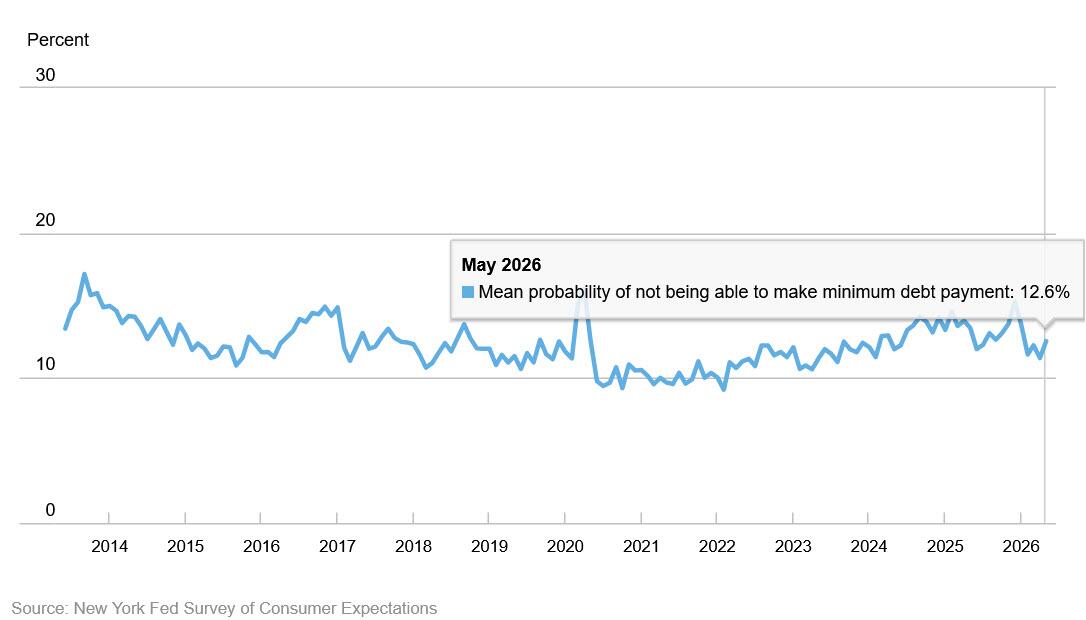

India Rescues 24 Crewmembers From Stricken Tanker Off Oman After US Airstrike

Update(1315ET): US Navy forces have announced a new Monday direction action operation in the Gulf of Oman. The US has cited that the vessel refused to respond to orders related to the blockade of Iranian naval ports.

The ship attempted to sail to an Iranian port, in violation of the ongoing blockade. A CENTCOM statement indicated that the military "disabled Palau-flagged M/T Marivex as it transited international waters in the Gulf of Oman toward Iran."

"An F/A-18 Super Hornet from USS Abraham Lincoln (CVN 72) fired a precision munition into the ship's engineering and steering spaces after the crew failed to comply with directions from U.S. forces," the statement continued. "Marivex is no longer sailing to Iran," it said. The Pentagon has also reviewed the following since initiating the blockade on April 13.

- CENTCOM forces have disabled seven non-compliant vessels

- it has redirected 134 ships that complied

- allowed 42 vessels supporting humanitarian aid to pass

This is the same vessel which took on US military fire:

Indian navy helicopters airlifted 24 sailors off a tanker on fire off the coast of Oman on Monday, New Delhi officials said, without saying what caused the blaze.

India’s Ministry of Ports, Shipping and Waterways said a fire was reported at around 1:30 p.m. (0800 GMT) on the MT Marivex, a Palau-flagged tanker.

“There has been a fire reported on a vessel, MT Marivex, on which there were 24 Indian seafarers... all Indian seafarers are safe,” ministry director Opesh Kumar Sharma told reporters.

And more from the same report:

Images posted on social media by the Forward Seamen’s Union of India showed crew members being winched from the vessel by helicopter as thick black smoke billowed from its bridge and accommodation cabins.

The tanker’s position was shown by ship-tracking service MarineTraffic as being off the coast of Oman, south of the capital Muscat.

* * *

Brent crude futures jumped as much as 5% to $97.83 a barrel, while WTI traded around $95 a barrel, as renewed Iran-Israel fighting threatened to unravel a fragile US-Iran ceasefire and further disrupt energy flows.

On the maritime chokepoint front, Iran-backed Houthis declared a full ban on Israeli vessels in the southern Red Sea, warning that any Israeli ship (or linked ship) will be seen as a military target.

"First: We declare a complete and total ban on maritime navigation for the Israeli enemy in the Red Sea, and we consider all enemy movements to be military targets for our Armed Forces from the moment this statement is issued," the terror group said Monday in a statement.

