The Fourth Turning Global War Has Entered The Terminal Phase

Authored by Milan Adams via Preppgroup,

The numbers came in just after dawn on the East Coast, and they told a story that no amount of White House spin could obscure. Oil futures had stabilized at $86 per barrel overnight—a figure that would have seemed catastrophic eighteen months ago but now represented a temporary reprieve from the $119 spike that had crippled global markets in April. The Strategic Petroleum Reserve, that emergency backstop established after the 1973 crisis, had fallen to 305 million barrels, its lowest level since 1983. The Congressional Budget Office quietly released its revised deficit projections: $2.3 trillion for fiscal year 2026, with another $1.8 trillion locked in for 2027 before accounting for the war’s accelerating costs, currently running at $1 billion per day with no exit strategy visible on any horizon.

This is not a recession. This is not a “period of heightened geopolitical tension.” This is the systematic dismantling of the global economic architecture that has sustained Western prosperity for eighty years, compressed into a timeframe too brief for institutional adaptation. We are witnessing, in real-time, the transition from a unipolar American-led order to a fragmented multipolar system, and the violence of that transition is being measured not just in body counts—though those are mounting in ways the Pentagon refuses to fully disclose—but in the erosion of strategic leverage that cannot be recovered once spent.

The Fourth Turning Global War has entered its terminal phase, and the metrics suggest we are only beginning to comprehend the depth of the strategic trap into which American policy has walked.

To understand the present crisis, one must first abandon the comforting narrative of accidental drift—the notion that policy errors and miscalculation have led to the current impasse. The data suggests something more troubling: a decoupling of strategic decision-making from national interest calculation, producing outcomes that serve no identifiable American objective while advancing the interests of regional actors with disproportionate influence over U.S. policy formation.

Consider the timeline with the precision of a military after-action report. On February 27, 2026, the United States initiated a surprise decapitation strike against Iranian leadership while Israeli envoys maintained ostensible negotiations in Geneva. The strike eliminated Iran’s military command structure and political leadership in a forty-eight-hour bombardment that the White House initially projected would conclude within “four to five weeks.” That projection, made on March 1, has now stretched to month five with no conclusion visible. The Strait of Hormuz, through which twenty percent of global petroleum flows, has been effectively closed since mid-March. Iranian ballistic missile strikes, utilizing Chinese targeting data and Russian satellite intelligence, have damaged or destroyed every major U.S. installation in the Persian Gulf, including Al Udeid in Qatar, Prince Sultan in Saudi Arabia, and the naval facilities at Bahrain.

The cost-benefit analysis is devastating. The initial strike was predicated on intelligence assessments—later disputed by seventeen agencies—that Iran was “weeks away” from nuclear weaponization. This assessment contradicted the June 2025 declaration by the same administration that Iran’s nuclear facilities had been “completely and totally obliterated” in a twelve-day conflict that cost $37 billion and achieved no lasting strategic effect. The current war, prosecuted with no congressional authorization and against the expressed preferences of the electorate that returned the President to office on explicit anti-interventionist promises, has now consumed $113 billion in direct costs with Harvard analysts projecting long-term liabilities exceeding $1 trillion when veterans’ care, equipment replacement, and base reconstruction are factored.

