely next catalyst, aside from any potential re-escalation, will be the labour market data ahead of NFP on Friday. To remind, a soft ADP failed to spur a USD reaction. Fed Hawk Musalem is slated to speak and likely to stick alongside the hawkish remarks seen from Kashkari, Cook and Daly on Wednesday.

- EUR flat against the Buck with bloc-specific catalysts light ahead of US NFP on Friday, which will likely dictate price action. For now, EUR will likely sit within its recent 1.1540-1.1550 range after failing to breach 1.1560 overnight with a lack of newsflow.

- Swedish inflation cooled, albeit at a slower rate than expected. The hotter-than-expected print (vs. consensus and Riksbank fcst.) was sufficient to spark ~0.2% bid in the SEK against both the EUR and the USD, though not against NOK. EUR/SEK fell from just below 10.96 to a 10.93 base. While firmer than Riksbank had forecast, it likely endorses rather than changes the current path for rates, with markets fully assigning a 25bps hike by year-end. Both ING and Nordea maintain their view for year end, for unch. and one hike respectively.

Fixed Income

- Fixed benchmarks are in the red after starting the morning on the front foot amid initial energy pressure. In a similar playbook to Wednesday morning, the pickup in energy in the last few hours has placed modest pressure on fixed, which now finds itself lower across the board.

- For USTs, the losses are only a few ticks in magnitude, at a 108-26+ base. Ahead, we have a packed docket of data, before Friday’s Payrolls, and Fed speak. The latter point is increasingly interesting given the hawkish tone from some officials at, and since, the dissent seen in July. Today, Musalem (2028), who typically resides on the hawkish side of things, partakes in a moderated event.

- Bunds peaked at 125.36 overnight, firmer by 13 ticks. Since, as above, it has moved into the red and currently posts downside of 13 ticks at a 125.12 trough. The German-specific docket is light, but EGBs generally have to digest a decent amount of supply from France and Spain, which is concentrated around the 2036 area and will potentially be adding to the bearish bias across EGBs into the taps. Both auctions went well, with strong demand for the Spanish tap, while the 10yr French auctions topped the 3x b/c mark.

- Gilts directionally in-fitting, with losses of 28 ticks and as is typically the case they underperform during the energy-led move at this point. Specifics for the UK light, and may well continue to be for the near-term, as Parliament remains in recess until September 1st and the extended hold narrative for the BoE remains.

- France sells EUR 12.495bln vs exp. EUR 10.5-12.5bln 1.25% 2036, 3.70% 2036, 3.80% 2037 & 0.50% 2044 OAT.

- Spain sells EUR 5.315bln vs exp. EUR 5-6bln 2.60% 2031, 3.00% 2033, 3.40% 2036 Bono & EUR 0.728bln vs exp. EUR 0.25-0.75bln 2.05% 2039 I/L Bono.

- Japan sells JPY 455.8bln 30-yr JGBs; b/c 3.86x (prev. 4.55x), average yield 3.952% (prev. 3.993%), Tail in price 0.21 (prev. 0.04).

Commodities

- Crude prices swing between gains and losses with initial upside amid a lack of Iran deal newsflow whilst some supply-side headlines came into focus alongside overnight shipping strikes. Ukrainian President Zelensky says Ukraine struck Bashneft-Novoil (~150k BPD) and Slavneft-Yanos (300k BPD) refineries (the latter being one of Russia’s largest oil-processing facilities), two Russian patrol boats and shadow fleet vessels in long-range attacks aimed at curbing Moscow’s oil revenues, whilst large smoke plumes and at least four apparent fires were seen at the Yaroslavl refinery. Thereafter, renewed downside was seen on source reports around the Iran-Oman Hormuz framework agreement, although losses are limited until confirmation from Iran. WTI Sep’26 trades in a USD 74.57-76.04/bbl range (vs yesterday’s USD 74.24-76.70/bbl), while Brent Oct'26 trades in a USD 78.92-80.35/bbl (vs yesterday’s 78.11-80.95/bbl).