The statement continued, "Second: We affirm that we will meet escalation with escalation, and that our military operations will escalate in line with events, the battle, and in conjunction with the axis of Jihad and Resistance."

"Third: We affirm the right of our people and the peoples of our free nation to confront American-Israeli aggression, and that we will not stand idly by in the face of the unjust siege imposed on our people and the peoples of the axis of Jihad and Resistance in Palestine, Gaza, Iran, Lebanon, and Iraq. All enemy attempts will fail, God willing, and our operations will continue as long as the aggression and siege against us and the axis of Jihad and Resistance continue," the statement concluded.

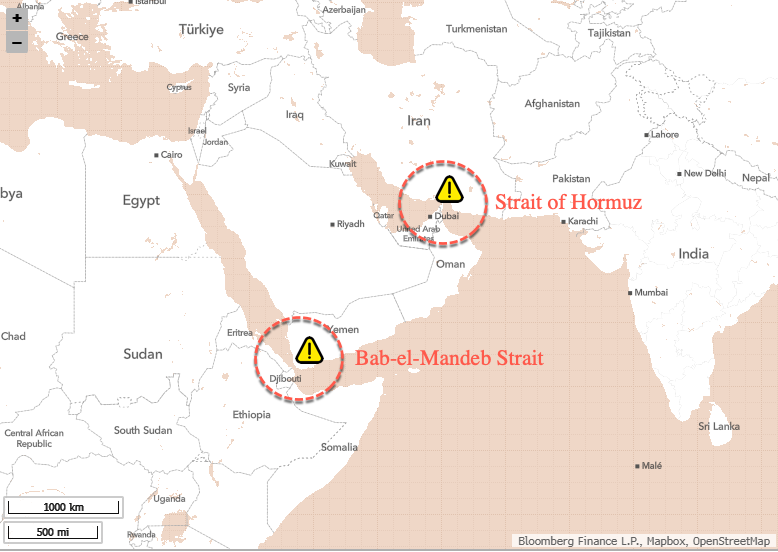

The Houthis have announced a "complete blockade" of the Red Sea and the Bab al-Mandab Strait against all vessels linked to Israel.

— Egypt's Intel Observer (@EGYOSINT) June 8, 2026

They also warned that any further escalation will be met with an even stronger response. pic.twitter.com/fu6UFPtD1G

The announcement is similar to the Houthis' late-2023 campaign, when rebel forces attacked ships linked to Israel or bound for Israeli ports in or around the Bab-el-Mandeb Strait. They framed the attacks as retaliation for the Gaza war.

Potential disruption of the Bab-el-Mandeb Strait in the southern Red Sea will only add to the headaches for global maritime trade, as it is a critical sea route for Asia-to-Europe commerce and Gulf energy exports.

At its narrowest point, the strait is about 18 miles wide, making commercial vessels extraordinarily vulnerable to suicide drones, missiles, mines, and small boats.

The previous disruption of the Bab-el-Mandeb Strait led to ships rerouting around the Cape of Good Hope, adding time, fuel, insurance costs, and higher shipping costs. The IMF has previously said that the Red Sea attacks halved Suez Canal trade in early 2024, while shipping traffic via the Cape of Good Hope surged.

Related:

-

Alarming Supply-Chain Stress Sends Transport Cost Soaring, Fueling Inflation Fears

-

UBS Reactivates Supply-Chain Stress Watch After Detecting Alarmingly Rapid Deterioration

Readers were brefied in mid-April on the threat other critical straits could be disrupted. Read the note here.

The big risk here is a simultaneous disruption of both maritime chokepoints. Bab-el-Mandeb would hit the world's trade artery, while Hormuz has already disrupted the world's energy artery. Combined, the clogging of both maritime chokepoints would be viewed as a major escalation, likely raising the risk of additional supply chain stress, higher freight and insurance costs, and another inflationary wave.

Tyler Durden Mon, 06/08/2026 - 13:15 An undated photograph shows an aerial view of Diego Garcia. U.S. Navy via AP

An undated photograph shows an aerial view of Diego Garcia. U.S. Navy via AP

People protest outside the High Court where Chagossian campaigners are challenging the British government's deal to transfer sovereignty of the Chagos Islands to Mauritius, in London, Britain, October 28, 2025.

People protest outside the High Court where Chagossian campaigners are challenging the British government's deal to transfer sovereignty of the Chagos Islands to Mauritius, in London, Britain, October 28, 2025.

A hiring sign at the Fashion Centre at Pentagon City shopping mall in Arlington, Va., on Jan 3, 2024. Madalina Vasiliu/The Epoch Times

A hiring sign at the Fashion Centre at Pentagon City shopping mall in Arlington, Va., on Jan 3, 2024. Madalina Vasiliu/The Epoch Times

Recent comments