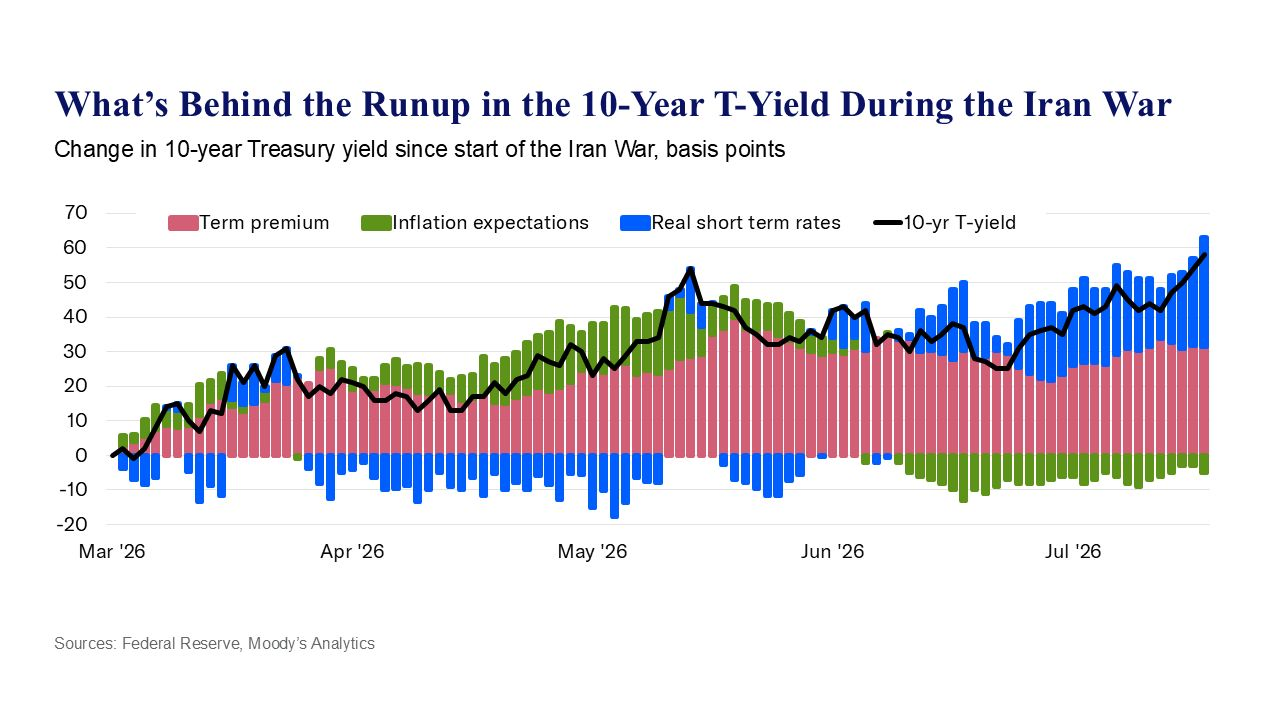

The economic externalities are equally severe. Inflation, which had moderated to 2.7% by December 2025, has reaccelerated to 4% and climbing. The 10-year Treasury yield at 4.64% represents the highest borrowing costs of the Trump presidency, translating to approximately $135 billion in additional annual interest expense and roughly $1,000 per household in direct energy and financing costs. These figures arrive at a moment when 60% of American households report inability to cover a $500 emergency expense, and consumer credit delinquencies have reached levels not seen since the 2008 financial crisis.

The strategic position has deteriorated in ways that resist quantitative measurement. The American military, designed for power projection against insurgent forces and regional adversaries, has proven vulnerable to the asymmetric warfare tactics of a mid-tier nation with sophisticated missile technology and defensive geography. The Patriot missile systems, costing $2 million per intercept, face Iranian ballistic missiles and drones costing $10,000 to $50,000 per unit—a cost-exchange ratio that renders sustained defense economically unsustainable. The revelation that Russian and Chinese intelligence services are providing real-time targeting data to Iranian forces, confirmed by satellite intercepts and acknowledged in congressional testimony, transforms a regional conflict into a proxy war with great-power adversaries testing American vulnerabilities at minimal direct risk to themselves.

The institutional response has compounded the crisis. The Department of Government Efficiency, which promised $2 trillion in administrative savings, was effectively dismantled when the “Big Beautiful Bill” added $5 trillion to the national debt—on top of the $21 trillion CBO baseline projection. The national debt has expanded from $36.2 trillion to $39.5 trillion in eighteen months, with $2 trillion annual deficits now locked in through 2030. The administration’s attempt to suppress oil prices through Strategic Petroleum Reserve drainage and derivatives market manipulation has depleted emergency reserves while exposing the hollowness of American energy “independence”—the nation now lacks sufficient buffer to withstand a sustained supply disruption, let alone a broader conflict involving Nigerian or Venezuelan production.

The geopolitical reconfiguration underway extends beyond the immediate theater. Russia, despite Western sanctions and the ongoing attrition in Ukraine, has consolidated a Eurasian security architecture incorporating Iran, China, and the expanding BRICS+ alignment. The dedollarization of international trade—accelerated by SWIFT weaponization that demonstrated the vulnerability of dollar-denominated clearing—has created parallel financial systems that will persist regardless of conflict outcome. China, while managing its own demographic and real estate crises, has secured energy corridors through the Belt and Road Initiative and established the industrial capacity to replace American military losses at scale.

The European powers face civilizational exhaustion: demographic collapse, energy deindustrialization, and the progressive loss of productive capacity to Asian competitors. Their enthusiasm for expanded NATO commitments and confrontation with Russia serves not strategic interest but distraction—the displacement of internal contradictions onto external enemies. The recent declarations by French, German, and British leadership regarding “readiness for war with Russia” represent either dangerous delusion or deliberate provocation, given the demonstrated inability of European militaries to sustain ammunition expenditure for more than weeks without American resupply.

The Architecture of Strategic Bankruptcy

The visual landscape of collapse often precedes its statistical confirmation. The imagery from the Gulf region—satellite photographs of burning tanker traffic, thermal imaging of refinery complexes offline, atmospheric data showing particulate concentrations affecting regional agriculture—prefigures economic consequences that will arrive with lagging but inexorable certainty. The SPR drainage that has suppressed gasoline prices temporarily cannot continue beyond 2027 at current extraction rates. The Hormuz closure has already disrupted grain shipments to import-dependent nations, with wheat futures decoupling from traditional pricing models and phosphate export restrictions from Morocco and China threatening global food security.