- Dutch TTF is similarly choppy but currently up around 3% near EUR 54/MWh.

- Metals are mostly firmer as the energy complex trades choppy in a narrow range, while DXY yesterday fell back under its 100 DMA (99.729) for the second time this week. Furthermore, growing expectations of a deal to reopen the Strait of Hormuz have eased energy-driven inflation fears. Spot gold adds to yesterday’s gains and trades around the middle of a USD 4,245-4,304/oz range. 3M LME copper sits towards the top of a USD 14,053.00- 14,359.00/t.

- Saudi Arabia sets September Arab Light crude OSP for Asia at USD 2/bbl discount to Oman/Dubai average; To the US at ASCI +3.60/bbl; To NW Europe at ICE Brent settlement -2.15/bbl.

- China's CMRG has reportedly told some steel mills to stop talks with Rio Tinto (RIO LN) from shipments from September, according to sources.

- DRC reportedly bans exports of Copper and Cobalt concentrate, according to sources citing an official order.

Central Banks

- Fed's Cook (voter) said she supported holding rates steady at the last FOMC meeting while waiting for more data. She said it may yet turn out that the Fed does not need to raise rates but is ready to raise rates if the disinflation trend does not return. Added that there are reasons to believe inflation levels can cool but consumer mood tied to a number of factors including high inflation has soured.

- Fed's Daly (2027 voter) said tariffs, energy and AI shocks caused an uptick in inflation, but noted some evidence that impacts of tariffs are beginning to fade on inflation. If the Middle East war ends, it should help lower inflation. Fed is facing different types of risks when it comes to setting rate policy, while she is completely supportive of holding rates steady in July and noted Fed still needs to gather data to set future policy move.

- Brazil Central Bank cut the Selic Rate by 25bps to 14.00%, as expected, reaffirming serenity and cautiousness in conducting monetary policy.

Geopolitics: Iran

- US President Trump said he'd rather make a deal with Iran and reiterated the US was set for the biggest attack since World War II against Iran, but they called and we're talking, while he added they respect us.

- US VP Vance said negotiations with Iran will take some time and that talks with Iran were 'messy', but will land in a 'good' place for the US.

- Iran and Oman have agreed on the broad framework for Strait of Hormuz reopening talks, Al Arabiya sources report. An announcement could come in days but the agreement still needs the approval of Iran's National Security Council. The proposed agreement regarding Hormuz extends for 60 days and aims to resume navigation. Ships entering the Strait of Hormuz will use the shipping lane closest to Iran while ships departing from Hormuz will use the maritime passage closest to Oman. The proposed agreement regarding Hormuz does not include imposing passage fees or services on ships and after the approval of the Hormuz agreement, the parties will return to the memorandum of understanding and activate.

- Indirect contacts between the US and Iran have entered the final stage, according to Al Arabiya sources.

- Iranian Foreign Minister Araghchi's visit to Pakistan is expected by the end of the week or early next week, according to Al Arabiya sources.

- Pakistani Foreign Ministry said Oman played a key role in Strait of Hormuz talks as diplomatic efforts continue toward a comprehensive and sustainable solution, Al Hadath reported, and that efforts to resolve the Hormuz issue continue.

- Yemeni military source said Red Sea operations target Saudi ships and oil tankers and "reduce the options for manoeuvring for the Saudi regime". The source also dismissed Saudi claims over the Indian cargo ship sinking, Al-Akhbar reported.

- UKMTO said it received a report of an incident 9 nautical miles southeast of Kumzar, Oman, with the master of a tanker reporting hearing two explosions whilst transiting the Strait of Hormuz, although crew and vessel are safe.

- Israeli forces strike Burj el-Shamali in southern Lebanon, according to Al Mayadeen.