The famine that development economists projected for 2030 has accelerated to 2027. Diesel availability for agricultural planting and harvest has become uncertain at prices permitting profitability. European fertilizer production, shuttered by energy costs in 2022-2023, has not resumed capacity. The global just-in-time supply chain, already fractured by pandemic policies and Suez disruption, approaches catastrophic failure as Red Sea interdiction by Houthi forces—equipped with Iranian missile technology—severs the maritime artery connecting Europe to Asian manufacturing.

This is not “market volatility.” This is the end of abundance—the reversion to a world where calorie and energy allocation follows political rather than economic logic, where reserve currency status no longer guarantees import capacity, and where the institutional frameworks established in 1944-1945 have ceased to function.

The psychological dimension of collapse resists quantification but demands analysis. The American population has been systematically anesthetized through pharmaceutical intervention (twenty-five percent of adults on psychiatric medication), digital addiction (average seven hours daily screen time), and ideological polarization that substitutes tribal identity for rational assessment. The same populations who accepted emergency measures during the 2020-2023 period based on epidemiological models with no empirical validation now dismiss warnings of systemic collapse as alarmism—while simultaneously accepting narratives of imminent threat from Iran that contradict the assessments of their own intelligence agencies.

The manufacturing of consent has reached its terminal phase. Media organs that promoted Russiagate as fact for three years now present Netanyahu’s Iran narrative as unquestionable truth. Conservative commentators who warned of executive overreach now justify the merger of state and corporate power as necessary security measures. The “uniparty” phenomenon—seamless continuity of policy between ostensibly opposed political formations—has become too obvious to deny, yet too uncomfortable to acknowledge for populations invested in the theater of democratic choice.

The Projection: Winter 2027-2028

Current trajectory analysis suggests the following developments with high probability:

By Q4 2026, the Strategic Petroleum Reserve will approach technical minimums, removing the administration’s capacity to suppress oil prices through market intervention. Energy costs will spike to levels that trigger cascading defaults in the transportation and logistics sectors, with trucking bankruptcies producing food distribution failures in major metropolitan areas. The Federal Reserve, caught between inflation acceleration and financial system fragility, will face the impossible choice of defending the currency or preventing sovereign debt crisis—likely attempting both and achieving neither through yield curve control that destroys market function.

The 2026 midterm elections, should they proceed on schedule, will occur against a backdrop of 6-7% inflation, 7% mortgage rates, and visible military failure in the Gulf. The political response—likely involving expanded emergency powers and the suspension of procedural norms—will accelerate the legitimacy crisis already visible in polling showing majority belief that “the system is rigged” regardless of partisan affiliation.

By mid-2027, absent Hormuz reopening, the global food system will face structural breakdown. Import-dependent nations in North Africa, the Middle East, and South Asia will experience mass migration events that make 2015 appear trivial. European border controls, already overwhelmed, will collapse entirely, producing the demographic and security crises that nationalist movements have predicted—and that mainstream institutions have dismissed as xenophobia.

The American military, exhausted by Gulf deployment and unable to replenish losses at industrial capacity, will face strategic overextension should conflict expand to include Taiwan or Korean scenarios. The revelation of actual casualty figures—currently suppressed through classification and media complicity—will produce domestic political crisis when inevitably disclosed.

The dollar’s reserve status will not collapse catastrophically but will erode incrementally, as BRICS+ nations complete bilateral currency arrangements and commodity producers demand payment in gold or yuan. This process, already underway, will accelerate as American debt monetization becomes impossible to ignore, producing the stagflation scenario that destroyed the 1970s consensus but at an order of magnitude greater severity.

The Reckoning: What the Data Cannot Capture

There are dimensions of civilizational crisis that resist econometric modeling.

The social capital depletion—the erosion of trust, the atomization of community, the substitution of digital simulation for embodied relationship—has progressed to levels that preclude collective response to systemic stress. The American population retains the technological capacity for coordination but has lost the cultural capacity for trust, producing the paradox of hyperconnectivity without solidarity.

The generational theory that predicted this moment—the Fourth Turning framework—suggested that crisis would forge new civic capacity through shared sacrifice. The evidence suggests instead a fragmentation trajectory, in which the stresses of collapse accelerate division rather than unity, producing not a “new High” but an extended period of interregnum—the old order dead, the new order unborn, the monsters roaming freely in the interval.