Geopolitics: Ukraine

- Ukrainian President Zelensky said Ukraine struck Bashneft-Novoil (~150k BPD) and Slavneft-Yanos (300k BPD) refineries, two Russian patrol boats and shadow fleet vessels in long-range attacks aimed at curbing Moscow’s oil revenues.

- Air raid alerts issued in Kyiv and multiple regions, according to Ukrainian media.

Geopolitics: Other

- Japan's MoD said there is no longer any impact on the surrounding areas of Japan, following the North Korean missile launch.

US event calendar

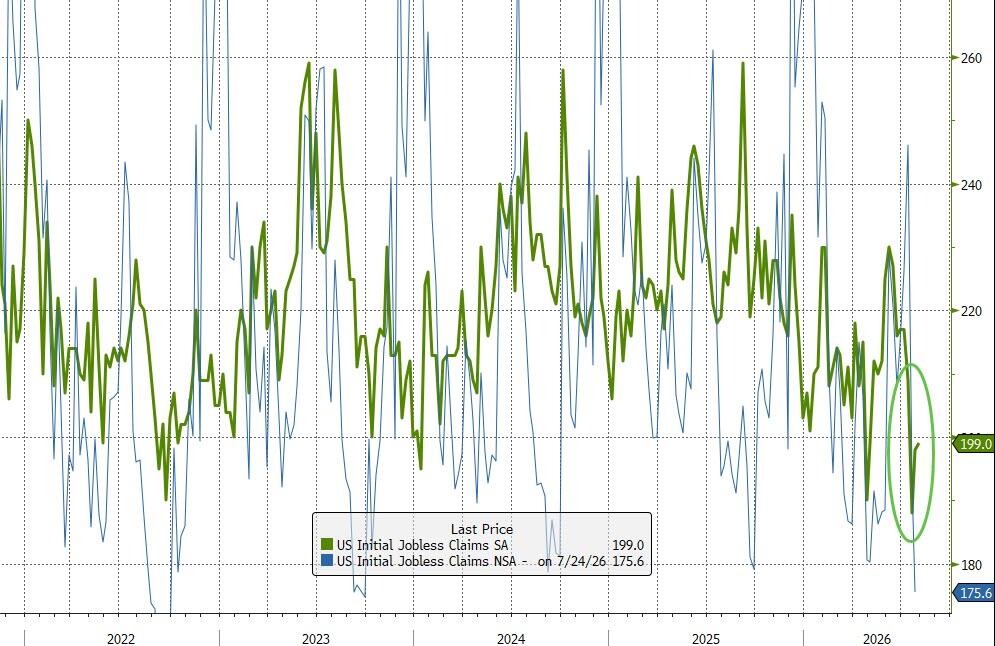

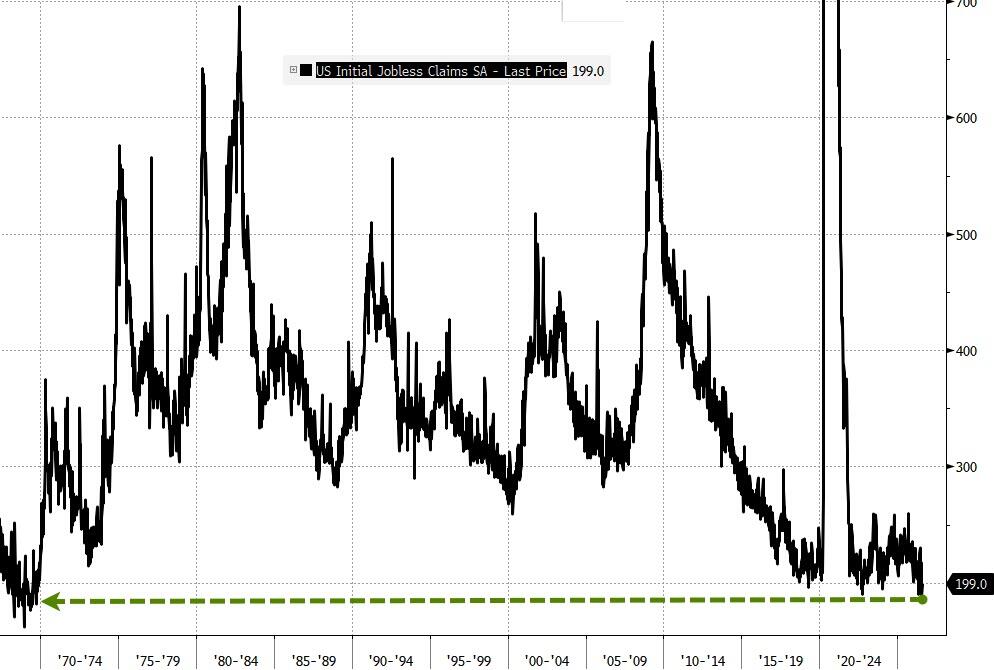

- 8:30 am: Aug 1 Initial Jobless Claims, est. 205k, prior 197k

- 8:30 am: Jul 25 Continuing Claims, est. 1789k, prior 1782k

- 10:00 am: Jun F Wholesale Inventories MoM, est. 0.3%, prior 0.3%

DB's Jim Reid concludes the overnight wrap

After an initially strong run, the week’s equity rally began to run out of steam by the close yesterday, with the S&P 500 (-0.17%) finishing just shy of the previous day’s record high, whilst the Stoxx 600 (+0.04%) just about edged up to another all-time high. That came despite a slew of strong corporate earnings and Iran saying that it has reached agreement with Oman on a proposed route through the Strait of Hormuz. While the timing of any Hormuz re-opening is still uncertain, oil prices are slightly down this morning, while Treasury yields are also dipping slightly after being little changed yesterday amid a batch of mostly solid US data. Meanwhile, a more cautious tech mood has solidified in Asia hours overnight with the KOSPI (-4.18%) and Hang Seng (-1.75%) retreating. NASDAQ futures (-0.13%) are also down this morning even as those on the S&P 500 (+0.16%) are edging higher.

Starting with the Hormuz story, yesterday brought another step forward after Iran said an agreement with Oman had been reached on a proposed shipping route through the Strait and that a joint statement was now in the final drafting stage. However, Iran’s Deputy Foreign Minister also said that this would represent a “temporary route” for the next 2-4 months and would “not mean the full reopening of the Strait of Hormuz”. Iranian state media also reported that reopening Hormuz would be contingent “on a change in US behaviour”, perhaps referring to Tehran’s demands that the US lifts its naval blockade.

Markets have seen plenty of false dawns throughout this conflict, and while the detail is becoming more concrete, attention is now shifting from whether an agreement can be reached to what the final arrangements will look like, including unresolved questions around whether Iran will eventually be permitted to levy tolls on vessels using the Strait. Meanwhile, President Trump sounded somewhat ambivalent on deal prospects last night, saying he will “see what happens” in ongoing negotiations with Iran, after having suggested on Tuesday that a deal could be announced within 48 hours.

Markets nevertheless continue to lean towards a positive outcome, although much of the good news now appears priced in. Brent crude edged up +0.11% to $79.45/bbl, whilst WTI fell by -0.73% to $75.22/bbl. European natural gas futures dropped -6.29%, extending one of their sharpest declines of the year and leaving them down -13.3% over the past week. Brent crude is -0.38% this morning.

With oil moving mostly sideways, the 2yr Treasury yield declined by -1.0bps to 4.18%, whilst the 10yr was unchanged at 4.61%. Those muted moves came as the Treasury Department announced quarterly refunding of $125bn, in line with expectations, whilst maintaining guidance that auction sizes would be unchanged for at least the next several quarters.