The psychological impact of sustained strategic decline—what historians term “imperial melancholy”—has produced a politics of compensatory fantasy, in which technological innovation (artificial intelligence, cryptocurrency, space colonization) serves as psychological defense against the recognition of material contraction. The billions invested in “data centers” that function as surveillance infrastructure, the meme coins that extract value from retail investors, the “smart city” projects that track and trace populations—represent not progress but cargo cults, magical thinking in technological guise.

The biological dimension of crisis—declining fertility, collapsing testosterone levels, epidemic levels of psychiatric medication dependency, the mysterious excess mortality that insurance actuaries have documented but media institutions refuse to investigate—suggests a population too physically and cognitively compromised to mount the collective response that historical crisis has previously elicited. The “Great Reset” agenda, whether conspiracy or strategy, represents an elite recognition that the existing population cannot be saved, only managed through its decline—a Malthusian calculus that dare not speak its name but structures policy regardless.

Conclusion: The Long Emergency

We are not approaching crisis. We are within it. The Fourth Turning Global War is not a future possibility but a present reality, consuming the institutional capital accumulated over eighty years of American hegemony at a rate that precludes recovery. The debt cannot be repaid. The empire cannot be sustained. The social contract cannot be restored. These are not defeatist assertions but empirical observations, supported by Treasury data, CBO projections, and the visible degradation of infrastructure, education, and public health that surrounds anyone willing to look.

What remains is the question of duration and form. The crisis of the 1930s-1940s resolved in seventeen years through total war and the establishment of a new institutional framework. The current crisis, accelerated by technological disruption and financialized complexity, may extend longer—or resolve more suddenly through catastrophic failure modes (nuclear exchange, pandemic, grid collapse) that render duration irrelevant.

The individual response to systemic crisis cannot reverse systemic trends but can prepare for systemic outcomes. The reconstruction of local capacity—food production, energy generation, security provision, currency exchange—represents the only available hedge against institutional failure. The Amish model, long dismissed as anachronism, reveals itself as adaptive strategy: technological selectivity, communal self-sufficiency, religious cohesion, and geographic dispersion providing the resilience that centralized systems cannot maintain under stress.

The political question—whether the republic can be saved, whether the Constitution can be restored, whether the enemies foreign and domestic can be identified and defeated—may be the wrong question. The right question is whether civil society can be maintained through the transition, whether the skills and trust networks necessary for post-collapse coordination can be preserved, and whether the human capacity for dignity and moral choice can survive the humiliation of imperial decline.

Thomas Paine wrote that these are the times that try men’s souls. He did not promise victory. He promised that the harder the conflict, the more glorious the triumph. But he wrote in a moment when the American population retained the competence for self-governance and the will for collective sacrifice. Whether those qualities persist in sufficient concentration to generate a “new High” from the present Crisis remains the open question of our era—a question that will be answered not by analysts but by the emergent behavior of millions of individuals confronting the erosion of everything they assumed permanent.

The winter is here. The long night has begun. And the saeculum, indifferent to human preference, continues its relentless turn.

Tyler Durden

Thu, 07/30/2026 - 23:25

Seattle Mayor Katie Wilson (C) and Seattle Police Chief Shon Barnes (L) attend the vigil for victims the day after a shooting at Seattle Center during the Bite of Seattle food festival, in Seattle on July 27, 2026. Lindsey Wasson/AP Photo

Seattle Mayor Katie Wilson (C) and Seattle Police Chief Shon Barnes (L) attend the vigil for victims the day after a shooting at Seattle Center during the Bite of Seattle food festival, in Seattle on July 27, 2026. Lindsey Wasson/AP Photo

Dr. Anthony Fauci, former director of the National Institute of Allergy and Infectious Diseases at the National Institutes of Health, testifies before the Senate Committee on Homeland Security and Governmental Affairs in Washington on July 29, 2026. Madalina Kilroy/The Epoch Times

Dr. Anthony Fauci, former director of the National Institute of Allergy and Infectious Diseases at the National Institutes of Health, testifies before the Senate Committee on Homeland Security and Governmental Affairs in Washington on July 29, 2026. Madalina Kilroy/The Epoch Times Sen. Rand Paul (R-Ky.), chairman of the Senate Committee on Homeland Security and Governmental Affairs, speaks during a hearing with Dr. Anthony Fauci, former director of the National Institute of Allergy and Infectious Diseases at the National Institutes of Health, in Washington on July 29, 2026. Madalina Kilroy/The Epoch Times

Sen. Rand Paul (R-Ky.), chairman of the Senate Committee on Homeland Security and Governmental Affairs, speaks during a hearing with Dr. Anthony Fauci, former director of the National Institute of Allergy and Infectious Diseases at the National Institutes of Health, in Washington on July 29, 2026. Madalina Kilroy/The Epoch Times

US Army photo

US Army photo

Source: Armament Research Services

Source: Armament Research Services

Recent comments