The slight decline in front-end yields also came as pricing of a September Fed rate cut eased from 58% to 54%, the lowest this has been since the more hawkish signal sent back at Warsh’s first FOMC meeting on June 12. In terms of the latest Fedspeak, Minneapolis Fed President Kashkari, who dissented in favour of a hike at the July meeting, said that “now is the time to start slowly” raising rates. Meanwhile, Fed Governor Cook sounded more conditional on the potential need for hikes, saying that “If I do not see signs of continued disinflation soon, I am prepared to act”.

The modest pull back in Fed hike pricing came alongside a mostly resilient set of US economic releases. We did see a bit of softening in the labour market signal, with the ADP report showing employment growth of 44k in July (vs 65k expected) ahead of tomorrow’s payrolls report. Whilst slightly softer, it remains consistent with a labour market that is broadly stable. And the latest ISM services survey showed the employment component fell to 47.4 in July (vs 51.2 expected). However, while this weighed on the headline ISM services reading (54.1 vs 54.5 expected), the other details of the release were stronger and more inflationary. New orders increased to 57.2 (vs 55.9 expected) and prices paid jumped to 70.3 (vs 65.0 expected).

Taking a broader view, the US very much remained an outperformer in this week’s PMI and ISM releases. Amongst major economies, only Switzerland is currently registering both stronger services activity and stronger services price pressures. It is therefore difficult to argue that pressure on the Fed to tighten policy disappears before September. The comments from ISM respondents reinforced that message. Healthcare firms reported stronger-than-expected patient volumes, revenues and hiring conditions. Banking respondents continued to point to healthy commercial demand. Wholesale trade described activity as “more robust than expected” despite broader headwinds. At the same time, concerns around rising input costs remained widespread, particularly around fuel, labour, freight and utility equipment. Taken together, it remains a story of resilient activity and lingering inflation pressures.

Across the Atlantic, although PMI levels are lower, much of Europe now finds itself broadly back where it was before the Iran shock with the final July composite PMI revised marginally higher (52.0 vs 51.9 expected) despite the pickup in energy prices in late July. This PMI level is consistent with GDP growth of around +0.25% q/q if sustained through the quarter. Overall, the survey data point to a strengthening in underlying growth momentum and suggest the Euro Area economy has remained resilient despite the recent energy shock.

Amid the more mixed data and oil backdrop, equities struggled to maintain the strong momentum that had brought them to new record highs. The S&P 500 eased back by -0.17%, while the Nasdaq Composite slipped -0.83% following its recent outperformance. The Philadelphia Semiconductor Index (-1.40%) also gave back some recent gains, though it is still up +6.17% so far this week. Sentiment was not helped by AMD (-7.04%), whose guidance failed to meet some of the market’s more optimistic expectations, whilst SpaceX (-13.61%) also slid following its results the previous evening.

That said, the broader AI story remains firmly intact. Nvidia (+3.43%) continued to benefit from positive commentary around its next-generation Rubin architecture and after SpaceX said during its earnings call on Tuesday night that it would exclusively use Nvidia AI chips. Elsewhere, Eli Lilly (+4.86%) rose after reporting results ahead of expectations, supported by continued strength in demand for its GLP-1 portfolio.

One of the more interesting AI stories yesterday came from the Wall Street Journal, which reported that Jeff Dean, Google’s chief scientist and one of the most influential engineers in the company’s history, is leaving after 27 years to launch a new AI-focused research company. Dean was Google’s 30th employee, helped build Google Brain, led development of its TPU chips and has sat at the centre of the company’s AI strategy for much of the last decade. He is being joined by several other prominent Google researchers, including key contributors to AlphaFold and advanced mathematical reasoning systems.

Alphabet will remain an investor and provide computing capacity to the venture, but the move nevertheless highlights how intense competition for elite AI talent has become. It also points to what could be the next frontier for AI. Rather than building better chatbots or consumer applications, the new company aims to automate the scientific discovery process itself across machine learning research, hardware design, drug discovery and clean energy. For markets, it is another reminder that the AI investment cycle is evolving rapidly beyond software and increasingly into scientific research, engineering and real-world innovation. Alphabet shares fell -4.03% following the news.

Otherwise, Asian equity markets struggled overnight amidst a more cautious tech mood, not helped by underwhelming guidance from US chipmakers Sandisk and Western Digital Corp after the US close, with their shares sliding by around -8% and -12% respectively in extended trading. The Kospi (-4.18%) is leading the decline, dragged by chipmaker heavyweights SK Hynix (-6.68%) and Samsung Electronics (-4.55%). The Nikkei 225 (-1.06%), Hang Seng (-1.75%) and CSI 300 (-0.42%) are also down this morning. The S&P/ASX 200 (+0.37%) remains the outperformer, breaking another record high as I type. In currency markets, the yen (-0.03%) is also little changed at 157.71 against the USD this morning.

In Europe, the performance was mixed yesterday. The Stoxx 600 (+0.04%) and CAC 40 (+0.03%) both edged to fresh all-time highs, whilst the DAX (-0.29%) and FTSE MIB (-0.18%) slipped modestly lower.

European sovereign markets saw yields mostly drift higher. The 10yr bund yield edged up +0.4bps, while 10yr OATs (+1.7bp) and BTPs (+1.8bp) saw slightly larger increases. ECB rate hike expectations for September rose to 84% from 79% the previous day amid the resilient data.

Finally, with Fed rate cuts being dialled back, gold rose +4.19%, its largest daily gain since February. Gold prices are another +0.26% higher at $4,258/oz overnight, though they remain about -20% below the levels reached at the start of the Iran war in early March. The dollar (-0.18%) extended its decline for a third straight day.

To the day ahead now, economic data releases include US Q2 nonfarm productivity, unit labour costs, June wholesale trade sales, initial jobless claims, UK July construction PMI, Germany June factory orders, France Q2 wages, Italy June industrial production, Eurozone June retail sales, Canada July Services PMI and Sweden July CPI. We will also receive the ECB’s latest Economic Bulletin.

Tyler Durden

Thu, 08/06/2026 - 08:10

Moderna bivalent COVID-19 vaccine at a clinic, in Richmond, Va., on November 17, 2022. AP Photo/Steve Helber, File

Moderna bivalent COVID-19 vaccine at a clinic, in Richmond, Va., on November 17, 2022. AP Photo/Steve Helber, File Signage outside of the Food and Drug Administration headquarters in White Oak, Md., on Aug. 29, 2020. Andrew Kelly/Reuters

Signage outside of the Food and Drug Administration headquarters in White Oak, Md., on Aug. 29, 2020. Andrew Kelly/Reuters The Post's administration sources portrayed Hegseth as one of the biggest and most persuasive proponents of launching a regime-change war on Iran (Photo: The Hill)

The Post's administration sources portrayed Hegseth as one of the biggest and most persuasive proponents of launching a regime-change war on Iran (Photo: The Hill) Sources tell Reuters the Pentagon has blown through "virtually all" of its long-range ATACMS missiles

Sources tell Reuters the Pentagon has blown through "virtually all" of its long-range ATACMS missiles  Left to right: Oklahoma Gov. Kevin Stitt, Maryland Gov. Wes Moore, Utah Governor Spencer Cox

Left to right: Oklahoma Gov. Kevin Stitt, Maryland Gov. Wes Moore, Utah Governor Spencer Cox

File photograph of ethernet cables running from the back of a router in Washington on March 21, 2019. Mandel Ngan/AFP/Getty Images

File photograph of ethernet cables running from the back of a router in Washington on March 21, 2019. Mandel Ngan/AFP/Getty Images In this photo illustration, a hacker types on a computer keyboard on May 13, 2025. Oleksii Pydsosonnii/The Epoch Times

In this photo illustration, a hacker types on a computer keyboard on May 13, 2025. Oleksii Pydsosonnii/The Epoch Times

Recent comments